1. Introducción

The financial services sector has seen a substantial transformation as a result of Industry 4.0, which is defined by the incorporation of cutting-edge digital technology across many industries. Under the broad heading of industry 4.0, developments like as automation, data analytics, artificial intelligence (AI), and the Internet of Things (IoT) offer opportunities for enhanced customer experiences and higher operational efficiency (Schwab, 2017). Using these technological advancements has become essential for businesses looking to stay current and competitive in this ever-evolving environment. In the framework of Industry4.0, the value of satisfied customers cannot be emphasized at a time when companies across all industries are vying for a competitive advantage. Numerous studies have shown that happy customers are far more inclined to show brand loyalty, refer people to the business, and become more involved with the services provided. Additionally, technological advancements can address gaps in financial inclusion by providing formerly underprivileged individuals with improved accessibility and opportunities for financial empowerment (Kirmizi & Kocaoglu, 2021).

The financial sector's integration of Industry 4.0 technology signifies a fundamental shift in client expectations, in addition to a technological transformation. In their dealings with financial institutions, customers of today want seamless, effective, and customized experiences. Realizing that Industry 4.0 may live up to these standards, Moniepoint Financial Technology took the initiative to implement cutting-edge digital advancements. Moniepoint has redesigned its customer interaction techniques to adapt to the changing needs of its customers by providing AI-powered chatbots, mobile applications for smooth transactions, and predictive modeling. Customer happiness is greatly affected by the use of Industry 4.0 technology. Studies have demonstrated that customers' views of the level of service and happiness in the financial industry are greatly impacted by the ease afforded by technology. By utilizing these technologies, Moniepoint hopes to improve client satisfaction through simpler procedures, faster response times, and customized solutions. But despite this change, worries about privacy violations, data security, and the possibility of impersonal interactions surface (European Central Bank, 2020).

The path taken by Moniepoint Financial Technology offers a singular chance to analyze how Industry 4.0 affects consumer satisfaction in the financial domain. The goal of this study is to examine the complex relationships between consumer perceptions and experiences and the adoption of new technologies. It seeks to offer practical information for financial institutions traversing the potential and problems brought forth by Industry 4.0 by concentrating on Moniepoint's instance. Furthermore, the study's conclusions could have applications outside of the financial technology industry. Knowing how technology and consumer satisfaction interact is essential as more financial institutions and businesses investigate integrating cutting-edge technologies. As a result, this study adds to the larger conversation on customer-centricity in the digital era and provides a paradigm for striking a balance between innovation and customer expectations (Ahuchogu et al., 2024).

In the age of technology, factors that contribute to customer satisfaction comprise data security, practicality, accessibility, and personalization (Hassan et al., 2022). Thus, a detailed investigation into the relationship between Industry 4.0 advancements from Moniepoint Financial Technology and customer satisfaction is required. Customer happiness is a critical determinant of the viability and performance of financial institutions in the quickly changing financial landscape of today. With the advent of Industry 4.0, which is defined by the combination of digital technologies, consumer satisfaction dynamics have experienced a significant shift. As a forward-thinking company, Moniepoint Financial Technologies understands how important client happiness is to its long-term survival and success.

The Industry 4.0 structure has created a new financial environment that has undergone significant changes due to the integration of current digital technologies (Lee, et. al., 2014). Innovative financial company Moniepoint Financial Technology Limited has embraced technological developments to improve its offerings and operational processes. While using automation, data analytics, artificial intelligence (AI), and digital banking systems promises many advantages, there are also important concerns and challenges that need to be addressed. Even while digital banking platforms are being used more and more, there is a clear lack of understanding about how these platforms really affect consumers' convenience in a setting of Moniepoint Financial Technology Limited. In the pursuit of facilitating seamless financial transactions, it is critical to determine if the incorporation of digital platforms has actually resulted in increased client convenience. This raises the question regarding if these platforms are doing a good job of bridging the gap between traditional banking procedures and modern client expectations. This study uses moniepoint financial technology to examine how industry 4.0 is affecting consumer happiness.

1.1 Research Objectives

The main objective of the study is to examine the impact of industry 4.0 on customer satisfaction in Moniepoint Financial Technology Limited. Other specific objectives are to;

-

examine the impact of Digital Banking Platforms on Customers Convenience in Moniepoint Financial Technology Limited

-

determine the influence of artificial intelligence on customer personalization in Moniepoint Financial Technology.

-

assess the effect of automation on customer efficiency in Moniepoint Financial Technology.

Research Hypotheses

Ho1: There is no significant impact of digital banking platforms on customers’ convenience in Moniepoint Financial Technology.

Ho2: Artificial intelligence has no significant influence on customer personalization in Moniepoint Financial Technology Limited.

Ho3: There is no significant effect of automation on Customer efficiency in Moniepoint Financial Technology

2. Marco Teórico

Concept of Industry 4.0

Driven by the confluence of cutting-edge digital technologies, the Fourth Industrial Revolution signifies a profound upheaval in the way organizations, industries, and society operate (Asif, 2020). It is crucial to examine its historical background, guiding principles, and the technical forces driving this revolutionary age while drawing on academic ideas in order to fully appreciate its influence and significance (Beier et al., 2020).

From a historical perspective, the idea of industrial revolutions dates back to significant periods in human history. While the Second Industrial Revolution brought electricity and mass manufacturing, the First Industrial Revolution used steam power and automation (Cancino et al., 2018). The digital era was made possible by the computerization that marked the Third Industrial Revolution. The Fourth Industrial Revolution, which is now taking place in the twenty-first century, builds on these previous stages but sets itself apart in a major way by emphasizing digital technology, connectivity, and the smooth transition between the digital and physical domains (Schwab, 2016).

Digitalization is the fundamental tenet that supports the Fourth Industrial Revolution. To make it easier to store, analyze, and share information, processes, and products, this entails converting them into digital representations. For many other aspects of Industry 4.0, digitalization serves as the cornerstone (Schwab, 2016). Another essential idea is interconnectivity, which is pivotal to the Internet of Things (IoT). Internet of Things (IoT) devices, which include sensors and networked equipment, allow data to be exchanged in real time between objects, systems, and people, resulting in a dynamic network of interactions and information (Atzori, Iera, & Morabito, 2010).

Measures of Industry 4.0

Digital Banking Platforms: Often referred to as online banking platforms or digital banking solutions, digital banking platforms mark a significant change in the accessibility and delivery of financial services. They include an array of digital tools and technologies that make it possible for people, companies, and financial institutions to manage their money, carry out banking operations, and get financial services via digital channels, usually the internet or mobile applications. Virtual cards, bank chatbots, and mobile banking apps are the three main components that characterize digital banking platforms.

Artificial Intelligence: Within computer science, artificial intelligence (AI) is the study and development of intelligent machines that can carry out activities that normally call for human intellect. Problem-solving, experience-based learning, reasoning, comprehending natural language, and pattern recognition are some of these activities. Artificial intelligence (AI) systems are engineered to emulate or simulate several facets of human intellect, enabling them to make judgments, resolve issues, and adjust to evolving circumstances (Tripathi & Rosak-Szyrocka, 2024).

Automation: Automation is the process of employing machinery, software, or technology to carry out activities with the least amount of human involvement. The principal aim of this approach is to improve and streamline processes in many sectors, resulting in heightened production, decreased mistakes, and higher efficiency.

Concept of Customer Satisfaction

The dynamics of customer satisfaction have undergone a significant upheaval with the advent of the digital era, making it essential for businesses to stay competitive and build enduring connections with their clients. Customer happiness is not only a catchphrase in this day and age; it is essential to success.The emergence of individualized experiences is one of the most noticeable shifts. The emergence of digital technologies, including artificial intelligence (AI) and data analytics, has enabled organizations to collect and evaluate enormous volumes of customer data. This makes it possible to provide extremely individualized experiences, such as content suggestions and purchase recommendations (Bhuiyan, 2024). Bhuiyan (2024) have noted that customisation increases customer satisfaction by giving them a sense of worth and understanding. Customers today expect businesses to anticipate their needs and preferences, therefore businesses that succeed in this sector are more inclined to win over customers' loyalty.

Furthermore, accessibility and ease in consumer interactions have been redefined in the digital age. Customers may now interact with enterprises at their convenience due to the elimination of geographical restrictions brought about by e-commerce platforms, smartphone applications, and online services. Being accessible around-the-clock is essential to ensuring that customers are satisfied. According to Kumar et al. (2018), in the digital era, clients anticipate prompt service and effective replies. Instantaneous replies are now expected, and firms who satisfy these expectations see higher levels of customer satisfaction. Chatbots and automated systems have become the standard.

Dimensions of Customer Satisfaction

Customer Personalization

Thanks to improved data analytics and digital technology, client customization has experienced a dramatic revolution in the digital era. Thanks to the abundance of consumer data available to them, businesses can now better understand the unique interests and habits of their customers. Customized customer journeys, real-time chatbot conversations powered by AI, and highly focused marketing efforts are all fueled by this insight (Bhuiyan, 2024). A crucial component of success in the digital age, this increased level of customisation not only boosts consumer happiness but also cultivates client loyalty.

Customer Efficiency

Customer efficiency has significantly increased in the digital age because to self-service alternatives, faster information access, quick transactions, and automated customer assistance. Digital technology expansion has also made data-driven customization, mobile accessibility, and effective feedback systems possible. Because they provide comfort, speed, and simplicity in customer interactions, these efficiency gains are intrinsically tied to consumer pleasure (Bhuiyan, 2024).

Customer Convenience

Online shopping, mobile applications, digital payments, on-demand services, tailored suggestions, automation, freelance employment, and digital content usage have all significantly increased customer convenience in the digital age. The way customers engage with organizations has been transformed by these innovations, which have also simplified procedures and reduced the time and effort needed for various operations (Bhuiyan, 2024).

Impact of Industry 4.0 on Customer Satisfaction

A new age of consumer pleasure has been brought about by Industry 4.0, which is defined by the incorporation of digital technology and the Internet of Things (IoT) into industrial and manufacturing operations. This shift stems from Industry 4.0's capacity to provide customized goods and services. Businesses may precisely respond to specific client preferences through flexible and agile production processes that are fueled by automation and data analytics (Barnatt, 2017). Consumers now want specific remedies, and Industry 4.0 helps companies to deliver on these demands. This leads to happier consumers as they get goods and services that perfectly suit their particular requirements and preferences.

Furthermore, quicker delivery times brought about by Industry 4.0 have a major influence on consumer happiness. According to Kägermann et al. (2013), Industry 4.0 technologies and smart factories enable supply chains to be optimized, resulting in shorter lead times and faster product delivery. Industry 4.0 has changed the game by providing consumers with quick and effective service in industries like e-commerce and retail, where quick delivery is a crucial competitive advantage. Moreover, Industry 4.0 enhances product quality, which is a key factor in consumer happiness. Early defect and quality issue identification is made possible in smart manufacturing facilities by real-time monitoring and data analytics (Wuest et al., 2016).

Theoretical Review

Customer Experience Management (CEM) Theory

The strategy framework known as Customer Experience Management (CEM) centers on the comprehensive administration of customer interactions with a corporation. Within the framework of Industry 4.0, CEM is essential to raising customer satisfaction since it coordinates smooth, customized interactions with many digital touchpoints. Holistic Customer Journey Mapping: CEM starts with a thorough mapping of the customer journey that includes every digital touchpoint. Understanding the complete customer experience is crucial in Industry 4.0, as customers interact through websites, mobile applications, social media, chatbots, and IoT devices (Meyer & Schwager, 2007).

Additionally, CEM uses data analytics to learn more about the requirements, preferences, and behavior of its customers. Businesses may segment their consumer base and offer highly tailored goods, suggestions, and content by utilizing AI and machine learning. According to Bhuiyan (2024), personalization has the power to increase customer happiness by boosting relevance and engagement.

Empirical Framework

Rymarczyk (2021). investigated the effects of the fourth industrial revolution on global commerce. The article's goal is to investigate how the Fourth Industrial Revolution (4IR), which is made up of ground-breaking inventions, has affected the amount and composition of global commerce. The essay draws on both internet and print sources. It is based on desk research, reports from various research organizations, literature reviews, and information from the Internet. Conclusions: The volume and composition of international commerce will significantly alter as a result of the 4IR's fundamental innovations being applied. Services will see a significant upswing in demand, while products will mainly focus on those whose expenses in transportation, logistics, information, regulation, and transaction have historically been expensive. These products will become increasingly important as a result of digitization. Trade circumstances will be significantly altered by the use of 4IR's gadgets. According to the adage "the winner takes it all," the first movers will profit the most. Because of their advantages in terms of finance and technology, developed countries will have the best opportunities to compete. Small and medium-sized businesses from developing nations will be able to expand their part in global trade, nevertheless, as trading costs will drop and the trade's material infrastructure needs would decrease. In addition to outlining the quantitative, structural, and comparative implications of Industry 4.0 devices on nations and businesses, the paper provides a thorough assessment of the prospective influence of these devices on global commerce. It lists the obstacles to the anticipated improvements and the requirements that these changes impose.

Zywiolek, et., al., (2021) investigated Polish industrial businesses' satisfaction levels with the use of Industry 4.0. Through a thorough assessment of the literature, it examined the issue of satisfaction with the use of industry 4.0. The Kano model was constructed based on the results of the investigation, which was carried out using the CAWI diagnostic opinion questionnaire. 670 people from businesses in different parts of Poland participated in the poll. Entrepreneurs express their worries and rewards in no uncertain terms. Industry 4.0 is not well understood and is only being applied in some contexts due to low social awareness of its existence. Thanks to the Kano model, the satisfaction survey was able to identify the conditioning and required qualities as well as those that the organization cannot do without, hence lowering implementation costs. The study also shown that new solutions may be implemented more quickly and effectively when they are based on a knowledge of the issue from the viewpoint of the employee rather than merely the company's customer. According to the study's conclusion, Industry 4.0 solutions have a major impact on how much businesses expand economically and, in turn, how the nation develops.

Martasari (2023) goal was to assess how Industry 4.0 technologies may enhance consumer satisfaction and service quality on e-commerce platforms. The influence of industrial technology 4.0 on e-commerce for data collecting is the main topic of this article. Creating this material began with a search for credible and pertinent publications. After that, the abstract and title are used to order the search results. If appropriate, a review of the literature must be done before a comparison may be made. It was discovered that e-commerce platforms' customer experience and service quality are significantly enhanced by industrial technology 4.0. Furthermore, the customization of services on e-commerce platforms has been enhanced by the application of industrial technology 4.0. E-commerce businesses may now use a range of tools and solutions to increase their operational efficiency and customer service due to the rapid improvements in technology. E-commerce businesses have enhanced consumer happiness and revenue by implementing these technologies, enabling them to provide a smooth and customized purchasing experience for their clients.

3. Research Methodology

The research will employ a descriptive design and employ the survey methodology. This is due to the fact that the goal of descriptive research is to accurately depict a person, event, or circumstance. Since it contributes to the explanation of present practices related to the topic issue, descriptive research design is deemed suitable. As a research subject, Moniepoint Financial Technology Limited's customer satisfaction is examined in relation to industry 4.0. The 397 students from University of Ilorin in Ilorin, Kwara state, Nigeria, will make up the research population. The survey's respondents were chosen from the whole population of the study region using the purposeful sampling approach. The sample size was calculated using Taro Yamane's (1967) 397 sample size estimate. A questionnaire utilized to gather replies from the respondents served as the primary source of data. There were five Likert scale items in the questionnaire.

The study instrument was tested using both descriptive and inferential statistics, including multiple linear regression analysis. With the use of SmartPLS version 3, structural equation modeling was used to examine the connections among the data produced in the research area.

Model Specification

Hypothesis I

Ho1, Ho2, and Ho3 was analyzed using the model below:

Y = β0+β1X1+β2X2+β3X3+....βnXn

Ho1: There is no significant impact of digital banking platforms on customers’ convenience in Moniepoint Financial Technology.

CC =  Where:

Where:

CC = Customer Convenience

MBA = Mobile Banking Apps

VC = Virtual Cards

BC = Bank Chatbot

Hypothesis II

Ho2: Artificial intelligence has no significant influence on customer personalization in Moniepoint Financial Technology.

CP =  Where:

Where:

CP = Customer Personalization

CS = Customer Support

FDP = Fraud Detection and Prevention

DS = Data Security

Hypothesis III

Ho3: There is no significant effect of automation on customers’ efficiency in Moniepoint Financial Technology.

WE =  Where:

Where:

CE = Customer Efficiency

PT = Processing Time

ER = Error Rate

CI = Customer Interaction

4. Result

Measurement Model

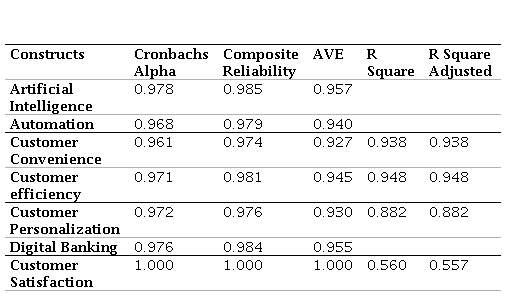

Table 1

Construct Reliability and Convergent Validity

Smart PLS 3 Output (2024)

Smart PLS 3 Output (2024)

| Constructs | Cronbachs Alpha | Composite Reliability | AVE | R Square | R Square Adjusted |

| Artificial Intelligence | 0.978 | 0.985 | 0.957 | | |

| Automation | 0.968 | 0.979 | 0.940 | | |

| Customer Convenience | 0.961 | 0.974 | 0.927 | 0.938 | 0.938 |

| Customer efficiency | 0.971 | 0.981 | 0.945 | 0.948 | 0.948 |

| Customer Personalization | 0.972 | 0.976 | 0.930 | 0.882 | 0.882 |

| Digital Banking | 0.976 | 0.984 | 0.955 | | |

| Customer Satisfaction | 1.000 | 1.000 | 1.000 | 0.560 | 0.557 |

The data gathered from 350 respondents was analyzed by the researcher using Bootstrapping and the Partial Least Square (PLS) Algorithm. Table 1 presented the total variance, T statistics, and R Square values for each of the 25 examined variables, comprising 7 latent variables and 18 indicators. Each and every element was verified, proving its applicability to the research.

In terms of the indicators' dependability, the PLS algorithm findings demonstrate that Cronbach's alpha values varied from 0.961 to 0.978, above the 0.70 standard value and demonstrating the indicators' consistency in measuring the hidden variables. The constructions' dependability was reinforced by the composite reliability values, which varied between 0.974 to 0.985. Furthermore, the indicators' validity was demonstrated by the average variance extracted (AVE) values, which ranged from 0.927 to 0.957 and confirmed both their divergent and convergent validity. Every value was higher than the minimally necessary 0.50 threshold.

The R-squared (R²) and modified R² values demonstrated the significant predictive power; variables pertaining to customer satisfaction, such as job efficiency, customization, and convenience, were predicted by 93.8%, 94.8%, and 88.2%, respectively. These results demonstrated that digital banking, automation, and artificial intelligence are significant predictors of these factors at Moniepoint Fintech in Ilorin, Kwara State, Nigeria; the rest of the variances, 6.2%, 5.2%, and 11.8%, were attributed to factors that were not considered. This demonstrates the significant influence of Industry 4.0 factors on consumer satisfaction.

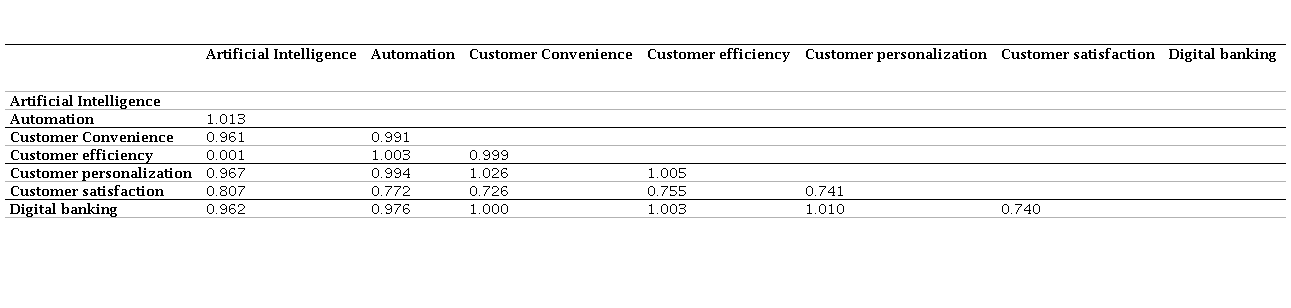

Table 2

Discriminant Validity

Authors Compilation (Smart PLS 3 Output (2024)

Authors Compilation (Smart PLS 3 Output (2024)

| Artificial Intelligence | Automation | Customer Convenience | Customer efficiency | Customer personalization | Customer satisfaction | Digital banking |

| Artificial Intelligence | | | | | | | |

| Automation | 1.013 | | | | | | |

| Customer Convenience | 0.961 | 0.991 | | | | | |

| Customer efficiency | 0.001 | 1.003 | 0.999 | | | | |

| Customer personalization | 0.967 | 0.994 | 1.026 | 1.005 | | | |

| Customer satisfaction | 0.807 | 0.772 | 0.726 | 0.755 | 0.741 | | |

| Digital banking | 0.962 | 0.976 | 1.000 | 1.003 | 1.010 | 0.740 | |

Strong evidence of discriminant validity among the latent variables—Artificial Intelligence, Automation, Customer Convenience, Customer Efficiency, Customer Personalization, Customer Satisfaction, and Digital Banking—is presented in Table 2's findings of the discriminant validity study. Every concept is guaranteed to be different from every other construct through discriminant validity. According to the research, there should be less correlation between various constructs when the diagonal values, which indicate the square root of the Average Variance Extracted (AVE) for each construct, are greater than the off-diagonal values.

The diagonal values, or square roots of the AVE, in discriminant validity represent the variance that each construct captures in relation to measurement error. The off-diagonal values, which show the correlations between the constructs, need to be less than these diagonal values, which go from top-left to bottom-right. The uniqueness of the constructs is reinforced by the off-diagonal correlations, which are less than the diagonal values.

For instance, "Artificial Intelligence" has an AVE square root of around 1.013, which shows that it is distinct from the other constructs. The constructs—Artificial Intelligence, Automation, Customer Convenience, Customer Efficiency, Customer Personalization, Customer Satisfaction, and Digital Banking—are distinct and do not significantly overlap in what they measure, according to this pattern, where diagonal values are larger than off-diagonal correlations.

As a result, the table exhibits good discriminant validity, indicating that the research's components are distinct and well-defined, with little measurement overlap.

Multicollinearity

This assesses the correlation between the independent variable. It is to know if two independent variables are not correlated and producing the same result. The variance inflation factor (VIF) is used in this study to assess likely correlation between the independent variables.

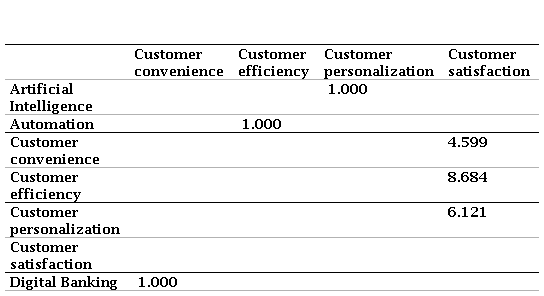

Table 3

Inner VIF Values

Smart PLS 3 Output (2024)

Smart PLS 3 Output (2024)

| Customer convenience | Customer efficiency | Customer personalization | Customer satisfaction |

| Artificial Intelligence | | | 1.000 | |

| Automation | | 1.000 | | |

| Customer convenience | | | | 4.599 |

| Customer efficiency | | | | 8.684 |

| Customer personalization | | | | 6.121 |

| Customer satisfaction | | | | |

| Digital Banking | 1.000 | | | |

The Variance Inflation Factor (VIF) table is used in regression studies to evaluate multicollinearity among predictor variables. As predictors have strong correlation, it becomes difficult to ascertain how each predictor affects the dependent variable separately. In this instance, the predictor variables being assessed for multicollinearity are customer convenience, customer efficiency, and customer customization.

If there is a reason to be concerned about multicollinearity, the VIF values are compared to the benchmark of 10. Since every VIF value is much less than 10, it may be concluded that there isn't much multicollinearity between the variables. The predictors' separate impacts on the dependent variable may be measured because of the weak correlation between them.

To sum up, the estimates provided by the model about the correlations between the predictor and dependent variables exhibit stability and consistency. The results are nonetheless dependable and unaffected by large correlations between the predictors because there is no discernible multicollinearity.

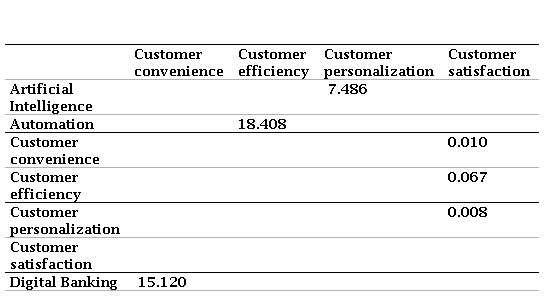

Table 4

Effect Size (f2) of Matrix

Smart PLS 3 Output (2024)

Smart PLS 3 Output (2024)

| Customer convenience | Customer efficiency | Customer personalization | Customer satisfaction |

| Artificial Intelligence | | | 7.486 | |

| Automation | | 18.408 | | |

| Customer convenience | | | | 0.010 |

| Customer efficiency | | | | 0.067 |

| Customer personalization | | | | 0.008 |

| Customer satisfaction | | | | |

| Digital Banking | 15.120 | | | |

The impact of every independent variable on the dependent variable was explicitly evaluated by calculating the significance of various constructs within the analytical framework using the f2 (effect size) matrix.

With a f2 value of 0.010, customer convenience has little bearing on related constructs like customer satisfaction, customer personalization, and customer efficiency. It has very little effect on the explanation of variability in these variables.

With a f2 of 0.067, customer efficiency has a marginally greater influence than customer convenience. It still only accounts for a significant portion of the variation in the other constructions, though.

Likewise, Customer Personalization has a negligible impact on other factors such as customer Convenience, customer Efficiency, and customer Satisfaction (f2 = 0.008). This indicates that their unpredictability can only be partially explained.

With a f2 value of 15.120, online banking has a far more significant function in the model. It highlights its critical role in the broader framework by explaining a major amount of the variation in linked variables.

Structural Model

Table 5

Path Analysis

Smart PLS 3 Output (2024)

Smart PLS 3 Output (2024)

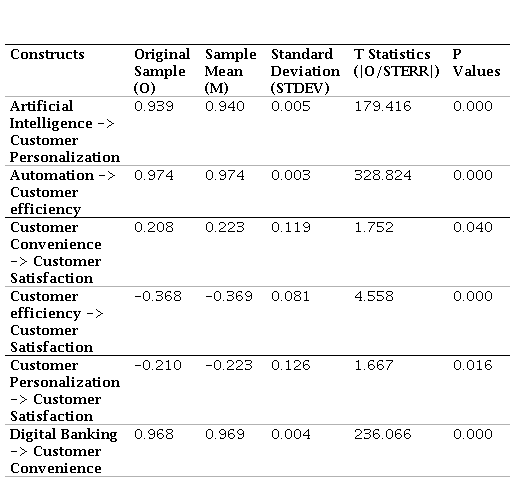

| Constructs | Original Sample (O) | Sample Mean (M) | Standard Deviation (STDEV) | T Statistics (|O/STERR|) | P Values |

| Artificial Intelligence -> Customer Personalization | 0.939 | 0.940 | 0.005 | 179.416 | 0.000 |

| Automation -> Customer efficiency | 0.974 | 0.974 | 0.003 | 328.824 | 0.000 |

| Customer Convenience -> Customer Satisfaction | 0.208 | 0.223 | 0.119 | 1.752 | 0.040 |

| Customer efficiency -> Customer Satisfaction | -0.368 | -0.369 | 0.081 | 4.558 | 0.000 |

| Customer Personalization -> Customer Satisfaction | -0.210 | -0.223 | 0.126 | 1.667 | 0.016 |

| Digital Banking -> Customer Convenience | 0.968 | 0.969 | 0.004 | 236.066 | 0.000 |

The outcomes of the path analysis show that digital banking, automation, and artificial intelligence have a major impact on important factors. Based on the data, it can be concluded that artificial intelligence had a considerable impact on consumer personalization (β = 0.939, t = 179.416, p = 0.000), hence validating the first hypothesis. Artificial intelligence (AI) has a significant influence in improving consumer personalization, as seen by the R2 value of 0.882, which shows that 88.2% of the variance in customer personalization is explained by AI.

In terms of automation and Customer efficiency, the study shows that automation had a substantial impact on Customer efficiency (β = 0.974, t = 328.824, p = 0.000), proving the second hypothesis. At Moniepoint Fintech Limited, automation greatly increases Customer efficiency as evidenced by its R2 of 0.948, which explains 94.8% of the variation in labor efficiency.

The findings indicate that there was a substantial impact of digital banking on consumer convenience (β = 0.968, t = 236.066, p = 0.000), indicating that Hypothesis three is supported. The substantial influence of digital banking on customer convenience is demonstrated by the R2 value of 0.938, which shows that it accounts for 93.8% of the variation in consumer convenience.

Additionally, the data demonstrates that consumer convenience has a substantial impact on customer satisfaction (β = 0.208, t = 1.752, p = 0.040). This suggests that at Moniepoint Fintech Ltd., customer happiness is significantly impacted by consumer ease.

Furthermore, a substantial negative influence is revealed by the path analysis of customer satisfaction and job efficiency (β = -0.368, t = 4.558, p = 0.000). This implies that Moniepoint Fintech Limited's customer happiness suffers when Customer efficiency increases.

Customer customization has a negative impact on customer satisfaction at Moniepoint Fintech Limited, as evidenced by the considerable (β = -0.210, t = 1.667, p = 0.016) effect on customer satisfaction.

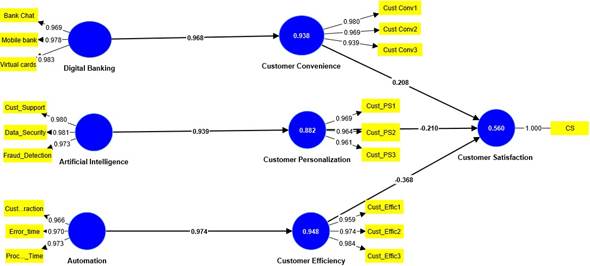

Figure 1

Structural Equation Path Model. Source: Smart PLS 3 Output, 2024

Smart PLS 3 Output, 2024

Figure 1

Structural Equation Path Model. Source: Smart PLS 3 Output, 2024

Smart PLS 3 Output, 2024

The path model illustrated in Figure 1 reveals strong and reliable relationships among indicators of digital banking. The correlation coefficients for the bank chatbot, mobile banking app, and virtual cards are 0.969, 0.978, and 0.983, respectively, demonstrating that these indicators are effective predictors of digital banking with robust and dependable relationships.

In the context of artificial intelligence, the indicators customer support, data security, and fraud detection exhibit correlation coefficients of 0.980, 0.981, and 0.973, respectively. These values underscore the strong and reliable nature of these indicators as predictors of artificial intelligence, highlighting their significant and dependable roles in enhancing AI applications.

For automation, the indicators customer interaction, error time, and processing time have correlation coefficients of 0.966, 0.970, and 0.973, respectively. These figures illustrate a strong and reliable relationship among the indicators as predictors of automation, emphasizing their effectiveness and consistency in streamlining processes.

Regarding the dependent variables, customer convenience is assessed through cust_conv1, cust_conv2, and cust_conv3, with correlation coefficients of 0.980, 0.969, and 0.939, respectively. These high values indicate a strong and reliable relationship of these indicators as predictors of customer convenience. Additionally, the indicators Cust_PS1, Cust_PS2, and Cust_PS3 for customer personalization show correlation coefficients of 0.969, 0.961, and 0.964, respectively, signifying their strong and dependable relationship as predictors of customer personalization. Regarding Customer efficiency, the indicators Cust_Effic1, Cust_Effic2, and Cust_Effic3 reflect correlation coefficients of 0.959, 0.974, and 0.984, respectively, indicating a strong and reliable relationship of these indicators as predictors of Customer efficiency

5. Discussion of Findings

Based on the analysis of operational data gathered via the field survey and the test of hypotheses, the following findings were revealed:

The study also revealed that elements of artificial intelligence—such as customer support, data security, and fraud detection—significantly impact customer personalization, contributing to satisfaction at Moniepoint Financial Technology Limited. The rejection of the null hypothesis in favor of the alternative hypothesis aligns with Buranasing, et. al. (2021), who noted that effective Industry 4.0 technologies boost business competitiveness, particularly during the COVID-19 pandemic. This highlights AI’s role in enhancing personalization.

Customer efficiency, another indicator of employee satisfaction at Moniepoint Financial Technology Limited, was shown to be highly impacted by customer engagement, error time, and processing time—all of which are connected to automation. The alternative hypothesis is supported by the rejection of the null hypothesis, which is consistent with Martasari's (2023) observation that Industry 4.0 technology improves e-commerce service quality and efficiency. This emphasizes how important automation is to increasing productivity at work.

6. Conclusion

In conclusion, the following are drawn from the findings of the study:

The research provided high support for the first hypothesis, which proposed that digital banking systems have a considerable impact on client convenience. The findings suggest that in order to improve client convenience, solutions like electronic cards, mobile banking applications, and bank chatbots are crucial. In order to meet client expectations in the current banking environment, Moniepoint Financial Technology Limited needs to make investments in and enhance these digital banking products.

Additionally, there was substantial confirmation of the second hypothesis, which questioned the impact of AI on client customisation. The investigation demonstrates that through functions like fraud detection, data protection, and customer assistance, artificial intelligence is essential to client customisation. This emphasizes how crucial it is for Moniepoint Financial Technology Limited to use AI technology in order to provide customized and individualized client experiences.

The data study provided strong support for the third hypothesis, which looked at how automation affects productivity at work. Automation has been identified as a critical component in increasing job efficiency, particularly in areas like client engagement, mistake diminution, and processing time improvement. This demonstrates how automation has greatly benefited Moniepoint Financial Technology Limited's operations.

7. Recommendations

Based on the conclusions drawn from the study, several recommendations can be made for Moniepoint Financial technology Limited to enhance customer satisfaction through the effective utilization of Industry 4.0 technologies:

Additional investments in cutting-edge digital banking systems, such as chatbots, mobile banking applications, and virtual cards, should be given top priority by Moniepoint management since they greatly improve client convenience. To maintain its leading position in digital banking innovation, the bank will make sure that these systems receive frequent upgrades and improvements.

The management of Moniepoint should keep using artificial intelligence (AI) technologies into its business practices. Personalized customer experiences require AI-driven fraud detection, data security, and customer support. Putting resources in AI technology will allow the bank to provide customized services while maintaining the security of client data.

Moniepoint management ought to look for ways to automate repetitive processes, particularly those involving customer service, minimizing errors, and processing time. Processes that are faster and more effective may be achieved through automation, which will eventually save operating costs and improve customer service.

The bank has to set up a mechanism for ongoing performance evaluation and appraisal of Industry 4.0 technologies' effects on client satisfaction. Frequent assessments of these developments will aid in pinpointing opportunities for enhancement and optimization, guaranteeing that the bank efficiently fulfills consumer expectations.