1. INTRODUCTION

Religious organizations in Jamaica are very vital to the country’s development. This is evident in the various social services and amenities that they provide. Some of these services and amenities include schools, hospitals, social intervention programs, and spiritual guidance to enhance the spiritual life of individuals. While they provide these services, there are times when churches find it very difficult to conduct their missionary activities because of insufficient financial resources. Often, this could be due to improper management of the church’s resources because of inadequate or no internal controls. Churches need to manage their financial resources properly. Frequently internal controls are overlooked due to the belief that Christians can be trusted; however, humans make errors sometimes (Hudson, 1984).

Tanui, Omare, and Bitange (2016) projected that by 2025 the global Christian community is expected to bring in $350 billion annually for the church. Nevertheless, the 2013 estimates from Status Global Missions and the Centre for the Study of Global Christianity indicated that worldwide, Christians engaged in fraudulent activities within the Church, amounting to more than $37 billion. They argue that this highlights a concerning trend of corruption that has spread across the globe, even in the religious sector, indicating a significant moral decline. Gonzalez Tapia (2021) in research conducted in Adventist churches in the Colombian Caribbean, found that there is a significant relationship between internal control and the planning done by the treasurers of these churches. It follows that good administration will generate confidence in the economic management of a religious congregation. Mokuo (2009) highlighted the importance of implementing effective management strategies. He advocated for the adoption of robust financial management practices within the Church, cautioning that the absence of an Internal Control System (ICS) could lead to inaccurate financial records, improper handling of Church funds (especially from tithes, offerings, projects, and contributors), and failure to adhere to accounting policies. Sulaiman (2007) suggested that inadequate internal controls or their absence could potentially contribute to instances of fraud and financial mismanagement. Additionally, management depends on financial records to make decisions; therefore, if these are not accurate it could significantly compromise the integrity of the organization.

According to Eko and Hariyanto (2011), internal control refers to a series of strategies implemented by an organization to safeguard its assets from misuse, fraud, and inefficiency. Its primary objectives include maintaining the precision and dependability of financial and operational data, adhering to organizational policies, and assessing the performance of all constituent units. On the other hand, as posited by Sukenti (2023), financial management involves the efficient administration of funds, which implies the efficient allocation of resources among various investment channels and the effort to obtain funds for efficient investment or consumption purposes. considers financial management as the effort to obtain funds at minimum cost and use them efficiently. The main objective of this research is to determine whether internal control significantly predicts financial management in the Treasury Department of a Religious Organization in the Caribbean.

Literature review

Internal control and financial management play pivotal roles in organizational governance and long-term viability. The subsequent section provides an examination of the relevant literature on these essential elements.

In the Caribbean context, Bowrin (2004) conducted research describing the nature of internal controls in Christian and Hindu religious organizations in Trinidad and Tobago, assessing the relative completeness of internal controls among the religious organizations evaluated. He found that although these organizations implemented some form of effective internal control, they still had inadequate internal control systems, implying that there are still areas for improvement in the quality of these internal controls. Steinhoff (2005) defines internal control as the application of an organization’s plans, methods, and protocols to achieve its goals. Apart from safeguarding assets, these measures also serve to prevent and detect errors, fraud, inefficiencies, misuse, and inadequate management. Cuomo (2005) argues that internal controls involve a set of guidelines and methods aimed at protecting an organization´s assets, ensuring accurate financial reporting, promoting compliance with legal requirements, and facilitating efficient operations. Widyaningsih (2015) supports this view, describing internal control as a crucial set of ongoing procedures and actions strategically planned to assist an organization in achieving its goals competently and productively. This includes ensuring accurate financial reporting, securing assets, and complying with legal requirements. Internal control encompasses interconnected elements such as the control atmosphere, hazard evaluation, supervising, and others.

Brigham and Houston (2011) assert that financial management involves making decisions concerning the acquisition of assets, methods for acquiring the necessary funds for asset procurement, and strategies for optimizing the firm’s value. This is a special ability that is of utmost importance. Amaka (2012) describes financial management as a process that comprises the planning, organization, coordination, and regulation of an organization’s activities. According to Tanui, Omare, and Bitange (2016), financial management is an essential skill that is needed in all institutions. Finances are the backbone of any organization and therefore require good management of these scarce resources. According to Fairfax County of Virginia publication (2008), sound financial management can be achieved by management looking at the following: planning policy adherence, annual budgets, cash management, internal controls, and inventory management.

Wakiriba, Ngahu, and Wagoki (2014) explored the impact of control measures on financial management in Mirangine Sub County, Nyandarua County. Inadequate financial control mechanisms were identified as leaving the public sector susceptible to vulnerabilities, such as inaccurate financial statements, asset loss, poor management, and unreliable financial records. The research indicated that implementing and enforcing systems of internal control could improve financial management. Using a descriptive research design, the study aimed to evaluate the influence of internal controls on financial management in Mirangine Sub County’s public sector. The target population comprised personnel in finance, accounting, and administration. A focused survey was provided to 30 individuals from relevant departments, demonstrating instrument reliability with a Cronbach’s alpha coefficient exceeding 0.7 (α ≥ 0.7). The findings revealed a positive correlation between control measures and prudence (r = 0.394, p < 0.01) and accountability (r = 0.348, p < 0.01), indicating a positive relationship between control activities and financial management.

Sanusi, Johari, Said, and Iskandar (2015) researched to assess the effectiveness of internal control systems, financial management practices, and accountability procedures in Malaysian mosques. Cases involving the improper handling of institutionally generated funds were subsequently linked to mosques. In their study, Alim and Abdullah (2010) highlight several factors concerning the management control system within mosques, including issues such as deficient accountability in financial management, limited budget involvement, inadequate income tracking and reporting, and the need for more efficient income generation methods within these religious institutions. The study aimed to explore how budget preparation, internal control systems, fund utilization, and accountability influence financial management practices in mosques. The research approach adopted was quantitative and exploratory in nature. Data were collected through a questionnaire administered to respondents. The study population comprised 250 mosques located in Malaysia, with 500 questionnaires distributed. Out of these, 211 fully completed surveys were gathered, achieving a 42.2% response rate. The results displayed correlations between the independent and dependent variables. Positive associations were noted between budget participation (r = 0.313), internal control (r = 0.359), fund utilization (r = 0.405), and accountability (r = 0.279) concerning financial management practices, with a significance level of p ˂ 0.05. Additionally, the analysis revealed a significant connection between the internal control variable and financial management practices, supported by a value below 0.05.

Ibrahim, Diibuzie, and Abubakari (2017) conducted a study to evaluate how internal control influenced the financial performance of five health institutions in the Upper West Region of Ghana. This research was motivated by the less-than-satisfactory outcomes resulting from policymakers’ continuous efforts to enhance the internal control system within the Ministry of Health and its subsequent effects on the financial performance of these health institutions. The research employed an ordered logistic regression model. To meet the recommended 10% to 30% sample size from the target population, fifty persons participated under the technique of purpose sampling. The findings revealed that among the internal control variables, three had significant impacts on financial performance. Internal audit, control activities, and monitoring showed significantly positive coefficients with p-values of 0.018, 0.038, and 0.007, respectively. Consequently, the research concluded that internal controls significantly influence the financial performance of institutions of health in the country of Ghana.

This study seeks to examine if internal control (independent variable) significantly predicts financial management (dependent variable). Internal controls, crucial for safeguarding church assets, form a focal point of investigation. Effective financial management is crucial for the church’s spiritual health as well as its financial well-being. Church leaders must be responsible custodians by overseeing the church’s resources effectively and responsibly. This study will contribute to this effort, ensuring the prudent management of these resources.

Figure 1.

Research model.

Figure 1.

Research model.

2. METHODOLOGY

The type of research is a quantitative and predictive attempt. The study involved 733 treasurers affiliated with churches from a religious community in the Caribbean, surveyed between November 2022 and March 2023. The type of sampling used for this research was non-probabilistic and quota because treasurers from five territories were selected and distributed as follows: North-East Jamaica Conference = 100, North Jamaica Conference = 80, East Jamaica Conference = 105, West Jamaica Conference = 240, and Central Jamaica Conference = 208. The sample was made up of 147 church treasurers representing 20.05% of the population and has the following characteristics: (a) with age, under 18 years, 2%; from 18 to 35 years, 14.3%; from 36 to 50 years, 43.5% and over 50 years, 40.1%; (b) for sex, 72.8% are women and 27.2% are men; (c) Concerning academic level, 19.7% have a diploma of basic studies, 46.3% have a bachelor’s degree, 17% have other types of studies, and a similar 17% have no previous studies. To collect data, a survey developed by Njeri (2014) and Ofori (2011) was modified, employing a Likert scale that ranges from 1 (strongly disagree) to 5 (strongly agree). The questionnaire comprised 37 statements organized into five dimensions for Internal Control: Control environment (CE), risk assessment (RA), control activities (CA), information and communication (IC), and monitoring (M); and other five dimensions for Financial Management: Policy adherence (PA), annual budgets (AB), cash management (CM), inventory management (IM), and information systems (IS).

The instrument’s reliability was assessed using Cronbach’s alpha for each variable: (a) internal control scored .956, and (b) financial management scored .932.

3. RESULTS

In this section, the result of the arithmetic means, and standard deviation of each construct and its items are presented. By analyzing the answers provided by 147 church treasurers, an arithmetic mean was obtained for internal control (M = 4.30, S = .62091) and financial management (M = 4.31, S = .62132).

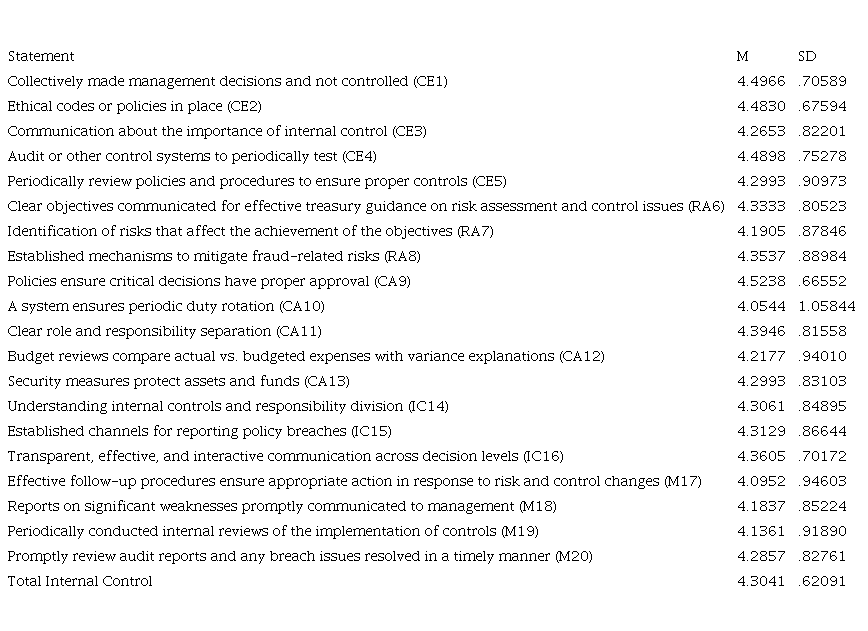

To deepen the study of how the treasurers work practically, the variables that were investigated, and the arithmetic means of the statements were obtained. Within these statements, it is noticeable that the internal control’s lowest aspect involves the endorsement of policies and procedures (CA9), while the highest aspect pertains to management decisions (CE1) (see Table 1).

Table 1

Arithmetic Means of Internal Control

| Statement | M | SD |

| Collectively made management decisions and not controlled (CE1) | 4.4966 | .70589 |

| Ethical codes or policies in place (CE2) | 4.4830 | .67594 |

| Communication about the importance of internal control (CE3) | 4.2653 | .82201 |

| Audit or other control systems to periodically test (CE4) | 4.4898 | .75278 |

| Periodically review policies and procedures to ensure proper controls (CE5) | 4.2993 | .90973 |

| Clear objectives communicated for effective treasury guidance on risk assessment and control issues (RA6) | 4.3333 | .80523 |

| Identification of risks that affect the achievement of the objectives (RA7) | 4.1905 | .87846 |

| Established mechanisms to mitigate fraud-related risks (RA8) | 4.3537 | .88984 |

| Policies ensure critical decisions have proper approval (CA9) | 4.5238 | .66552 |

| A system ensures periodic duty rotation (CA10) | 4.0544 | 1.05844 |

| Clear role and responsibility separation (CA11) | 4.3946 | .81558 |

| Budget reviews compare actual vs. budgeted expenses with variance explanations (CA12) | 4.2177 | .94010 |

| Security measures protect assets and funds (CA13) | 4.2993 | .83103 |

| Understanding internal controls and responsibility division (IC14) | 4.3061 | .84895 |

| Established channels for reporting policy breaches (IC15) | 4.3129 | .86644 |

| Transparent, effective, and interactive communication across decision levels (IC16) | 4.3605 | .70172 |

| Effective follow-up procedures ensure appropriate action in response to risk and control changes (M17) | 4.0952 | .94603 |

| Reports on significant weaknesses promptly communicated to management (M18) | 4.1837 | .85224 |

| Periodically conducted internal reviews of the implementation of controls (M19) | 4.1361 | .91890 |

| Promptly review audit reports and any breach issues resolved in a timely manner (M20) | 4.2857 | .82761 |

| Total Internal Control | 4.3041 | .62091 |

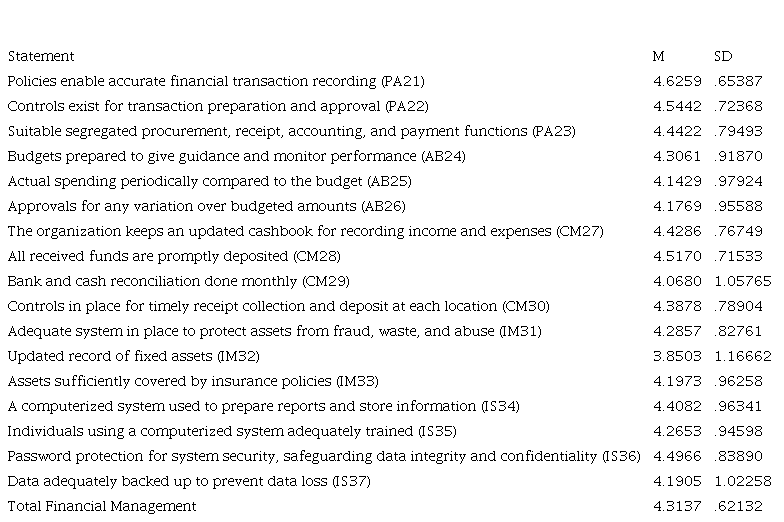

For financial management, the lowest statement is that of controls that serve for the preparation and approval of transactions (PA22) while the highest statement is policies for the appropriate recording of financial transactions (PA21) (see Table 2).

Table 2

Arithmetic Means of Financial Management

| Statement | M | SD |

| Policies enable accurate financial transaction recording (PA21) | 4.6259 | .65387 |

| Controls exist for transaction preparation and approval (PA22) | 4.5442 | .72368 |

| Suitable segregated procurement, receipt, accounting, and payment functions (PA23) | 4.4422 | .79493 |

| Budgets prepared to give guidance and monitor performance (AB24) | 4.3061 | .91870 |

| Actual spending periodically compared to the budget (AB25) | 4.1429 | .97924 |

| Approvals for any variation over budgeted amounts (AB26) | 4.1769 | .95588 |

| The organization keeps an updated cashbook for recording income and expenses (CM27) | 4.4286 | .76749 |

| All received funds are promptly deposited (CM28) | 4.5170 | .71533 |

| Bank and cash reconciliation done monthly (CM29) | 4.0680 | 1.05765 |

| Controls in place for timely receipt collection and deposit at each location (CM30) | 4.3878 | .78904 |

| Adequate system in place to protect assets from fraud, waste, and abuse (IM31) | 4.2857 | .82761 |

| Updated record of fixed assets (IM32) | 3.8503 | 1.16662 |

| Assets sufficiently covered by insurance policies (IM33) | 4.1973 | .96258 |

| A computerized system used to prepare reports and store information (IS34) | 4.4082 | .96341 |

| Individuals using a computerized system adequately trained (IS35) | 4.2653 | .94598 |

| Password protection for system security, safeguarding data integrity and confidentiality (IS36) | 4.4966 | .83890 |

| Data adequately backed up to prevent data loss (IS37) | 4.1905 | 1.02258 |

| Total Financial Management | 4.3137 | .62132 |

Simple regression assumptions

There are four assumptions to test in simple regression (Hair, Anderson, Tatham, and Black, 2007) which are the following: (a) linearity of this case, (b) independence of the error terms, (c) homoscedasticity, (d) normality of the residuals and normality test.

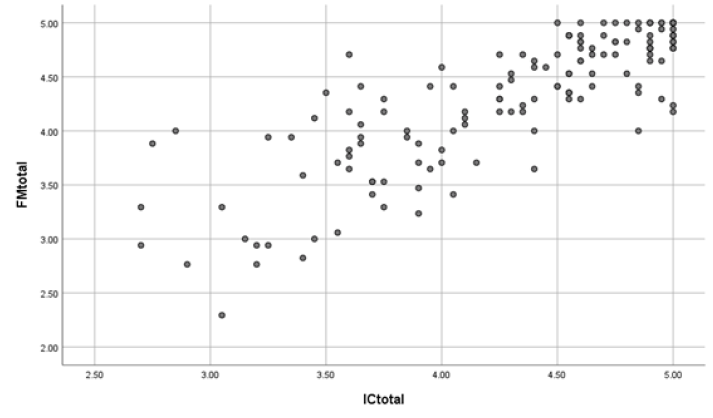

a) In this study, the initial aspect examined was the correlation between the independent and criterion variables. The scatter plots revealed a positive association, with points forming a linear pattern (refer to Figure 2).

Figure 2.

Linearity

Figure 2.

Linearity

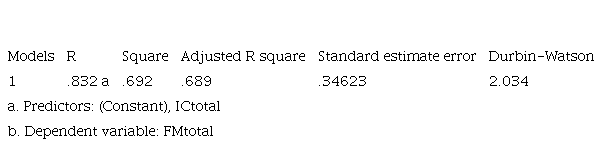

b) The second parameter assessed was the autocorrelation of errors, gauged through the Durbin-Watson statistic (DW = 2.034), falling within the acceptable range of 1.5 to 2.5 which indicates that the errors are uncorrelated and independent (see Table 3).

Table 3

Autocorrelation of errors

| Models | R | R Square | Adjusted R square | Standard estimate error | Durbin-Watson |

| 1 | .832 a | .692 | .689 | .34623 | 2.034 |

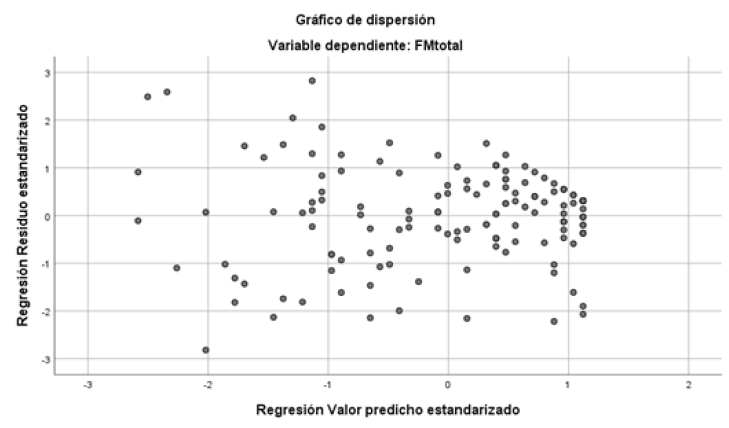

c) As part of the third evaluation, homoscedasticity was examined by assessing the graph of standardized predicted values and the corresponding standardized residuals. The observation indicated the absence of a linear relationship in the residuals, affirming equal variances in errors (refer to Figure 3).

Figure 3.

Homoscedasticity

Figure 3.

Homoscedasticity

d) Table 4 shows that the standardized residuals, in their skewness and kurtosis, are within the range of -1 to 1. So, the standardized residuals tend to have a normal distribution (p > .05), this is corroborated in the Kolmogorov-Smirnov normality test where the value is very close to normality (p = .033).

Table 4

Normal residuals

| Variable | Asymmetry | Kurtosis | Kolmogorov-Smirnov normality |

| Standardized residual of internal control and financial management | -.197 | .531 | p = .033 |

Null hypothesis testing

H0: The level of internal control is not a significant predictor of the level of financial management within the treasury department of a church organization in the Caribbean as perceived by treasurers.

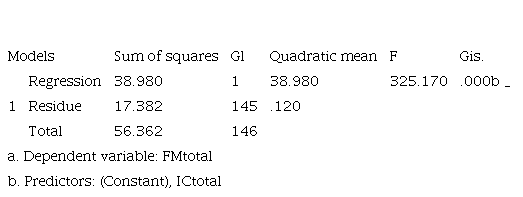

In analyzing the null hypothesis test, the study revealed that the independent variable, internal control, explains 69.2% of the criterion variable, financial management. With a corrected R2 value of 0.689, the ANOVA yielded an F-statistic of 325.170, indicating that R is significantly different from 0 (p = 0.001). Therefore, the significance value shows a direct positive linear correlation between internal control and financial management which confirms that the model is adequate (see Tables 5 and 6).

Table 5

Summary of model b

| Models | R | Square | Adjusted R square | Standard estimate error | Durbin-Watson |

| 1 | .832 a | .692 | .689 | .34623 | 2.034 |

| a. Predictors: (Constant), ICtotal |

| b. Dependent variable: FMtotal |

Table 6

ANOVAa -

| Models | Sum of squares | Gl | Quadratic mean | F | Gis. |

| 1 | Regression | 38.980 | 1 | 38.980 | 325.170 | .000b _ |

| Residue | 17.382 | 145 | .120 | | |

| Total | 56.362 | 146 | | | |

| a. Dependent variable: FMtotal |

| b. Predictors: (Constant), ICtotal |

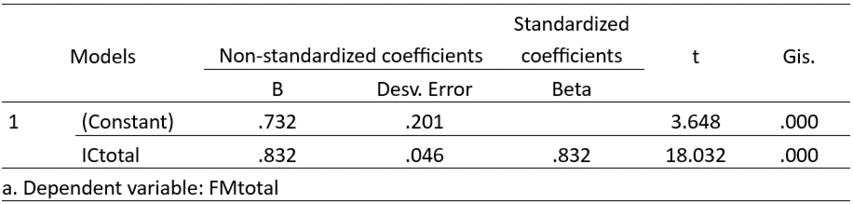

On the other hand, Table 7 presents the non-standardized coefficient Bk obtained from simple regression: B0 is .732, and B1 is .832, both significant. Using these values, the regression equation can be formulated through the least squares method.

Financial management = .732 + .832 (internal control)

Table 7

Coefficients a

4. DISCUSSION

The objective of this research was to determine whether internal control is a significant predictor of financial management in the treasury department of a Caribbean religious organization. The results of the regression model show that internal control significantly predicts financial management (R = 0.832, R² = 0.692). The treasurers’ perception of internal control explains 69.2% of the variance in financial management, indicating that internal control management about financial management is substantial.

Nalle et al. (2023) explicate that within the domain of religious organizations, internal control constitutes a structured framework meticulously crafted to guarantee the effective, efficient, and regulatory-compliant execution of organizational operations. In the analysis conducted by Miiro (2013) in a similar church setting in Uganda, simple linear regression was employed to investigate internal control dimensions, revealing comparable results that significantly impact financial management. However, the effect sizes associated with each dimension were considered small. In contrast, the present research addressed the internal control construct, integrating all dimensions (Internal Control: Control environment (CE), risk assessment (RA), control activities (CA), information and communication (IC), and monitoring (M); and other five dimensions for Financial Management: Policy adherence (PA), annual budgets (AB), cash management (CM), inventory management (IM), and information systems (IS)) and exhibited an effect size greater than 0.35, categorized as high. A distinctive aspect is that, while in Miiro’s research, the participants were administrators without direct involvement in church financial matters, this study involved those responsible for the management of church resources.

In addition, it was found that, according to the perception of the participating treasurers, there is a level of implementation of internal control and financial management of 86%, indicating a high level in both cases. In contrast, the Miiro study in Uganda revealed that the participants had a 73% perception of internal control and 64% perception of financial management, values that indicate relatively lower levels compared to those obtained in the present study.

Iradukunda and Kamande (2022) conducted a study aimed at examining the contribution of the internal control system to financial performance in the Rwandan banking sector. The results revealed that the components of internal control, specifically control activities, control environment, and risk assessment, exert a significant impact on the financial performance of GT Bank Plc in Rwanda. In the present study, the regression analysis model allows identifying a positive correlation between the two constructs, highlighting the importance of having sound internal control systems to achieve efficient financial management. This finding supports the assertions of Gao (2019), who argues that internal control quality and financial performance are positively correlated. However, the intensity of this impact varies across industries. Gao suggests that organizations should improve the allocation of human, financial, and material resources toward internal control to maximize its positive effect on improving business performance.

Furthermore, Oyetunji et al. (2021) revealed that the impact of internal control practices on budgetary control, a dimension of financial management, is evident and demonstrates a significant positive influence on budgetary control.

The current research provides a valuable explanation of the internal control and financial management procedures implemented in the treasury departments of a church organization in the Caribbean, which was part of this study. Despite identifying areas for improvement, the high scores obtained indicate a commendable level of financial management and internal control.

5. CONCLUSIONS

The internal control variable in the Caribbean region, as revealed by the study, serves as a notable predictor of improved financial management. The study suggests that as internal control measures are strengthened, there is a corresponding improvement in financial management practices within the treasury department of the religious organization located in the Caribbean that was part of this study.

Church leaders are encouraged to integrate technology into their operations to facilitate transparency among church members through internal control mechanisms. This approach enables congregational stakeholders to access and scrutinize financial management outcomes more readily.

The treasurers of religious institutions must make every effort to implement plans and strategies in a way that respects the loyalty of the members of their religious congregations and generates greater credibility in their overall management.

REFERENCES

Alim, A. P., Abdullah, S. R. 2010. Audit Pengurusan Masjid: Kajian di Daerah Pasir Puteh, Kelantan. Universiti Teknologi Malaysia Institutional Repository: 1-7

Amaka, C. P. (2012). The impact of internal control system on the financial management of an organization (a case study of the Nigeria bottling company plc, Enugu) (Doctoral dissertation, Master’s Thesis). Faculty of Management and Social Sciences Caritas University.

Bowrin, A. R. (2004). Internal control in Trinidad and Tobago religious organizations. Accounting, Auditing & Accountability Journal, 17(1), 121–152. doi:10.1108/09513570410525238.

Brigham, E. & Houston, J. (2011). Fundamentals of Financial Management: Concise Edition. (7th ed.). USA: Cengage Learning.

Cuomo, A. (2005). Internal Controls and Financial Accountability for Not-for-Profit Boards. Retrieved from http://www.oag.state.ny.us/charities/html.

Eko, S., and Hariyanto, E. (2011). Relationship between internal control, internal audit, and organization commitment with good governance: Indonesian Case.

Fairfax County of Virginia (2008). Ten Principles of sound financial management. Retrieved from http://www.fairfaxcounty.gov/dmb/10_principles_sound_financial_management.htm

Gao, J. (2019, November). A research on the correlation between internal control quality and financial performance. In IOP Conference Series: Materials Science and Engineering (Vol.688, No. 5, p. 055043). IOP Publishing.

Gonzalez Tapia, K. F. (2021). Control interno y su relación con el desempeño de los tesoreros, en las iglesias adventistas de la Asociación del Caribe Colombiano, Colombia, 2021.

Greenberg, J. (2018). Employee theft as a reaction to underpayment inequity: The hidden cost of pay cuts. In occupational crime (pp. 99-106). Routledge.

Hair, J., Anderson, R., Tatham, R. y Black, W. (2007). Análisis multivariante (5ª ed.). Madrid: Prentice Hall Iberia.

Hudson, J. W. (1984). Internal controls in the area of finance for local churches.

Ibrahim, S., Diibuzie, G., & Abubakari, M. (2017). The Impact of Internal Control Systems on Financial Performance: The Case of Health Institutions in Upper West Region of Ghana. International Journal of Academic Research in Business and Social Sciences, 7(4), 684-696.

Iradukunda, P., & Kamande, M. (2022). Internal Control System and Financial Performance in Banking Industry: A case of Guaranty Trust Bank-Rwanda. International Journal of Scientific and Research Publications (IJSRP), 12(11), 13108. DOI: http://dx.doi.org/10.29322/IJSRP.12.11.2022.p13108.

Miiro, E. (2013). Internal controls and financial management in faith-based organizations: A case study of Seventh-Day Adventists Church Central Uganda Conference (Doctoral dissertation, Uganda Management Institute).

Mokuo, O. (2009). Sustainability of Church managed projects: A case of Kenya Evangelical Lutheran Church in Nairobi. Journal of Research Abstracts 3.

Mohamed, I. S., Ab Aziz, N. H., Masrek, M. N., & Daud, N. M. (2014). Mosque fund management: issues on accountability and internal controls. Procedia-Social and Behavioral Sciences, 145, 189-194.

Nalle, H. M., Pradnyani, N. L. P. S. P., & Wasita, P. A. A. (2023). Accountability and Internal Control of Religious Organizations (Study on GKPB Immanuel Tabanan). International Journal of Pertapsi, 1(1), 21-31.

Njeri, C. K. (2014). Effect of Internal Controls on the Financial Performance of Manufacturing Firms in Kenya. Unpublished Master’s Dissertation, University of Nairobi.

Ofori, W. (2011). Effectiveness of Internal Controls: A Perception or Reality? The Evidence of Ghana Post Company Limited in Ashanti Region. A thesis submitted to the Institute of Distance Learning, Kwame Nkrumah University of. Retrieved from http://dspace.knust.edu.gh/bitstream/123456789/4435/1/WILLIAM%20OFORI%20FINAL%20THESIS%202011.pdf

Oyetunji, O. T., Lawal, B. A., Yinus, S. O., Akodu, A. A., & Lawal, B. O. (2021). Internal control practices and financial management of local governments: a quantitative framework approach. African Multidisciplinary Journal of Development, 10(2), 42-54

Sanusi, Z. M., Johari, R. J., Said, J., & Iskandar, T. (2015). The Effects of Internal Control System, Financial Management and Accountability of NPOs: The Perspective of Mosques in Malaysia. Procedia Economics and Finance, 28, 156-162.

Steinhoff, J. C. (2005). Financial Management: Effective Internal Control is Key to Accountability. United States Government Accountability Office.

Sukenti, S. (2023). Financial Management Concepts: A Review. Journal of Contemporary Administration and Management (ADMAN), 1(1), 13-16.

Sulaiman, M. (2007). The internal control procedures of mosques in Malaysia. Revista Universo Contábil, 3(2), 101-115.

Tanui, P. J., Omare, D., & Bitange, J. B. (2016). Internal Controls system for financial management in the church: a case of protestant churches in Eldoret municipality, Kenya. European Journal of Accounting, Auditing, and Finance Research, 4(6), 29-46.

Wakiriba, J. W., Ngahu, S., & Wagoki, J. (2014). Effects of financial controls on financial management in Kenya’s public sector: A case of National Government departments in Mirangine Sub-County, Nyandarua County. Journal of Business and Management, 16(10), 105-115.

Widyaningsih, A. (2015). The influence of the internal control system on the financial accountability of elementary schools in Bandung, Indonesia. Research Journal of Finance and Accounting, 6(24), 89-96.