1. Introduction

Financing decisions remain central to a firm’s strategic management because they determine its ability to invest, expand, and maintain profitability in a competitive environment. Firms particularly large ones expanding operations routinely utilize combinations of short-term and long-term funding sources to support both ongoing operations and capital investments (Chiu, King, & Wang, 2021; Dangl & Zechner, 2021). Managers generally design their financing structures to maximize shareholder wealth while maintaining an optimal balance among risk, cost of capital, and financial flexibility (Frank & Goyal, 2009).

Debt policy and especially the maturity structure of debt has a pervasive impact across risk management, cost of capital, investment capacity, and agency conflicts (Deng & Fang, 2022; Wang, Wang, & Xu, 2023). Firms with significant long-term risky debt may constrain shareholder benefit from positive NPV projects because a greater portion of returns might accrue to debtholders in adverse states (Brogaard, Li, & Xia, 2017; Dangl & Zechner, 2021). Thus, financial managers continuously seek debt structures that maximize shareholder value while managing refinancing, monitoring and rollover risks.

The maturity of corporate debt affects liquidity risk, agency costs, and a firm’s ability to undertake long-horizon investments. Short maturities can enhance monitoring and reduce under-investment or asset substitution risk (Chiu et al., 2021). Whereas longer maturities reduce rollover risk for longer-gestation projects (Harford, Klasa, & Maxwell, 2020; Deng & Fang, 2023). Recent empirical analyses show that firm-specific variables (liquidity, asset tangibility, profitability, size, non-debt tax shields) and macro-financial environment factors (interest-rate term structure, monetary policy stance, refinancing risk) jointly shape maturity decisions in dynamic ways (Crouzet & Tourre, 2024; OECD, 2023).

In Nigeria’s institutional and macroeconomic context, the debt maturity challenge is particularly salient, major shocks such as oil-price declines, exchange rate volatility, and constrained foreign investment have increased refinancing risk for listed firms, especially in the oil & gas sector (Debt Management Office [DMO], 2024; IMF, 2021). The Nigeria DMO’s Medium-Term Debt Management Strategy (2024-2027) highlights the high share of maturing obligations and the need for firms to align debt maturities with asset lifecycles in a volatile fiscal and financial environment.

Many prior Nigeria-focused and sectoral studies on debt maturity use static estimators such as OLS or ARDL and limited control variable sets (Etudaiye-Muhtar et al, 2017; Paseda & Olowe, 2018; Mohammed & Musa-Mubi, 2020). Yet maturity decisions are inherently dynamic current maturity is influenced by past maturity, evolving funding conditions, and endogenous firm characteristics (Flannery & Rangan, 2006; Fabiani, Gambacorta, & Riggi, 2022). Modern panel techniques such as system-GMM are better suited to address unobserved heterogeneity, endogeneity of financing decisions, and dynamic adjustments (Roodman, 2009; Hwang, Lee, & Lee, 2021). Therefore, this study uses a dynamic panel GMM approach and includes an expanded set of firm-level controls (liquidity, asset structure, size, profitability, non-debt tax shields, R&D intensity) to deliver more robust and policy-relevant estimates for Nigerian listed oil & gas firms.

2. Theoretical framework

Contracting-Cost Theory posits that debt maturity serves as a mechanism to mitigate under-investment problems. When firms carry large amounts of long-term debt, shareholders may forgo positive-NPV opportunities because the anticipated returns may flow primarily to debtholders in distress (Myers, 1977; Dangl & Zechner, 2021). Myers proposed responses like reducing debt, embedding covenants, or shortening maturities to alleviate under-investment (Myers, 1977). Stulz (1990) extended this idea by arguing that firms with limited growth opportunities may select longer maturities as a way to reduce monitoring and allow managerial discretion. Empirical studies between 2020 and 2024 have reinforced these dynamics firms with higher growth opportunities and higher monitoring needs often choose shorter maturities to align with asset liquidity and reduce agency risk (Deng & Fang, 2022).

Agency and Monitoring Theory predicts that firms with pronounced agency conflicts or volatile cash flows prefer shorter maturities to increase monitoring and limit creditor exposure, whereas firms with stable cash flows, greater asset tangibility, and stronger relationships with creditors may secure longer-term debt because their rollover and information asymmetry costs are lower (Barclay & Smith, 1995; Chiu et al., 2021). A recent cross-country empirical review confirms that these firm characteristics remain significant determinants of maturity, but their magnitude and direction vary with institutional and macroeconomic environments (Wu, Opare, Bhuiyan, & Habib, 2023; OECD, 2023).

Research consistently shows that firm-level characteristics such as liquidity, profitability, size, asset structure, and non-debt tax shields play critical roles in determining debt maturity structures. In Nigeria, Mohammed and Musa-Mubi (2020) established that non-debt tax shields, liquidity, and asset intensity significantly influence the debt maturity of listed non-financial firms, although profitability showed limited effect. This aligns with Nguyen and Wald’s (2022) findings that larger firms with more tangible assets are more likely to issue long-term bonds, while smaller firms rely more on short-term borrowing. In Ghana, Awunyo-Vitor and Badu (2012) observed similar dynamics, where liquidity and leverage were critical determinants of funding tenor. Likewise, Do and Phan (2022) revealed that Vietnamese firms strategically balance liquidity and investment risk by adjusting maturity to market uncertainty.

Chiu, King, and Wang (2021) found that firms with high liquidity ratios often rely on short-term financing, reflecting their lower refinancing risk and stronger internal cash flow buffers. Alnori (2023) confirmed this pattern for Saudi listed firms, showing profitability and size positively associated with maturity length, while risk indicators shortened maturity. Karim, Chakrobortty, and Bhadra (2022) reported that highly leveraged pharmaceutical firms in Bangladesh face shorter maturities due to creditor aversion to long-term exposure, supporting agency-cost predictions. Similarly, Lemma and Negash (2021) documented that in African markets, asset tangibility and profitability drive longer maturities, while market risk shortens them a finding echoed by Zeitun and Goaied (2022) for Japanese firms during financial turbulence.

Governance and disclosure quality also significantly affect maturity decisions. Gamba and Saretto (2023) emphasized that effective covenant design and transparent reporting reduce monitoring costs, enabling longer-term borrowing. Elsa and Butar (2022) similarly found that earnings management and weak governance constrain firms to short-term debt. Building on this, Harford, Klasa, and Maxwell (2020) demonstrated that firms with stronger liquidity management retain flexibility under refinancing stress.

Recent studies show that macroeconomic and institutional contexts strongly moderate these firm-level relationships. Crouzet and Tourre (2024) found that U.S. firms extend maturities during loose monetary cycles and contract them when policy tightens, confirming that interest-rate expectations drive corporate refinancing strategies. In emerging markets, the OECD (2022, 2023) highlighted that higher global rates and reduced investor appetite for emerging-market debt shorten firm-level maturities, especially where local bond markets are shallow. For Nigeria, the Debt Management Office (2024) noted that maturity concentration remains high, with firms facing liquidity mismatches due to frequent rollovers of short-term debt. These findings mirror Musa, Abdulganiu, and Yahaya (2023), who identified macroeconomic volatility and inflation as significant drivers of corporate debt restructuring among Nigerian non-financial firms.

Additional recent evidence underscores that financial flexibility and innovation capacity shape maturity choices. Nakatani (2023) found that firms with greater intangible assets (which often correlate with R&D-intensity) tend to have greater short-term debt relative to long-term debt, suggesting a preference for shorter maturities, while (Frank and Goyal (2009) observed that firms with strong investment discipline adopt longer maturities, leveraging stable internal financing. (Kim and Park, 2024; Jeenas, 2023) observed during the COVID-19 crisis that firms with better liquidity management and credible disclosure extended debt maturities, contrasting with smaller or opaque firms forced into shorter-term borrowing. Wang, Wang, and Xu (2023) further showed that firms with higher disclosure quality reduce rollover risk through longer-term contracts, reinforcing the governance-maturity linkage.

Several recent African and Asian studies provide deeper empirical support. Khan, Khan, and Khan (2022) reported that firms in emerging economies extend debt maturity when macroeconomic stability improves, but reduce it during inflationary or interest-rate shocks. Deng and Fang (2023) demonstrated that firms adjust maturity cyclically across business cycles, confirming the procyclicality of debt structures. Nguyen (2022) found in Vietnam that firm age, profitability, and asset tangibility are the most significant positive determinants of maturity. Nizam, Shafai, and Asari (2023) confirmed similar results in Malaysia, underscoring regional consistency. Collectively, these findings indicate that firm maturity decisions depend not only on firm fundamentals but also on dynamic macro-financial and institutional conditions.

In the Nigerian context, studies such as Musa et al. (2023) and Mohammed and Musa-Mubi (2020) confirm that size, profitability, and liquidity positively influence maturity structure, while non-debt tax shields have an inverse effect.

H1: Fir-specific characteristics significantly influences the debt maturity structure of listed Oil and Gas Firms in Nigeria

3. Methodology

Ex post facto research design was used as it is suitable because it allows analyzing fact before the commencement of the research. The research utilized secondary data which was derived from yearly statements of all the selected manufacturing firms covering 2012 to 2023. Therefore, the data has been refined and processed, hence it is free from any form of misinformation before it is been published. The selected companies are listed oil & gas companies in Nigeria which are Conoil Plc, Eterna Plc, Japaul Gold & Ventures Plc, Oando Plc, Seplat Energy Plc, Aradel Holdings Plc, Capital Oil Plc and Totalenergies Marketing Nigeria Plc. The research adopts Generalized Method of Moments technique to analyzed the data obtained. In the light of this, the study model debt maturity structure (DSTR) in its functional form as:

DSTR = f (LIQ, ASS, SIZE, PROF, NDT, RSD) (1)

Econometrically, it can be written thus:

Where:

B0 = Constant

DSTR= Debt Maturity Structure (Long Term Debt )

Short-term Debt+ Long-term debt

LIQ= Liquidity

ASS= Asset Structure

SIZE= Firms’ Size

PROF= Profitability

NDT= Non-debt tax shields

RSD= Research and Development

Table 1

Measurment of variables

Authors’ Compilation (2025).

Authors’ Compilation (2025).

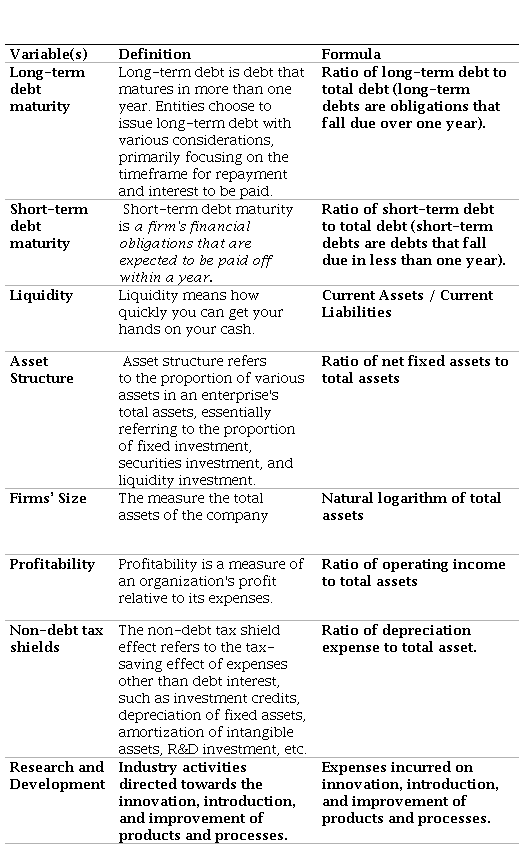

| Variable(s) | Definition | Formula |

| Long-term debt maturity | Long-term debt is debt that matures in more than one year. Entities choose to issue long-term debt with various considerations, primarily focusing on the timeframe for repayment and interest to be paid. | Ratio of long-term debt to total debt (long-term debts are obligations that fall due over one year). |

| Short-term debt maturity | Short-term debt maturity is a firm's financial obligations that are expected to be paid off within a year. | Ratio of short-term debt to total debt (short-term debts are debts that fall due in less than one year). |

| Liquidity | Liquidity means how quickly you can get your hands on your cash. | Current Assets / Current Liabilities |

| Asset Structure | Asset structure refers to the proportion of various assets in an enterprise's total assets, essentially referring to the proportion of fixed investment, securities investment, and liquidity investment. | Ratio of net fixed assets to total assets |

| Firms’ Size | The measure the total assets of the company | Natural logarithm of total assets |

| Profitability | Profitability is a measure of an organization's profit relative to its expenses. | Ratio of operating income to total assets |

| Non-debt tax shields | The non-debt tax shield effect refers to the tax-saving effect of expenses other than debt interest, such as investment credits, depreciation of fixed assets, amortization of intangible assets, R&D investment, etc. | Ratio of depreciation expense to total asset. |

| Research and Development | Industry activities directed towards the innovation, introduction, and improvement of products and processes. | Expenses incurred on innovation, introduction, and improvement of products and processes. |

4. Results and discussion

This part addresses the data presentation and interpretation of results. The section as well as compares the findings with other studies and theories.

4.1 Empirical Results and Discussion

The compiled data from all the countries are shown in below.

Table 1

Descriptive Statistics

Authors’ Computation (2025).

Authors’ Computation (2025).

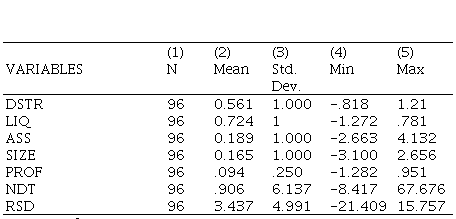

| | (1) | (2) | (3) | (4) | (5) |

| VARIABLES | | N | Mean | Std. Dev. | Min | Max |

| DSTR | | 96 | 0.561 | 1.000 | -.818 | 1.21 |

| LIQ | | 96 | 0.724 | 1 | -1.272 | .781 |

| ASS | | 96 | 0.189 | 1.000 | -2.663 | 4.132 |

| SIZE | | 96 | 0.165 | 1.000 | -3.100 | 2.656 |

| PROF | | 96 | .094 | .250 | -1.282 | .951 |

| NDT | | 96 | .906 | 6.137 | -8.417 | 67.676 |

| RSD | | 96 | 3.437 | 4.991 | -21.409 | 15.757 |

| Number of Companies | | 8 | 8 | 8 | 8 | 8 |

Summary of selected variables of the research are shown in Table 1. The outcomes give the average, standard deviation, lowest, and highest values of all variables for a panel of eight organisations from 2012 to 2023. DSTR, LIQ, ASS, SIZE, PROF, NDT, and RSD were found to have mean values of 0.561, 0.724, 0.189, 0.165, 0.94, 0.906, and 3.437, respectively. The standard deviations of the variables are 1.000, 1, 1.000, 1.000,.250, 6.137, and 4.991, in that order. The variables exhibit a range of values, with the smallest values being -.818, -1.272, -2.663, -3.100, -1.282, -8.417 and -21.409, while the maximum values are 1.21, .781, 4.132, 2.656, .951, 67.676 and 15.757 respectively. This finding illustrates a significant variation across all variables during the specified period. The examination of this significant variation holds considerable value.

Table 2

Correlations Tests

Authors’ Computation (2025).

Authors’ Computation (2025).

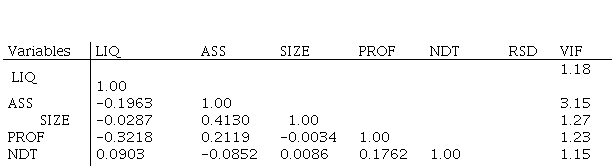

| Variables | LIQ | ASS | SIZE | PROF | NDT | RSD | VIF |

| LIQ | 1.00 | | | | | | 1.18 |

| ASS | -0.1963 | 1.00 | | | | | 3.15 |

| SIZE | -0.0287 | 0.4130 | 1.00 | | | | 1.27 |

| PROF | -0.3218 | 0.2119 | -0.0034 | 1.00 | | | 1.23 |

| NDT | 0.0903 | -0.0852 | 0.0086 | 0.1762 | 1.00 | | 1.15 |

| RSD | -0.2175 | 0.0147 | 0.4311 | 0.1277 | -0.0947 | 1.00 | 1.08 |

Multicollinearity (the interdependence of independent variables) in a multiple regression model leads to biassed coefficient estimations, which taints the regression's outcome. A correlation test was used in this study to determine whether multicollinearity was present. The outcomes of the correlation analysis show that all of the variables are less than 0.5. Likewise, the variance inflation factor outcome reveals that the variables are smaller than 5. Therefore, the variables do not exhibit multicollinearity.

Table 3

Regression for Debt Maturity Structure

Authors’ Computation (2025).***, ** and * indicates 1%, 5% and 10% level of significance respectively

Authors’ Computation (2025).***, ** and * indicates 1%, 5% and 10% level of significance respectively

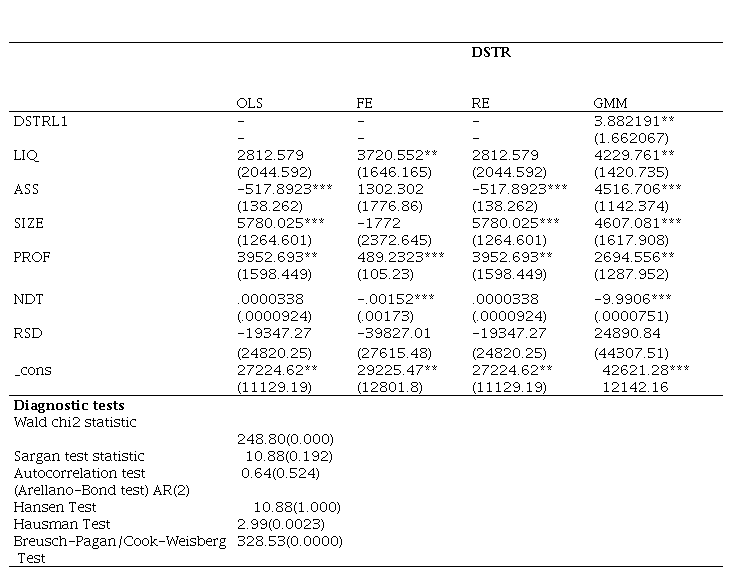

| | | DSTR | |

| OLS | FE | RE | GMM |

| DSTRL1 | - | - | - | 3.882191** |

| - | - | - | (1.662067) |

| LIQ | 2812.579 | 3720.552** | 2812.579 | 4229.761** |

| (2044.592) | (1646.165) | (2044.592) | (1420.735) |

| ASS | -517.8923*** | 1302.302 | -517.8923*** | 4516.706*** |

| (138.262) | (1776.86) | (138.262) | (1142.374) |

| SIZE | 5780.025*** | -1772 | 5780.025*** | 4607.081*** |

| (1264.601) | (2372.645) | (1264.601) | (1617.908) |

| PROF | 3952.693** | 489.2323*** | 3952.693** | 2694.556** |

| (1598.449) | (105.23) | (1598.449) | (1287.952) |

| NDT | .0000338 | -.00152*** | .0000338 | -9.9906*** |

| (.0000924) | (.00173) | (.0000924) | (.0000751) |

| RSD | -19347.27 | -39827.01 | -19347.27 | 24890.84 |

| (24820.25) | (27615.48) | (24820.25) | (44307.51) |

| _cons | 27224.62** | 29225.47** | 27224.62** | 42621.28*** |

| (11129.19) | (12801.8) | (11129.19) | 12142.16 |

| Diagnostic tests | | | | |

| Wald chi2 statistic | 248.80(0.000) | | | |

| Sargan test statistic | 10.88(0.192) | | | |

| Autocorrelation test (Arellano-Bond test) AR(2) | 0.64(0.524) | | | |

| Hansen Test | 10.88(1.000) | | | |

| Hausman Test | 2.99(0.0023) | | | |

| Breusch-Pagan/Cook-Weisberg Test | 328.53(0.0000) | | | |

The effect of firm-specific characteristics on the debt repayment structure of Nigerian listed oil and gas companies was assessed using panel data regression. The results are presented in Table 3. The Breusch-Pagan/Cook-Weisberg (BP) test statistic (χ² = 328.53, p = 0.0000) rejects the null hypothesis of homoskedasticity, indicating the presence of heteroskedasticity in the model. The Hausman test, which assists in choosing the optimal estimator between fixed and random effects, produced a χ² statistic of 2.99 with a p-value of 0.0023. Since the p-value is below the 5% significance threshold, the fixed effects model is preferred to the random effects model, implying that firm-specific effects are correlated with the explanatory variables.

Debt Maturity Structure (DSTR) is the dependent variable, while Liquidity (LIQ), Asset Structure (ASS), Firm Size (SIZE), Profitability (PROF), Non-debt Tax Shields (NDT), and Research and Development (RSD) are the explanatory variables. The results reveal that Firm Size (SIZE), NDT, and RSD are negatively related to DSTR, suggesting that increases in these variables are associated with shorter debt maturities. Conversely, LIQ, ASS, and PROF are positively related to DSTR, implying that firms with higher liquidity, asset tangibility, and profitability tend to use longer-term debt.

For the fixed effects model, Liquidity (LIQ), Profitability (PROF), and Non-debt Tax Shields (NDT) are statistically significant, as indicated by their coefficients (3720.552, 489.2323, and 0.00152, respectively) and corresponding standard errors (1646.165, 105.23, and 0.00173). The significance of these variables implies that a one-unit increase in Liquidity and Profitability leads to an increase in the likelihood of long-term debt maturity by 3720.552 and 489.2323 units, respectively, while a one-unit increase in NDT reduces DSTR by 0.00152 units.

The Generalized Method of Moments (GMM) result shows consistent and efficient estimates and to address potential endogeneity and autocorrelation problems commonly associated with static panel estimators such as OLS, Fixed Effects (FE), and Random Effects (RE) (Arellano & Bond, 1991; Blundell & Bond, 1998). GMM is particularly appropriate for dynamic models where the lagged dependent variable (DSTRL1) appears among the regressors, as it uses lagged levels and differences of the endogenous variables as instruments, thereby mitigating simultaneity bias and unobserved heterogeneity (Roodman, 2009).

A comparison of results across the four estimators (OLS, FE, RE, and GMM) shows that GMM provides more robust and statistically valid estimates. The lagged debt maturity variable (DSTRL1) is positive and significant at the 5% level under GMM, confirming the dynamic nature of debt maturity decisions an effect that the OLS, FE, and RE estimators fail to capture. In addition, the diagnostic results support the reliability of the GMM model. The Sargan test statistic (10.88, p = 0.192) and Hansen test (p = 1.000) indicate that the instruments are valid and not overidentified, while the Arellano-Bond AR(2)test (p = 0.524) confirms the absence of serial correlation. The Wald chi-square statistic (248.80, p = 0.000) further indicates that the overall model is significant.

These findings demonstrate that GMM outperforms OLS, FE, and RE estimators in terms of efficiency and consistency. For instance, while the static estimators (OLS, FE, RE) suggest mixed significance among firm-level variables, the GMM results reveal that Liquidity (LIQ), Asset Structure (ASS), Firm Size (SIZE), and Profitability (PROF) exert significant positive effects on DSTR, in line with theoretical expectations that larger, more liquid, and more profitable firms can secure long-term financing (Ozkan, 2000; Antoniou et al., 2006). The improvement in significance and stability of coefficients under GMM implies that the static models likely suffered from omitted variable bias or simultaneity.

The GMM estimation results are consistent with earlier empirical studies that affirm the influence of firm-specific characteristics on debt maturity structure in developing markets (Etudaiye-Muhtar et al, 2017; Paseda & Olowe, 2018; Mohammed & Musa-Mubi, 2020). The validity of the diagnostic tests and the dynamic nature of the model confirm that GMM is the most appropriate estimator for examining the debt maturity structure of Nigerian oil and gas companies. Therefore, the study concludes that firm characteristics particularly liquidity, profitability, and firm size are significant determinants of firms’ debt maturity choices, reinforcing the role of internal financial health and asset structure in shaping long-term financing behavior.

5. Conclusions

The research determines that liquidity impact significantly on debt maturity structure. It was also concluded that asset structure significantly impacts debt maturity structure. The research also concludes that firm size and profitability have significant impact on debt maturity structure. Finally, it was concluded that firms’ characteristics have significant impact on debt maturity structure of listed oil and gas firms in Nigeria. The research therefore indicates that the management of companies should pursue efficiency in order to reduce the usage of debt in the capital structure option. Future researches should consider the effect of institutional quality on debt repayment structure of firms in Nigeria. This is because institutional environment influences the loanable funds in the economy. In addition, the future researches can consider macroeconomic variables and debt repayment structure of firms in Nigeria.

7. Referencias

Alnori, F. (2023). Corporate investment, financial structure and debt maturity: New evidence from Saudi Arabia. International Journal of Economics and Financial Issues, 14(5), 262-268.

Antoniou, A., Guney, Y., & Paudyal, K. (2006). The determinants of debt maturity structure: Evidence from France, Germany and the UK. European Financial Management, 12(2), 161-194.

Arellano, M., & Bond, S. (1991). Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Review of Economic Studies, 58(2), 277-297.

Awunyo-Vitor, D., & Badu, J. (2012). Capital structure and performance of listed banks in Ghana. Global Journal of Human-Social Science Research, 12(5). 57-62.

Barclay, M. J., & Smith, C. W., Jr. (1995). The maturity structure of corporate debt. Journal of Finance, 50(2), 609-631.

Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115-143.

Brogaard, J., Li, D., & Xia, Y. (2017). Stock liquidity and default risk. Journal of Financial Economics, 124, 486-502.

Chiu, W.-C., King, T.-H. D., & Wang, C.-W. (2021). Debt maturity dispersion and the cost of bank loans. Journal of Corporate Finance, 70(C), 1-21.

Crouzet, N., & Tourre, F. (2024). Corporate debt maturity matters for monetary policy (IFDP No. 1402). Board of Governors of the Federal Reserve System.

Dangl, T., & Zechner, J. (2021). Debt maturity and the dynamics of leverage. Review of Financial Studies, 34(12), 5796-5840.

Debt Management Office, Federal Republic of Nigeria. (2024). Nigeria’s medium-term debt management strategy (MTDS) 2024-2027.

Deng, M., & Fang, M. (2022). Debt maturity heterogeneity and investment responses to monetary policy. European Economic Review, 144(2022), 1-23.

Deng, M., & Fang, M. (2023). Corporate debt maturity and business-cycle fluctuations. European Economic Review, 152, (2023), 1-53.

Do, T. V. T., & Phan, D. T. (2022). Debt maturity structure and investment decisions: Evidence of listed companies on Vietnam’s stock market. Cogent Economics & Finance, 10(1), 1-12.

Elsa, T., & Butar, S. B. (2022). Determinants of debt maturity structure: Evidence from Indonesian companies. Jurnal Akuntansi Bisnis, 20(1), 17-28.

Etudaiye-Muhtar, O. F., Ahmad, R., & Matemilola, B. T. (2017). Corporate debt maturity structure: The role of firm-level and institutional determinants in selected African countries. Global Economic Review, 46(4), 422-440.

Fabiani, A., Gambacorta, L., & Riggi, M. (2022). Corporate debt maturity and monetary policy transmission (IFDP No. 1409). Board of Governors of the Federal Reserve System.

Flannery, M. J., & Rangan, K. P. (2006). Partial adjustment toward target capital structures. Journal of Financial Economics, 79(3), 469-506.

Frank, M. Z., & Goyal, V. K. (2009). Capital structure decisions: Which factors are reliably important? Financial Management, 38(1), 1-37.

Gamba, A., & Saretto, A. (2023). Debt maturity and commitment on firm policies (Working Paper No. 2303). Research Department, Federal Reserve Bank of Dallas.

Harford, J., Klasa, S., & Maxwell, W. F. (2020). Refinancing risk and cash holdings. Journal of Financial Economics, 136(2), 532-553.

Hwang, J., Lee, S., & Lee, Y. (2021). A doubly corrected robust variance estimator for linear GMM. Journal of Econometrics, 229(2), 276-298.

Jeenas, P. (2023). Monetary policy, liquidity risk, and corporate debt structure. Journal of Financial Economics, 149(2), 456-479.

Karim, R., Chakrobortty, T., & Bhadra, H. (2022). Impact of firm’s leverage on financial performance: Evidence from the pharmaceuticals industry of Bangladesh. Business Review, 17(1), 16-34.

Khan, M. K., Khan, K., & Khan, S. (2022). Determinants of debt maturity: Evidence from emerging economies. Emerging Markets Finance and Trade, 58(11), 3112-3128.

Kim, M., & Park, G. (2024). Corporate debt maturity and output price dynamics [Unpublished manuscript]. Retrieved from https://minseogkim.github.io/files/Kim_JMP_Debt_Maturity_Output_Price_Dynamics.pdf

Lemma, T. T., & Negash, M. (2021). Debt maturity choice of a firm: Evidence from African countries. Journal of Business & Policy Research, 7(2), 60-92.

Mohammed, L., & Musa-Mubi, A. (2020). Firm-specific determinants of debt maturity structure of listed non-financial firms in Nigeria. Malaysian Management Journal, 24, 77-102.

Musa, A. B., Abdulganiu, M., & Yahaya, A. (2023). Relationship between macroeconomic factors and debt structure: Evidence from non-financial firms in Nigeria. International Journal of Intellectual Discourse, 6(2), 1-11.

Myers, S. C. (1977). Determinants of corporate borrowing. Journal of Financial Economics, 5(2), 147-175.

Nguyen, K. (2022). Determinants of debt maturity structure: Evidence in Vietnam. Cogent Business & Management, 9(1), 1-27.

Nakatani, R. (2023). Debt maturity and firm productivity: The role of intangibles (MPRA Paper No. 116172). Munich Personal RePEc

Nizam, B. H. B., Shafai, N. A., & Asari, F. F. A. H. (2023). Determinants of capital structure: An analysis of listed firms in Malaysia. International Journal of Accounting, 8(48), 72-81.

OECD. (2023). OECD sovereign borrowing outlook 2023. OECD Publishing.

Ozkan, A. (2000). An empirical analysis of corporate debt maturity structure. European Financial Management, 6(2), 197-212.

Paseda, O. A., & Olowe, R. A. (2018). The debt maturity structure of Nigerian quoted firms. Lagos Journal of Banking, Finance & Economic Issues, 4(1), 51-96.

Roodman, D. (2009). How to do xtabond2: An introduction to difference and system GMM in Stata. The Stata Journal, 9(1), 86-136.

Stulz, R. M. (1990). Managerial discretion and optimal financing policies. Journal of Financial Economics, 26(1), 3-27.

Wang, S., Wang, X., & Xu, L. (2023). Debt maturity structure and the quality of risk disclosures. Journal of Corporate Finance, 83(C), 1-26.

Wu, J. Y., Opare, S., Bhuiyan, M. B. U., & Habib, A. (2022). Determinants and consequences of debt maturity structure: A systematic review of the international literature. International Review of Financial Analysis, 48(2022), 1-28.

Zeitun, R., & Goaied, M. (2022). The nexus between debt structure, firm performance, and the financial crisis: Non-linear panel data evidence from Japan. Applied Economics, 54(40), 4681-4699.

(2)

(2)