1. Introduction

Economic resilience, characterized as the ability of an economy to withstand, adapt to, and recover from external shocks, is a critical factor for long-term stability and sustainable growth (Briguglio, 2016). In an increasingly interconnected global economy, disruptions such as financial crises, natural disasters, and pandemics can have far-reaching effects, particularly on developing regions, which are often more vulnerable due to structural deficiencies and limited resources (Diop et al., 2021; Hossaini et al., 2024). Understanding how different regions build and maintain economic resilience is critical for policymakers seeking to promote sustainable development and mitigate the adverse effects of such shocks. This study builds on the work of researchers such as Lian and Li (2024) and Dahmani and Makram (2024), who have emphasized the importance of factors such as financial stability, human capital development, and sustainable growth drivers in promoting economic resilience. For example, Lian and Li (2024) emphasize the role of renewable energy and technological innovation in reducing environmental footprints, while Dahmani and Makram (2024) argue that financial stability is essential for sustained economic growth, particularly in sub-Saharan Africa.

This study examines the economic resilience of four regions: Eastern and Southern Africa, Western and Central Africa, Latin America and the Caribbean, and Sub-Saharan Africa. These regions were chosen because of their diverse economic structures, varying levels of integration into the global economy, and different obstacles to economic stability. For example, many regions are heavily dependent on commodity exports, while others have more diversified economies. Their institutional frameworks, governance effectiveness, and policy responses to disturbances also vary widely. The differences between these regions illustrate the complex nature of economic resilience, as evidenced by research by Henri (2019), Rasheed and Tahir (2024), and Husain (2024), all of which emphasize the importance of governance, debt management, and foreign direct investment (FDI) in enhancing resilience.

The current literature often assesses economic resilience, but generally neglects significant regional differences, especially in comparisons involving developing regions (Spratt & Ber-nini, 2010). Most studies focus on specific countries or overarching global patterns, resulting in a lack of understanding of how resilience emerges in regions with different economic characteristics. This study seeks to fill this vacuum by analyzing economic resilience in the selected regions using three primary indicators: GDP growth stability, total debt service, and foreign direct investment (FDI) inflows. These variables were chosen because they represent a region's ability to sustain economic development, meet financial obligations, and attract foreign investment, all essential elements of resilience (Onafowora & Owoye, 2019; Mohamud & Warsame, 2024). The research is particularly timely in light of global challenges that have highlighted the vulnerability of developing economies and the need for resilient systems that can withstand such shocks (Armah, 2022).

By comparing these locations, this study aims to uncover trends, strengths, and vulnerabilities in economic resilience, thereby increasing understanding of how different economic structures and policies affect resilience outcomes. This research is particularly relevant in the context of global difficulties such as the COVID-19 pandemic, which exacerbated pre-existing vulnerabilities and underscored the need for resilient economic systems (Diop et al., 2021; Hossaini et al., 2024).

2. Literature Review

Economic resilience, characterized as the capacity of an economy to withstand, adjust to, and recover from external shocks, is a complex notion based on different theoretical frameworks. Systems theory views economies as complex systems that can adapt to disturbances, while the notion of "bounce-back capacity" emphasizes recovery after shocks (Briguglio, 2016). Critical elements that enhance resilience include diversity of economic activities, robust institutional frameworks, efficient governance, and availability of external financing (Gnangnon, 2022). Economic diversity and policy adaptability are essential, as emphasized by Briguglio and Piccinino (2012) in their study of East Asia's resilience during the 2008-2009 global recession. Their research created a "growth-with-resilience" (GWR) index to assess how countries withstand shocks while promoting growth, highlighting the importance of economic policies and structural elements.

A stable GDP growth trajectory is often considered a key indicator of resilience, reflecting an economy's ability to withstand external challenges. Onafowora and Owoye (2019) found that foreign direct investment (FDI), domestic investment, and trade openness enhance the stability of GDP growth, while factors such as public debt and inflation pose significant challenges. This is consistent with the findings of Dahmani and Makram (2024), who found that financial stability in Sub-Saharan Africa is crucial to mitigate risks and promote growth, highlighting the role of sound monetary, fiscal, and market policies in building resilience. Similarly, Mohamud and Warsame (2024) suggest that effective debt management is essential for reducing vulnerability to external shocks, a point supported by Henri (2019), who found that debt relief under the HIPC Initiative has long-term benefits but limited short-term impact on growth in Africa.

Debt sustainability is an important measure of an economy's fiscal health. While high debt levels can reduce resilience by limiting fiscal flexibility, effective debt management can enhance resilience in the long run. Vinokurov et al. (2020) found that external shocks, such as the COVID-19 pandemic, can exacerbate debt sustainability challenges in emerging markets. Rasheed and Tahir (2024) also find that sovereign debt crises can severely destabilize economies, with long-term consequences for governance and political stability. They recommend implementing robust debt management frameworks and strengthening institutional governance to prevent such crises and promote economic resilience.

FDI plays a key role in economic resilience by providing capital, technology and expertise. However, its effectiveness depends on factors such as the quality of governance and the institutional framework. Husain (2024) highlights the mixed effects of FDI in the Congo, emphasizing the need for strong institutions and regulatory frameworks to maximize the benefits of FDI. This view is echoed by Talla (2023), who finds that FDI is more impactful when associated with macroeconomic stability and institutional quality in WAEMU countries. Yangailo (2024) adds that FDI in Zambia is hampered by weak institutions and infrastructure, underscoring the importance of an enabling environment for FDI to contribute to resilience.

Despite these contributions, there are significant gaps in the literature. The stability of GDP growth has been extensively studied, but its correlation with other indicators of resilience, such as debt and foreign direct investment (FDI), remains underexplored. The influence of regional economic systems on resilience remains underexplored. While studies such as Gnangnon (2022) highlight the importance of productive capacity, trade openness, and macroeconomic stability in building resilience, there is limited research on how regional economic structures influence resilience outcomes in developing regions. Few studies have directly compared economic resilience across developing regions, and those that do often focus on individual indicators rather than their interaction, limiting their ability to provide a holistic view of resilience (Spratt & Bernini, 2010). Tsiotas and Katsaiti (2024) introduced a multidimensional index to measure global resilience; however, their research did not focus on specific developing regions, highlighting the need for more focused research in this area. The work of Antoniades (2017) shifts the focus to the evolving vulnerability and resilience dynamics between developed and developing countries, highlighting the importance of changing policy space in emerging economies. This study seeks to fill the gap by providing a comparative analysis of economic resilience across four developing regions, integrating the indicators of GDP stability, debt sustainability, and FDI inflows to provide a comprehensive view of resilience dynamics.

The research gap exists due to the lack of studies that directly compare economic resilience across regions, including East and Southern Africa, West and Central Africa, Latin America and the Caribbean, and Sub-Saharan Africa, using a combination of GDP growth stability, total debt service, and foreign direct investment inflows. This study seeks to fill this gap by providing a comparative analysis that emphasizes regional differences and identifies characteristics that promote or hinder resilience. This promotes a deeper understanding of how different economic frameworks and policies affect resilience outcomes in emerging markets. This is particularly relevant for global difficulties such as the COVID-19 pandemic, which exacerbated pre-existing vulnerabilities and underscored the need for resilient economic systems (Diop et al., 2021; Hossaini et al., 2024).

3. Methodology

This study uses a quantitative research design to examine the relationships between economic resilience, debt service, foreign direct investment (FDI) and GDP growth across regions. The study is primarily based on secondary data from reputable global databases such as the World Bank, focusing on the period from 1994 to 2023, with a focus on countries in four key regions: Latin America and the Caribbean; West and Central Africa; East and Southern Africa; and Sub-Saharan Africa. The objective is to identify the factors that influence economic resilience in different regions and to identify the key economic indicators that enhance or hinder resilience. In addition, GDP Growth Stability is calculated as the standard deviation of GDP growth rates over a specified period. The Resilience Score is then derived using the following formula:

Resilience Score=(GDP Growth Stability)−(Total Debt Service % of GNI)+(FDI Inflows) 1

This formula combines the stability of growth, the debt burden, and foreign investment to measure economic resilience. Higher resilience scores indicate economies that are more stable and able to absorb shocks.

The data were analyzed using Jamovi, a statistical software program that supports a variety of statistical tests, including correlation analysis, ANOVA, and regression models. The primary analytical approach involved a series of tests to understand the relationships between economic resilience and the independent variables.

-

Descriptive Statistics: Descriptive statistics (mean, standard deviation, and range) were calculated for GDP growth, debt service, FDI inflows, and resilience scores to provide an overview of the data and explore regional variations.

-

Correlation Analysis: A Pearson correlation analysis was conducted to examine the strength and direction of relationships between the variables (debt service, GDP growth, FDI inflows, and resilience). This helped identify whether significant correlations exist between these variables, such as how debt service might negatively affect resilience or how FDI could positively impact economic stability.

-

ANOVA (Analysis of Variance): ANOVA was used to assess whether there are significant differences in the mean values of the key variables (debt service, GDP growth, FDI inflows) across the four regions. Post-hoc tests were performed (Games-Howell) to identify specific regional differences.

-

Multiple Regression Analysis: To further understand the impact of each independent variable on economic resilience, a multiple regression model was applied. The general regression formula used for the model is:

Resilience Score=β0+β1(Total Debt Service % of GNI) +β2(GDP Growth) +β3(FDI Inflows)+ϵ 2

Where:

• Resilience Score is the dependent variable,

• β0 is the intercept of the regression equation,

• β1,β2,β3 are the regression coefficients for the independent variables,

• Total Debt Service % of GNI\, GDP Growth, and FDI Inflows are the predictors,

• ϵ is the error term representing the residual variance.

4. Results

Correlation Analysis

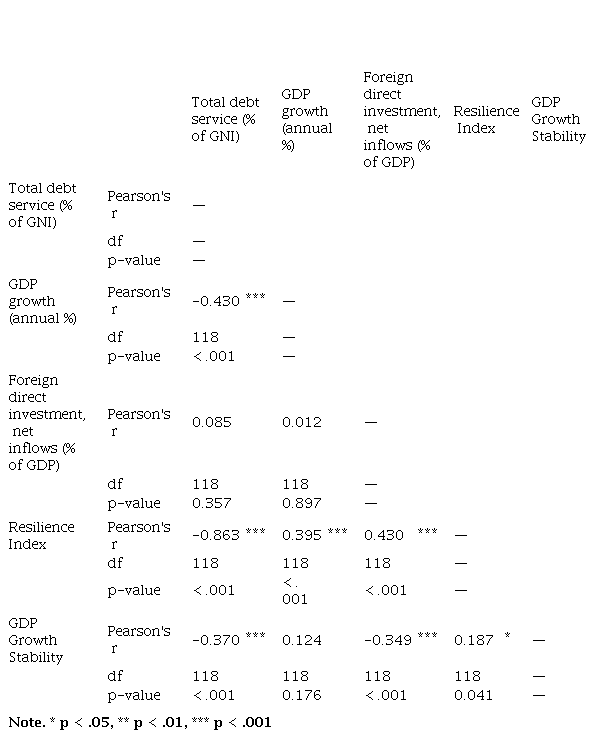

The correlation matrix in Table 1 presents the relationships between key economic variables: total debt service (% of GNI), GDP growth (annual %), net FDI inflows (% of GDP), the resilience index, and GDP growth stability. A strong negative correlation is observed between total debt service and the resilience index (r = -0.863, p < 0.001), suggesting that higher debt service burdens are associated with lower economic resilience. Similarly, total debt service is negatively correlated with GDP growth (r = -0.430, p < 0.001), suggesting that economies with higher debt service tend to experience lower growth rates. In addition, there is a significant negative relationship between total debt service and GDP growth stability (r = -0.370, p < 0.001), suggesting that higher debt service contributes to economic volatility.

Table 1.

Correlation Matrix

| Total debt service (% of GNI) | | Pearson's r | | — | | | | | | | | | |

| | df | | — | | | | | | | | | |

| | p-value | | — | | | | | | | | | |

| GDP growth (annual %) | | Pearson's r | | -0.430 | *** | — | | | | | | | |

| | df | | 118 | | — | | | | | | | |

| | p-value | | < .001 | | — | | | | | | | |

| Foreign direct investment, net inflows (% of GDP) | | Pearson's r | | 0.085 | | 0.012 | | — | | | | | |

| | df | | 118 | | 118 | | — | | | | | |

| | p-value | | 0.357 | | 0.897 | | — | | | | | |

| Resilience Index | | Pearson's r | | -0.863 | *** | 0.395 | *** | 0.430 | *** | — | | | |

| | df | | 118 | | 118 | | 118 | | — | | | |

| | p-value | | < .001 | | < .001 | | < .001 | | — | | | |

| GDP Growth Stability | | Pearson's r | | -0.370 | *** | 0.124 | | -0.349 | *** | 0.187 | * | — | |

| | df | | 118 | | 118 | | 118 | | 118 | | — | |

| | p-value | | < .001 | | 0.176 | | < .001 | | 0.041 | | — | |

| Note. * p < .05, ** p < .01, *** p < .001 |

|

GDP growth has a positive and significant correlation with the resilience index (r = 0.395, p < 0.001), implying that more resilient economies tend to have higher growth rates. However, GDP growth does not show a statistically significant relationship with net FDI inflows (r = 0.012, p = 0.897) or GDP growth stability (r = 0.124, p = 0.176), suggesting that these factors may be influenced by other economic determinants. FDI net inflows are positively correlated with the resilience index (r = 0.430, p < 0.001), suggesting that higher foreign investments contribute to greater economic resilience. However, FDI net inflows exhibit a significant negative correlation with GDP growth stability (r = -0.349, p < 0.001), which may indicate that economies with higher FDI inflows experience greater fluctuations in growth.

The resilience index positively correlates with GDP growth stability (r = 0.187, p = 0.041), though the relationship is weaker compared to other significant correlations. This suggests that economies with higher resilience tend to have more stable growth patterns, albeit with some variations. Overall, the correlation matrix highlights the intricate relationships among debt service, economic growth, foreign investment, and resilience. The findings underscore the importance of managing debt levels and fostering resilience to promote stable economic growth.

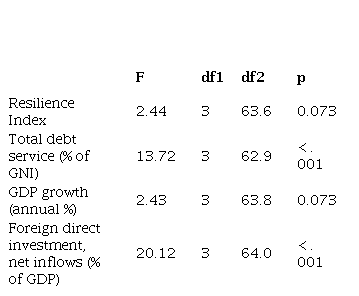

ANOVA

The results from Table 2 show different levels of significance for the four key variables. For the Resilience Index, the F-value is 2.44 with a p-value of 0.073. Since the p-value is above the conventional threshold of 0.05, we cannot reject the null hypothesis, indicating that there is no significant difference in the Resilience Index across regions. This implies that resilience, as measured in this study, does not vary significantly across regions.

Table 2.

One-Way ANOVA (Welch's)

| Resilience Index | | 2.44 | | 3 | | 63.6 | | 0.073 | |

| Total debt service (% of GNI) | | 13.72 | | 3 | | 62.9 | | < .001 | |

| GDP growth (annual %) | | 2.43 | | 3 | | 63.8 | | 0.073 | |

| Foreign direct investment, net inflows (% of GDP) | | 20.12 | | 3 | | 64.0 | | < .001 | |

For total debt service (% of GNI), the F-value is 13.72, with a p-value of less than 0.001, indicating a statistically significant difference between the regions. This suggests that the regions differ in their debt service burden relative to their Gross National Income. The significant difference in total debt service highlights regional disparities that are likely influenced by economic structures, debt management policies and financial conditions in these regions.

Similarly, for GDP growth (annual %), the F-value is 2.43, with a p-value of 0.073, which is above the 0.05 threshold for significance. Therefore, we cannot reject the null hypothesis, which means that there are no significant differences in GDP growth between the regions in the dataset. Despite some differences in growth rates, these differences are not statistically significant at the regional level.

Finally, for FDI, net inflows (% of GDP), the F-value is 20.12, with a p-value of less than 0.001, indicating a highly significant difference across regions. This suggests that regions differ significantly in their ability to attract FDI as a share of GDP. The large F-value and low p-value underscore the importance of foreign investment in the economic landscape of different regions.

Table 3.

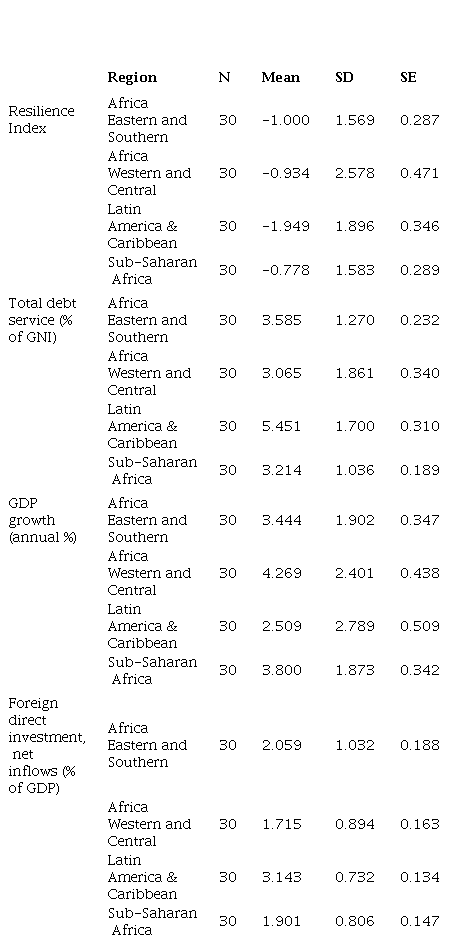

Group Descriptive

| Resilience Index | | Africa Eastern and Southern | | 30 | | -1.000 | | 1.569 | | 0.287 | |

| | Africa Western and Central | | 30 | | -0.934 | | 2.578 | | 0.471 | |

| | Latin America & Caribbean | | 30 | | -1.949 | | 1.896 | | 0.346 | |

| | Sub-Saharan Africa | | 30 | | -0.778 | | 1.583 | | 0.289 | |

| Total debt service (% of GNI) | | Africa Eastern and Southern | | 30 | | 3.585 | | 1.270 | | 0.232 | |

| | Africa Western and Central | | 30 | | 3.065 | | 1.861 | | 0.340 | |

| | Latin America & Caribbean | | 30 | | 5.451 | | 1.700 | | 0.310 | |

| | Sub-Saharan Africa | | 30 | | 3.214 | | 1.036 | | 0.189 | |

| GDP growth (annual %) | | Africa Eastern and Southern | | 30 | | 3.444 | | 1.902 | | 0.347 | |

| | Africa Western and Central | | 30 | | 4.269 | | 2.401 | | 0.438 | |

| | Latin America & Caribbean | | 30 | | 2.509 | | 2.789 | | 0.509 | |

| | Sub-Saharan Africa | | 30 | | 3.800 | | 1.873 | | 0.342 | |

| Foreign direct investment, net inflows (% of GDP) | | Africa Eastern and Southern | | 30 | | 2.059 | | 1.032 | | 0.188 | |

| | Africa Western and Central | | 30 | | 1.715 | | 0.894 | | 0.163 | |

| | Latin America & Caribbean | | 30 | | 3.143 | | 0.732 | | 0.134 | |

| | Sub-Saharan Africa | | 30 | | 1.901 | | 0.806 | | 0.147 | |

In Table 3, the descriptive statistics for the variables reveal some important regional trends. For the Resilience Index, all regions have negative means, with Latin America and the Caribbean having the lowest mean of -1.949, indicating relatively low resilience compared to other regions. The variation in standard deviations (SD) and standard errors (SE) also highlights the different levels of resilience within the regions. Latin America and the Caribbean has the highest SD (1.896), suggesting greater variability in resilience levels.

In terms of total debt service (% of GNI), Latin America and the Caribbean has the highest mean (5.451%), followed by Eastern and Southern Africa (3.585%). Sub-Saharan Africa has the lowest average (3.214%), suggesting that Latin America and the Caribbean has the highest debt service burden relative to its GNI. Variability in debt service burdens is also evident, with regions such as West and Central Africa showing more diverse values.

In terms of GDP growth, the highest average annual growth is reported by Africa West and Central (4.269%), followed by Sub-Saharan Africa (3.800%). On the other hand, Latin America and the Caribbean has the lowest average growth rate (2.509%), reflecting slower economic growth in this region. This difference could be attributed to various macroeconomic factors, including policy differences, market structures and external shocks.

Foreign direct investment (FDI) data show that Latin America and the Caribbean again outperformed other regions, with an average of 3.143%. In contrast, Sub-Saharan Africa has the lowest average (1.901%), suggesting that the region has been less successful in attracting foreign investment. This difference highlights the differences in investment climates and business environments across regions.

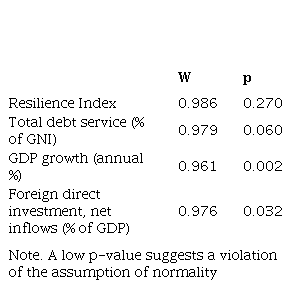

Assumption Checks

Table 4.

Normality Test (Shapiro-Wilk)

| Resilience Index | | 0.986 | | 0.270 | |

| Total debt service (% of GNI) | | 0.979 | | 0.060 | |

| GDP growth (annual %) | | 0.961 | | 0.002 | |

| Foreign direct investment, net inflows (% of GDP) | | 0.976 | | 0.032 | |

| Note. A low p-value suggests a violation of the assumption of normality |

Table 4 shows the results of normality tests for the variables. The Resilience Index and Total Debt Service (% of GNI) have p-values above 0.05, indicating that their distributions are not significantly different from normal. This suggests that these variables are approximately normally distributed and meet the assumptions needed to run an ANOVA.

However, for GDP growth (annual %) and FDI net inflows (% of GDP), the p-values are below 0.05, indicating a violation of the normality assumption. This suggests that the distributions of these variables are not normal, which could affect the reliability of the ANOVA results, as violations of normality can lead to biased estimates and incorrect conclusions.

Table 5.

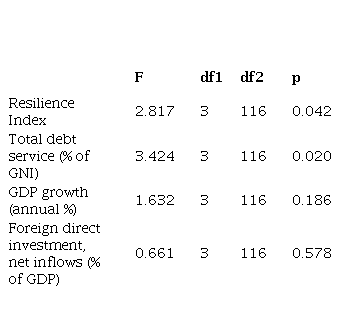

Homogeneity of Variances Test (Levene's)

| Resilience Index | | 2.817 | | 3 | | 116 | | 0.042 | |

| Total debt service (% of GNI) | | 3.424 | | 3 | | 116 | | 0.020 | |

| GDP growth (annual %) | | 1.632 | | 3 | | 116 | | 0.186 | |

| Foreign direct investment, net inflows (% of GDP) | | 0.661 | | 3 | | 116 | | 0.578 | |

|

Table 5 shows the results of Levene's test for homogeneity of variances. For both the Resilience Index and Total Debt Service (% of GNI), the p-values are below 0.05, indicating that the assumption of equal variances across groups is violated for these variables. This suggests that the variation within regions is not consistent and could potentially affect the results of the ANOVA, since the test assumes homogeneity of variances.

For GDP growth and FDI, the p-values are greater than 0.05, indicating that the assumption of homogeneity of variances holds for these two variables. Therefore, the ANOVA results for these two variables are likely to be more reliable as the assumption of equal variances is not violated.

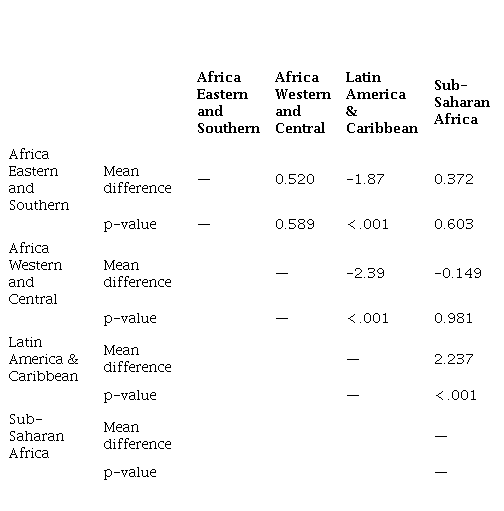

Games-Howell Post-Hoc Test analysis

The Games-Howell post-hoc test in Table 6 shows significant mean differences between certain regions for total debt service (% of GNI). Specifically, Africa East and Southern has a significant mean difference from Latin America and the Caribbean (p < 0.001), with the latter region having a much higher debt service. There is also a significant difference between Africa Western and Central and Latin America & Caribbean, with Latin America again having a higher debt service. However, comparisons between East Africa and Southern and Sub-Saharan Africa, and between West Africa and Central and Sub-Saharan Africa do not show significant differences.

Table 6.

Games-Howell Post-Hoc Test – Total debt service (% of GNI)

| Africa Eastern and Southern | | Mean difference | | — | | 0.520 | | -1.87 | | 0.372 | |

| | p-value | | — | | 0.589 | | < .001 | | 0.603 | |

| Africa Western and Central | | Mean difference | | | | — | | -2.39 | | -0.149 | |

| | p-value | | | | — | | < .001 | | 0.981 | |

| Latin America & Caribbean | | Mean difference | | | | | | — | | 2.237 | |

| | p-value | | | | | | — | | < .001 | |

| Sub-Saharan Africa | | Mean difference | | | | | | | | — | |

| | p-value | | | | | | | | — | |

|

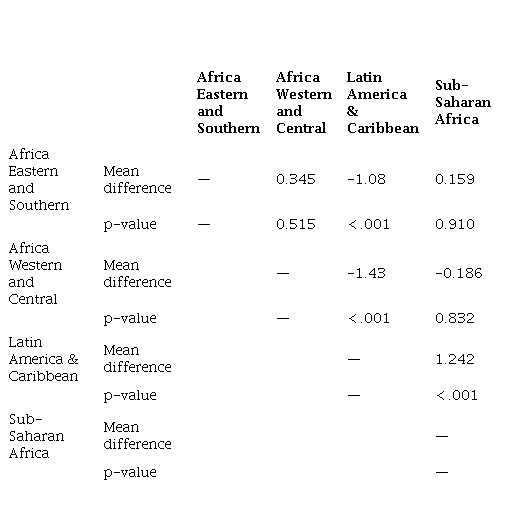

In Table 7, the Games-Howell post-hoc test reveals significant differences in Foreign Direct Investment, net inflows (% of GDP) across regions. Africa Eastern and Southern shows a significant mean difference from Latin America and Caribbean, with the latter reporting higher FDI inflows. Similarly, Africa Western and Central also differs significantly from Latin America and the Caribbean. However, there are no significant differences between Sub-Saharan Africa and the other regions.

Table 7.

Games-Howell Post-Hoc Test – Foreign direct investment, net inflows (% of GDP)

| Africa Eastern and Southern | | Mean difference | | — | | 0.345 | | -1.08 | | 0.159 | |

| | p-value | | — | | 0.515 | | < .001 | | 0.910 | |

| Africa Western and Central | | Mean difference | | | | — | | -1.43 | | -0.186 | |

| | p-value | | | | — | | < .001 | | 0.832 | |

| Latin America & Caribbean | | Mean difference | | | | | | — | | 1.242 | |

| | p-value | | | | | | — | | < .001 | |

| Sub-Saharan Africa | | Mean difference | | | | | | | | — | |

| | p-value | | | | | | | | — | |

|

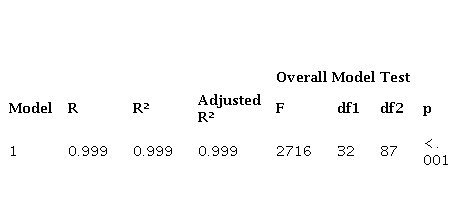

Regression Analysis

The results of Table 8 indicate an exceptionally good fit of the model. The R-value of 0.999, the R² of 0.999, and the adjusted R² of 0.999 indicate that the model explains almost all of the variance in the data. The F-value of 2716, with degrees of freedom df1 = 32 and df2 = 87, along with a p-value less than 0.001, further confirms that the model is statistically significant. These results indicate that the predictors included in the model (such as FDI, total debt service, and GDP growth) collectively account for a substantial portion of the variation in the Resilience Index. Given the near perfect fit, the model appears to provide a highly accurate and robust representation of the relationships among the variables.

Table 8.

Model Fit Measures

| 1 | | 0.999 | | 0.999 | | 0.999 | | 2716 | | 32 | | 87 | | < .001 | |

|

| | | | | | | | | | | | | | | |

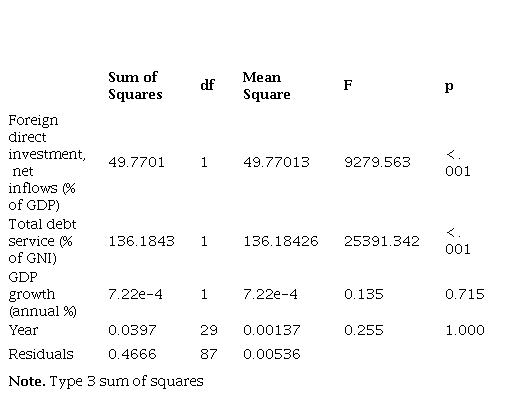

In Table 9, the results for FDI, net inflows (% of GDP) and total debt service (% of GNI) all have extremely large F-values and p-values less than 0.001, indicating that these two variables have a significant impact on the Resilience Index. In particular, FDI inflows and debt service levels appear to have a significant impact on resilience in all regions studied.

In contrast, GDP growth (annual %) has a very small F-value (0.135) and a p-value of 0.715, which is well above the 0.05 threshold for statistical significance. This suggests that GDP growth does not have a significant effect on the Resilience Index in this model. The Year variable also has a very low F-value (0.255) and a p-value of 1.000, indicating that year-to-year changes have no significant effect on resilience.

These results reinforce the notion that while FDI and debt service are important drivers of resilience, GDP growth and the specific year do not contribute significantly to changes in resilience levels.

Table 9.

Omnibus ANOVA Test

| Foreign direct investment, net inflows (% of GDP) | | 49.7701 | | 1 | | 49.77013 | | 9279.563 | | < .001 | |

| Total debt service (% of GNI) | | 136.1843 | | 1 | | 136.18426 | | 25391.342 | | < .001 | |

| GDP growth (annual %) | | 7.22e-4 | | 1 | | 7.22e-4 | | 0.135 | | 0.715 | |

| Year | | 0.0397 | | 29 | | 0.00137 | | 0.255 | | 1.000 | |

| Residuals | | 0.4666 | | 87 | | 0.00536 | | | | | |

| Note. Type 3 sum of squares |

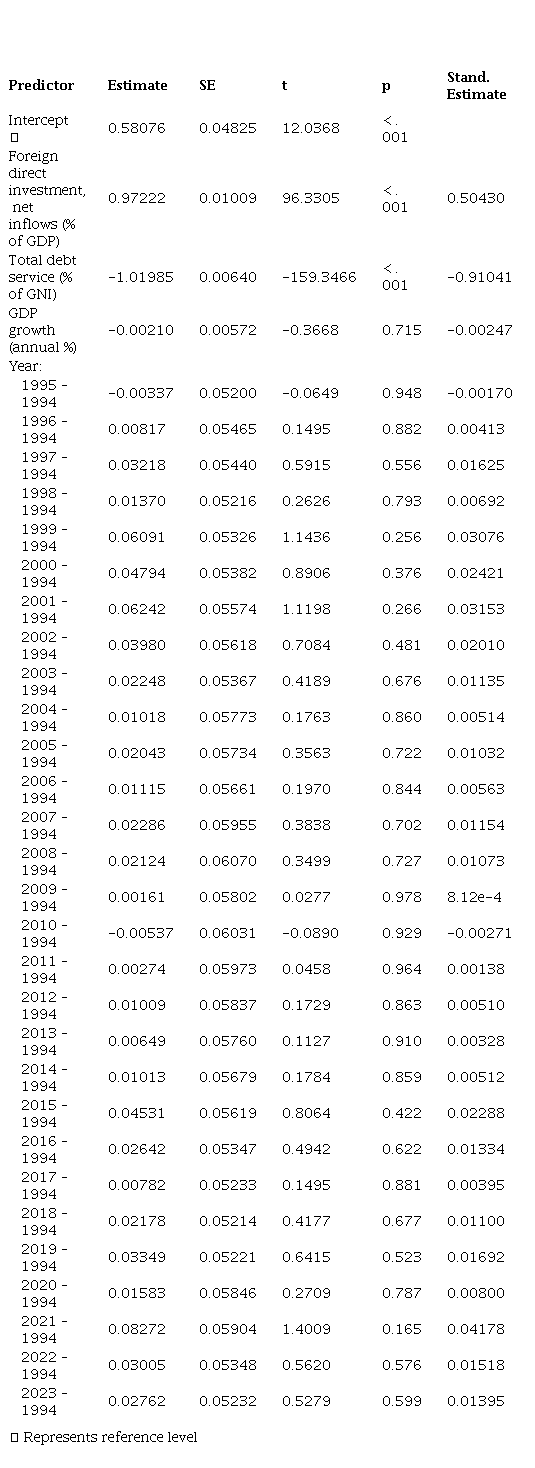

Table 10 shows the coefficients for the variables in the model. The intercept has a highly significant p-value (< 0.001) and an estimate of 0.58076, indicating a positive initial value for the Resilience Index when all predictors are zero.

For FDI, net inflows (% of GDP), the coefficient estimate is 0.97222 with a p-value less than 0.001. This indicates that for every unit increase in FDI as a percentage of GDP, the Resilience Index increases by about 0.97. The standardized estimate of 0.50430 suggests a moderate to strong positive relationship between FDI and resilience, meaning that countries with higher FDI inflows tend to have better resilience.

For total debt service (% of GNI), the coefficient estimate is -1.01985, with a p-value of less than 0.001. This indicates that higher levels of debt service are associated with lower resilience, with each unit increase in debt service leading to a decrease in resilience of about 1.02 units. The standardized estimate of -0.91041 reflects a strong negative relationship between debt service and resilience, implying that countries with higher debt burdens relative to their GNI tend to have weaker resilience.

On the other hand, GDP growth (annual %) shows a coefficient estimate of -0.00210, with a p-value of 0.715. This result suggests that GDP growth does not have a significant impact on the Resilience Index, as the coefficient is very small and statistically insignificant. The standardized estimate of -0.00247 further confirms the negligible effect of GDP growth on resilience in this model.

Regarding the Year variable, which measures annual changes from the reference year (1994), most of the year-to-year differences have very small coefficients and are not statistically significant. For example, the coefficient for 1995 - 1994 is -0.00337, with a p-value of 0.948, indicating no significant change in resilience between 1994 and 1995. Similarly, the differences for other years (e.g., 1996, 1997, 2001, 2003, etc.) are also small and insignificant, suggesting that changes over the years do not significantly affect resilience.

Table 10.

Model Coefficients - Resilience Index

| Intercept ᵃ | | 0.58076 | | 0.04825 | | 12.0368 | | < .001 | | | |

| Foreign direct investment, net inflows (% of GDP) | | 0.97222 | | 0.01009 | | 96.3305 | | < .001 | | 0.50430 | |

| Total debt service (% of GNI) | | -1.01985 | | 0.00640 | | -159.3466 | | < .001 | | -0.91041 | |

| GDP growth (annual %) | | -0.00210 | | 0.00572 | | -0.3668 | | 0.715 | | -0.00247 | |

| Year: | | | | | | | | | | | |

| 1995 – 1994 | | -0.00337 | | 0.05200 | | -0.0649 | | 0.948 | | -0.00170 | |

| 1996 – 1994 | | 0.00817 | | 0.05465 | | 0.1495 | | 0.882 | | 0.00413 | |

| 1997 – 1994 | | 0.03218 | | 0.05440 | | 0.5915 | | 0.556 | | 0.01625 | |

| 1998 – 1994 | | 0.01370 | | 0.05216 | | 0.2626 | | 0.793 | | 0.00692 | |

| 1999 – 1994 | | 0.06091 | | 0.05326 | | 1.1436 | | 0.256 | | 0.03076 | |

| 2000 – 1994 | | 0.04794 | | 0.05382 | | 0.8906 | | 0.376 | | 0.02421 | |

| 2001 – 1994 | | 0.06242 | | 0.05574 | | 1.1198 | | 0.266 | | 0.03153 | |

| 2002 – 1994 | | 0.03980 | | 0.05618 | | 0.7084 | | 0.481 | | 0.02010 | |

| 2003 – 1994 | | 0.02248 | | 0.05367 | | 0.4189 | | 0.676 | | 0.01135 | |

| 2004 – 1994 | | 0.01018 | | 0.05773 | | 0.1763 | | 0.860 | | 0.00514 | |

| 2005 – 1994 | | 0.02043 | | 0.05734 | | 0.3563 | | 0.722 | | 0.01032 | |

| 2006 – 1994 | | 0.01115 | | 0.05661 | | 0.1970 | | 0.844 | | 0.00563 | |

| 2007 – 1994 | | 0.02286 | | 0.05955 | | 0.3838 | | 0.702 | | 0.01154 | |

| 2008 – 1994 | | 0.02124 | | 0.06070 | | 0.3499 | | 0.727 | | 0.01073 | |

| 2009 – 1994 | | 0.00161 | | 0.05802 | | 0.0277 | | 0.978 | | 8.12e-4 | |

| 2010 – 1994 | | -0.00537 | | 0.06031 | | -0.0890 | | 0.929 | | -0.00271 | |

| 2011 – 1994 | | 0.00274 | | 0.05973 | | 0.0458 | | 0.964 | | 0.00138 | |

| 2012 – 1994 | | 0.01009 | | 0.05837 | | 0.1729 | | 0.863 | | 0.00510 | |

| 2013 – 1994 | | 0.00649 | | 0.05760 | | 0.1127 | | 0.910 | | 0.00328 | |

| 2014 – 1994 | | 0.01013 | | 0.05679 | | 0.1784 | | 0.859 | | 0.00512 | |

| 2015 – 1994 | | 0.04531 | | 0.05619 | | 0.8064 | | 0.422 | | 0.02288 | |

| 2016 – 1994 | | 0.02642 | | 0.05347 | | 0.4942 | | 0.622 | | 0.01334 | |

| 2017 – 1994 | | 0.00782 | | 0.05233 | | 0.1495 | | 0.881 | | 0.00395 | |

| 2018 – 1994 | | 0.02178 | | 0.05214 | | 0.4177 | | 0.677 | | 0.01100 | |

| 2019 – 1994 | | 0.03349 | | 0.05221 | | 0.6415 | | 0.523 | | 0.01692 | |

| 2020 – 1994 | | 0.01583 | | 0.05846 | | 0.2709 | | 0.787 | | 0.00800 | |

| 2021 – 1994 | | 0.08272 | | 0.05904 | | 1.4009 | | 0.165 | | 0.04178 | |

| 2022 – 1994 | | 0.03005 | | 0.05348 | | 0.5620 | | 0.576 | | 0.01518 | |

| 2023 – 1994 | | 0.02762 | | 0.05232 | | 0.5279 | | 0.599 | | 0.01395 | |

| ᵃ Represents reference level |

|

The results of this model suggest that FDI and total debt service are the most influential predictors of resilience. The strong positive relationship between FDI and resilience underscores the importance of foreign investment in enhancing a country's ability to cope with economic challenges. Conversely, the strong negative relationship between debt service and resilience underscores the negative impact of high debt burdens on a country's economic stability and resilience.

However, GDP growth does not appear to have a significant effect on resilience, suggesting that factors such as investment flows and debt management may be more critical in building resilience than simply achieving higher GDP growth rates. In addition, year-to-year variation does not appear to have a significant effect on resilience, suggesting that resilience is influenced more by structural factors such as investment and debt levels than by short-term changes in economic growth.

Overall, the model highlights the importance of fiscal and economic policy choices, in particular foreign investment and debt management, in fostering resilience. The lack of significant influence of GDP growth and the passage of time suggests that resilience depends more on long-term economic strategies than on short-term fluctuations in growth.

5. Discussion

The results of this study provide a deeper understanding of the relationship between economic resilience, debt service, foreign direct investment (FDI), and GDP growth, with a focus on four developing regions: Latin America and the Caribbean, Western and Central Africa, Eastern and Southern Africa, and Sub-Saharan Africa. By analyzing these regions, the study builds on previous literature that emphasizes the importance of debt management, economic diversification, and investment attractiveness in fostering resilience (Briguglio, 2016; Dahmani & Makram, 2024). However, this study differs in some respects from existing findings and provides new insights into how these factors interact across regions.

Debt Burden and Economic Resilience

A strong negative correlation between total debt service (% of GNI) and the resilience index (r = -0.863, p < 0.001) suggests that economies with high debt burdens tend to have lower economic resilience. This finding is consistent with the existing literature, which suggests that excessive debt service can strain fiscal resources, limit public investment, and hinder economic stability. In addition, there is a significant negative correlation between total debt service and GDP growth (r = -0.430, p < 0.001). This is in line with the findings of Dahmani and Makram (2024), who argue that financial stability is crucial for sustained economic growth in sub-Saharan Africa.

However, this study adds a new dimension by highlighting regional disparities in debt service levels, particularly in Latin America and the Caribbean, where debt burdens are significantly higher. This finding suggests that differences in borrowing strategies and access to international financial markets play a critical role in shaping debt dynamics across regions, further supporting the need for region-specific policy approaches as emphasized in the literature (Rasheed & Tahir, 2024).

GDP Growth, Resilience, and Stability

This study found a positive and significant correlation between GDP growth and the resilience index (r = 0.395, p < 0.001), which is consistent with the general understanding in the literature that robust economic growth is a key indicator of resilience (Briguglio & Piccin-ino, 2012). However, GDP growth did not significantly affect the stability of GDP growth (r = 0.124, p = 0.176), suggesting that growth rates alone do not necessarily lead to stable economies. This finding contrasts with the literature, which often assumes that sustained growth leads to stability (Onafowora & Owoye, 2019). The lack of significance in the relationship between GDP growth and resilience (F = 0.135, p = 0.715) suggests that resilience is more influenced by a broader set of economic factors, such as fiscal policy and debt management, rather than growth alone. This supports the argument made in the introduction that resilience is a multifaceted concept that requires more than just high growth rates.

Foreign Direct Investment and Economic Stability

Foreign direct investment (FDI) emerged as a key factor positively correlated with economic resilience (r = 0.430, p < 0.001), which is consistent with findings in the literature that emphasize the role of FDI in promoting economic adaptability and stability (Husain, 2024). FDI brings in much needed capital, technology, and employment opportunities, all of which contribute to increased resilience, as discussed in the literature review. However, this study also found a significant negative correlation between FDI and GDP growth stability (r = -0.349, p < 0.001), suggesting that economies with higher FDI inflows experience greater fluctuations in growth. This finding reflects the cyclical nature of FDI, where inflows can fluctuate based on global economic conditions and investor confidence, and supports the view from the literature review that the impact of FDI on stability is nuanced and depends on governance and institutional quality (Talla, 2023; Yangailo, 2024).

Regional differences in FDI inflows were also significant, with Latin America and the Caribbean receiving the highest FDI (3.143% of GDP on average). These findings confirm that regional investment climates and business environments play a key role in attracting foreign capital and support the literature's suggestion that the effectiveness of FDI depends on the institutional framework and quality of governance (Husain, 2024). The strong positive correlation between FDI and resilience in this study underscores the critical need for policies that create a favorable investment environment to support economic stability.

Regional Economic Disparities

The descriptive statistics revealed significant regional differences in resilience, debt service, GDP growth and FDI. Latin America and the Caribbean had the lowest resilience and the highest debt burden, while Western and Central Africa had the highest GDP growth rates. These findings highlight the diverse economic challenges faced by each region and underscore the need for tailored policy approaches to foster resilience, as suggested in the literature review (Henri, 2019; Rasheed & Tahir, 2024).

The study also highlighted challenges related to data distribution, as both GDP growth and FDI inflows did not follow normal distributions (p < 0.05), which could affect the reliability of parametric tests. The violation of the homogeneity of variances assumption further suggests that future studies should explore nonparametric methods or robust regression models to account for these complexities, which was a gap identified in the literature (Spratt & Bernini, 2010).

Policy Implications and Recommendations

The results of this study reveal significant regional disparities in economic resilience, debt service burdens, GDP growth, and FDI inflows, which call for tailored policy approaches for each region. The policy implications and recommendations for Latin America and the Caribbean, Western and Central Africa, Eastern and Southern Africa, and Sub-Saharan Africa are presented in the following paragraphs.

Latin America and the Caribbean

Latin America and the Caribbean has the highest debt service burden (average = 5.451% of GNI) and the lowest resilience index (average = -1.949), despite attracting the highest FDI inflows (average = 3.143% of GDP). This suggests that while the region is successful in attracting foreign investment, it is struggling to translate these inflows into long-term economic stability. The high debt burden is likely to strain fiscal resources, limit public investment, and hinder resilience. To address these challenges, the region should prioritize debt management through restructuring programs and concessional financing to reduce debt service obligations. Strengthening fiscal discipline by improving tax systems and reducing non-essential spending is also critical. In addition, the region should focus on attracting quality FDI in sectors such as technology, renewable energy, and manufacturing, while strengthening institutional frameworks to ensure that these investments contribute to resilience. Economic diversification is another key priority, as reducing reliance on volatile sectors such as commodities can enhance stability. Finally, investments in social safety nets and sustainable development initiatives will help protect vulnerable populations and address environmental challenges, further enhancing long-term resilience.

Africa Western and Central

Africa Western and Central has the highest GDP growth (mean = 4.269%), but only moderate levels of resilience (mean = -0.934) and FDI inflows (mean = 1.715% of GDP). This suggests that while the region is experiencing robust economic expansion, growth is not yet translating into broader stability. To sustain high growth, the region should invest in infrastructure development and promote agricultural modernization to increase productivity and food security. Debt sustainability should also be a focus, with efforts to monitor debt levels and prioritize domestic resource mobilization to reduce reliance on external borrowing. Attracting and effectively using foreign direct investment is another key area for improvement. Streamlining regulations, reducing red tape, and targeting FDI to strategic sectors such as renewable energy and digital technologies can help. Building resilience requires strengthening financial systems and investing in education and health to develop human capital and reduce vulnerability to external shocks.

Africa Eastern and Southern

Africa Eastern and Southern has moderate levels of debt service (mean = 3.585% of GNI), GDP growth (average = 3.444%), and FDI inflows (mean = 2.059% of GDP), with a resilience index of -1,000. While the region shows potential, structural bottlenecks hinder its ability to translate these factors into higher resilience. To address this, the region should focus on debt sustainability by prioritizing concessional lending and strengthening public financial management. Boosting FDI inflows through the development of special economic zones (SEZs) and enhanced trade facilitation measures can also help. Economic diversification is critical, with investments in value-added industries such as agro-processing and manufacturing, as well as digital transformation to unlock new growth opportunities. Enhancing resilience requires strengthening social protection systems and investing in climate-resilient infrastructure to address environmental challenges and improve long-term stability.

Sub-Saharan Africa

Sub-Saharan Africa has the lowest debt service burden (mean = 3.214% of GNI) and the highest resilience index (mean = -0.778), indicating relatively better economic stability. However, the region attracts the lowest FDI inflows (average = 1.901% of GDP), suggesting untapped potential for leveraging foreign investment to further enhance resilience. To attract more FDI, the region should improve investment promotion agencies and address infrastructure gaps to reduce the cost of doing business. Maintaining prudent fiscal policies and strengthening governance and anti-corruption measures will help maintain resilience. Economic diversification through industrialization and support for entrepreneurship and innovation is also essential to reduce dependence on commodities and create stable sources of growth. In addition, strengthening regional integration through trade agreements and cross-border infrastructure investments can expand market access and attract cross-border investment.

Cross-Regional Recommendations

In all regions, strengthening institutions is a common priority. Improving governance, transparency and institutional quality will enhance the effectiveness of economic policies and attract investment. Data-driven policymaking is also critical, as investments in data collection and analysis will enable governments to better understand the drivers of resilience and design targeted interventions. Regional cooperation through knowledge sharing and collaboration can help address common challenges and leverage best practices. Finally, all regions should prioritize climate resilience by adopting adaptation and mitigation strategies to address environmental risks and build long-term stability.

6. Conclusiones

This study highlights the complex relationships between debt service, economic growth, FDI, and resilience in four developing regions: Latin America and the Caribbean, Western and Central Africa, Eastern and Southern Africa, and Sub-Saharan Africa. High debt service burdens are consistently associated with lower resilience, slower growth, and greater economic volatility, while FDI inflows contribute positively to resilience but can lead to instability in growth patterns. Regional differences in debt burdens, GDP growth, and investment attractiveness underscore the need for differentiated policy strategies.

For Latin America and the Caribbean,, where high debt service burdens are the most pressing issue, policymakers should prioritize debt management strategies such as debt restructuring and fiscal discipline. In addition, promoting investment in non-commodity sectors such as technology and renewable energy can help build resilience. Economic diversification and strengthening institutional frameworks are key priorities to improve long-term stability.

In Western and Central Africa, despite robust GDP growth, the challenge remains to translate growth into broader economic stability. Infrastructure investment, economic diversification, and targeted FDI policies in strategic sectors are essential to ensure that growth translates into sustainable resilience. In addition, prioritizing debt sustainability and improving fiscal policies will lay the foundation for lasting stability.

For Eastern and Southern Africa, structural challenges such as moderate debt service levels and GDP growth are hampering resilience. This region needs enhanced debt sustainability measures and targeted FDI attraction in areas such as manufacturing and digital transformation. Economic diversification is critical, and the region needs to strengthen social protection systems and build climate-resilient infrastructure to enhance stability.

Sub-Saharan Africa stands out for its relatively low debt burden and resilience. However, the region faces untapped potential for foreign direct investment, and improving investment promotion is key. Sustaining resilience also requires investment in human capital, infrastructure, and governance. Economic diversification, regional integration, and industrialization will reduce dependence on volatile sectors and ensure long-term stability.

Overall, these findings highlight the need for region-specific policy interventions. Strengthening governance and institutional frameworks, focusing on attracting FDI, and improving debt management are critical components in promoting economic resilience. Future research should examine the role of institutional quality, trade policies, and external economic shocks in shaping resilience to provide a more comprehensive understanding of economic stability across these diverse regions.

Study Limitations:

While the study provides valuable insights, there are several limitations. First, the reliance on a resilience index based on GDP growth, stability, FDI, and debt service does not capture other factors that may influence resilience, such as political stability, institutional quality, or environmental risks. Second, the study uses aggregated regional data, which may overlook intra-regional disparities. In addition, the violation of normality assumptions for GDP growth and FDI inflows suggests the need for caution in interpreting the results, as nonparametric methods or robust regression techniques may be more appropriate for future studies.

Finally, while the study covers a wide range of regions, it does not address microeconomic factors or sector-specific resilience, which could provide further insights into the dynamics at play within individual countries or industries.

Future Recommendations

Future research should examine the role of governance and institutional quality in enhancing economic resilience, as these factors could significantly influence the effectiveness of debt management and the use of FDI. In addition, studies should consider microeconomic and sectoral factors, examining how specific industries contribute to resilience and stability within regions. Given the limitations of using aggregate data, more granular studies at the country or sector level are encouraged. Finally, non-parametric methods should be explored to address data distribution issues and ensure robustness of results.