Municipal Tourist Tax Regulations in Portugal: A comparative analysis

Regulaciones del Impuesto Municipal Turístico en Portugal: un análisis comparativo

Turismo y Patrimonio, no. 25, pp. 7-21, 2025

Universidad de San Martín de Porres

Received: 31 January 2025

Accepted: 15 April 2025

Para citar este artículo:: Vareiro, L., Gonçalves, S., Miranda, E. V., & Mendes, R. (2025). Municipal Tourist Tax Regulations in Portugal: A comparative analysis. Turismo y Patrimonio, 25, 7-21. https://doi.org/10.24265/turpatrim.2025.n25.01

Abstract: Our research has explored the complex landscape of Municipal Tourist Tax regulations across Portuguese municipalities that currently impose a tourist tax on overnight stays. The introduction of a tourist tax in Portugal first occurred in Aveiro in 2013. However, its implementation and collection did not achieve the expected impact, so it was discontinued. Many Portuguese municipalities now impose the tourist tax, including popular destinations such as Porto, Lisbon, and Faro, offering a unique opportunity to assess the evolving regulatory landscape and its effects on local economies. This study examined and compared the Portuguese regulations in force at the end of 2023. The analysis focused on the date of application, incidence, value, purpose, and exemptions of the tourist tax applied in the various municipalities, providing insights into the effectiveness and challenges of these tax policies in Portugal. The research will not only contribute to the scholarly understanding of municipal tourist tax dynamics but also offer practical implications for policymakers, local authorities, and the broader tourism industry.

Keywords: Municipal tourist tax, Portuguese municipalities, sustainability, tourist tax regulations.

Resumen: Nuestra investigación ha explorado el intrincado panorama de las regulaciones del Impuesto Municipal Turístico en los municipios portugueses que actualmente imponen un impuesto turístico sobre las pernoctaciones. La primera experiencia de un impuesto turístico en Portugal ocurrió en Aveiro en 2013. Sin embargo, su aplicación y recaudación no tuvieron el impacto esperado, por lo que fue descontinuado. Actualmente, numerosos municipios portugueses cobran este impuesto turístico, incluyendo destinos destacados como Oporto, Lisboa y Faro, lo que brinda una oportunidad única para evaluar la evolución del panorama regulatorio y sus repercusiones en las economías locales. Este estudio examinó y comparó las regulaciones portuguesas vigentes hasta finales de 2023. El trabajo se centró en la fecha de aplicación, la incidencia, el valor, el propósito y las exenciones del impuesto turístico aplicado en los diferentes municipios, proporcionando perspectivas sobre la efectividad y los desafíos de estas políticas fiscales en Portugal. La investigación no solo contribuirá a la comprensión académica de las dinámicas del impuesto municipal turístico, sino que ofrecerá, también, implicaciones prácticas para los responsables de políticas, autoridades locales y la industria turística en general.

Palabras clave: Impuesto Municipal Turístico, municipios portugueses, sostenibilidad, regulaciones del impuesto turístico.

Introduction

Several cities, such as Lisbon and Porto, in Portugal, have become highly popular destinations. The influx of visitors has brought numerous benefits to the cities, including economic growth and cultural exchange. However, it has also placed a significant strain on local infrastructure and resources, leading to challenges such as overcrowding, environmental degradation, and rising living costs for residents – a phenomenon known as overtourism (Harvey, 2013; Milano, 2017). In response, several cities, including those we studied in this research have implemented tourist taxes to mitigate the impact of tourism and generate additional revenue for sustainable development. Despite their increasing adoption, a gap remains in comprehensive studies analysing these tax regulations and their effectiveness in various contexts in Portugal.

This research aimed to explore the implementation of tourist taxes in fifteen Portuguese municipalities, while also considering their potential adoption in other cities across the country. Specifically, the study examined and compared the Portuguese regulations in force as of the end of 2023. The main research question guiding this study is: How have Portuguese municipalities adapted their tourist tax regulations in response to tourism growth, and what lessons can be drawn for other cities? This question will be addressed through a detailed discussion of findings in the later sections of the paper.

The study employed a qualitative analysis. The first phase of the study involved a review of existing literature on tourist taxes, examining their purpose, structure, and outcomes in various contexts. Subsequently, the study examined the cases of fifteen municipalities in Portugal, analysing the regulations concerning tourist taxes in these cities, specifically their tourist tax systems. This analysis encompassed an examination of tax rates, collection methods, revenue allocation, and the overall effectiveness of these policies in achieving their intended objectives. Additionally, the research compared the experiences of these cities, highlighting similarities and differences in their approaches to implementing tourist taxes.

The interest of this study is substantial for both national and foreign municipalities seeking to implement a tourist tax. By analysing the regulatory frameworks of fifteen Portuguese municipalities, this research offers a detailed understanding of key operational dimensions, including tax rates, scope of application, exemptions, and stated purposes. These insights allow municipalities to benchmark against real-world examples, identify best practices, and anticipate challenges. For national municipalities, this comparative analysis provides a blueprint for harmonising their tax regulations with those of peer regions, promoting consistency and enhancing the effectiveness of their tourism policies.

For foreign municipalities, the study serves as a valuable reference point for adapting the Portuguese approach to their specific contexts. The inclusion of diverse categories, such as exemptions and seasonal variations can inspire the development of tailored strategies to align tax policies with local tourism patterns and socio-economic goals. Furthermore, the study highlights the role of transparency and official documentation in fostering public acceptance and compliance, an aspect that other municipalities can adopt to enhance the legitimacy and success of their tourist tax initiatives.

The paper is structured as follows: After this introduction, Section 2 reviews the literature on the foundations of tourism taxes and evolution studies in Portugal. Section 3 provides a brief contextualisation of the emergence of this type of legislation in Portugal. Section 4 details the methodology, while Section 5 presents the results of the analysis of the fifteen municipalities. Section 6 discusses the findings, and Section 7 concludes with policy implications, limitations, and research directions.

Literature review

Foundations of tourism taxation

Tourism taxation has become increasingly popular worldwide (Do Valle et al., 2012; García et al., 2018; Mak, 2006; WTO, 1998), with various motivations and objectives driving its implementation. In recent years, the rise of overtourism, characterised by excessive visitor numbers that strain local resources and infrastructure, has emerged as a critical factor shaping tax policies, particularly in high-demand destinations such as Portugal (Gusman et al., 2023; Peeters et al., 2018; Vareiro et al., 2023).

The primary motivations behind the application of tourist taxes are relatively consensual among authors (Biagi et al., 2017; Borges et al., 2020; Do Valle et al., 2012; Gago et al., 2009; Ihalanayake, 2013; Ponjan & Thirawat, 2016): i) to increase and diversify government revenues, ii) to fund the provision of public goods, and iii) to internalise negative externalities.

Firstly, governments use these taxes to expand their revenue streams, especially in destinations where tourism plays a significant role in the local economy (Biagi et al., 2017; Gago et al., 2009; Gooroochurn et al., 2005). Tourism’s unique characteristics, such as its inelastic demand in many destinations, make it a valuable source of revenue (Gooroochurn et al., 2005; López-del-Pino et al., 2020). Additionally, governments view tourism taxation as a way to allocate a budget for providing public goods and services, especially when the demand for such services surges during peak tourist seasons, and tourism-related extra costs increase substantially (Biagi et al., 2017; Gago et al., 2009). Furthermore, taxation can serve as a tool to correct externalities associated with tourism, such as congestion and environmental degradation (Adedoyin et al., 2023; Biagi et al., 2017; Gago et al., 2009; López-del-Pino et al., 2020), representing, according to López-del-Pino et al. (2020), the main argument for the use of tourism taxes as a tool to internalise these costs. Indeed, Nepal & Nepal (2021) argue that the tourism tax not only solves external costs but also increases economic efficiency, if used to avoid congestion peaks and de-seasonalize tourist activities. Similarly, Ihalanayake (2013) argues that taxes should be employed to internalise external costs and encourage more responsible tourist behaviour.

However, there are also dissenting opinions about these tourist taxes, with the tourism industry opposed to this type of tax, citing the potential loss of competitiveness that could result from its implementation (Biagi et al., 2017; Borges et al., 2020; Lee, 2014; López-del-Pino et al., 2020).

Tourism taxes, in general terms, can be divided into two categories: specific and general indirect taxes (Gago et al., 2009; Ihalanayake & Divisekera, 2006; Ponjan & Thirawat, 2016). Hotel room taxes and airport exit taxes are examples of specific taxes, whereas the value-added tax (VAT) is a widely used broad general indirect tax.

Considering the comparative analysis we will conduct, our focus is on the tourist tax levied on overnight stays in any accommodation, commonly referred to as the room tax or accommodation tax. These taxes are one of the most prevalent forms of tourism taxation globally (Do Valle et al., 2012; Gago et al., 2009; Gooroochurn et al., 2005). According to Do Valle et al. (2012), Durán-Roman et al. (2020), and Gago et al. (2009), these taxes can take the form of ad valorem (a percentage of the price) or ad quantum (unit tax) per night. Their flexibility allows differentiation based on lodging type, location, and seasons (Vareiro et al., 2023). Accommodation taxes have proven effective in addressing the objectives of tourism taxation, as mentioned above (Borges et al., 2020; Do Valle et al., 2012).

Evolution of studies in Portugal

In Portugal, since the tourism tax was only recently reintroduced (2016), empirical research remains limited. The earliest known work is that of Do Valle et al. (2012), which seeks to evaluate tourists’ receptivity towards an accommodation tax earmarked for environmental protection in the Algarve. The Algarve is a quintessential sun and sea destination, and tourism taxes are defended as a means of moderating and mitigating environmental impacts. The accommodation tax had not yet been implemented, and the authors attempted to measure tourists’ responses to such a proposal. They concluded that the vast majority of the tourists surveyed are not willing to pay an accommodation tax to fund environmental protection. Several reasons were identified for that, ranging from the fact that a mass sun and beach destination may not be attractive to environmentally friendly tourists, who are more likely to pay this type of tax, to the fact that tourists may not trust that the revenue from the accommodation tax will be used for environmental protection.

Costa (2016) presented a master’s thesis at the Portuguese Catholic University to obtain a master’s degree in business economics on «The Impact of the Tourist Tax in Northern Portugal». The main objective was to quantify the trade-offs associated with the potential implementation of a tourism tax in hotels and accommodations of the Northern region of Portugal. It focuses on its impact on the number of overnight stays, the revenues of hotel establishments, and the tax revenue generated. At that time, the tourism tax had not yet been implemented in any municipality in Northern Portugal. The results suggest that consumers are price-sensitive, and the implementation of the tourist tax is likely to lead to a decrease in the monthly number of stays across all accommodation types. On the other hand, implementing the tourist tax would generate significant tax revenue for all the municipalities within the region.

Costa (2017) published the book «Municipal Tourism Taxation - The case of the Municipality of Lisbon,» following his master’s thesis, which was defended in 2015. After outlining the taxation system in Portugal and conducting a comparative analysis of tourist taxes, the author examines the taxes introduced by the Municipality of Lisbon in this context. Specifically, the author scrutinises the overnight tax, air arrival tax, and sea arrival tax, raising questions and issues related to their categorisation, legality, implementation, and constitutionality.

Alves (2019) submitted her dissertation «Tourism in Portugal - Implementation of the Municipal Tourist Tax» as a partial requirement for the master’s degree in accounting at ISCTE, Lisbon. The primary objective of this study was to analyse the implementation of the municipal tourist tax in the Municipality of Lisbon and assess its effectiveness by examining the projected outcomes resulting from the imposition of this levy. The findings obtained demonstrated a strong correlation between the municipality’s expenditure increases and the rise in the number of tourists. It was also evident that the application of the tax had no significant negative impact on tourist demand, and the revenue generated contributed significantly to financing a substantial portion of the tourism-related expenses.

Borges et al. (2020) published a study on Porto, in which they sought to evaluate tourists’ awareness of the municipal tourist tax, assess their knowledge of it, and estimate the consequences on the city’s level of competitiveness as a tourism destination. Slightly over 50% of tourists were already informed about the tourist tax, with awareness varying based on their sociodemographic characteristics. Additionally, nearly 70.7% of tourists find this tax «acceptable». The tourist tax is considered competitive, and it is emphasised that if the generated revenue is invested in enhancing tourism and improving the quality of services, it is unlikely to affect the demand from the previously identified tourist profiles, thereby ensuring the destination remains attractive.

Context

In Portugal, public finances are regulated by Law no. 73/2013 of September 3, which sets out the financial regime of local authorities and inter- municipal entities, as well as Law no. 53-E/2006, of December 29, which establishes the general regime of fees for local authorities.

Some Portuguese municipalities already charge or intend to charge the tourist tax in establishments where tourists stay overnight. In this context, it is worth noting that the municipality of Aveiro was the first to introduce the tourist tax in 2013. Nevertheless, this proved to be unsuccessful, and it was revoked after two years, as the amount collected was lower than expected. By the end of 2023, fifteen city councils were charging tourist fees in tourist accommodation establishments, namely Braga, Cascais, Coimbra, Faro, Figueira da Foz, Lisbon (the first to introduce the tourist tax in Portugal, in 2016), Mafra, Óbidos, Olhão, Portimão, Porto, Santa Cruz in Madeira, Sintra, Vila Nova de Gaia, and Vila Real de Santo António.

Each municipality establishes its regulations, and therefore, tourist fees can vary according to the municipality where they are implemented, even though there are also several standard rules.

Methodology

This study used a qualitative content analysis to examine the regulatory frameworks governing tourist taxes in fifteen Portuguese municipalities that implemented this tax in 2023. Content analysis was selected as the methodological approach due to its capacity to systematically interpret textual data and identify patterns and themes within regulatory documents (Elo et al., 2014).

The data collection process involved sourcing official regulations concerning tourist taxes directly from the official websites of the respective municipalities or the Diário da República (Official State Gazette). The selection criterion ensured that only regulations effective in 2023 were included. Each document was carefully reviewed to ensure completeness and accuracy, and only publicly accessible, officially published texts were analysed.

The analysis focuses on five key categories: date of application, incidence, amount applied, purposes, and exemptions. These categories were selected based on their relevance to understanding the implementation and operational specifics of tourist taxes. Each category was defined as follows:

1. Date of application: The date on which the tourist tax regulation came into force.

2. Incidence: The entities or individuals subject to the tax, such as tourists staying in hotels or other accommodation types.

3. Amount applied: The specific tax rate or fee charged, including variations by accommodation type or tourist season.

4. Purposes: The stated purposes for implementing the tax include funding local tourism promotion or infrastructure improvements.

5. Exemptions: Any exemptions or special conditions, such as age-related exemptions or exemptions for specific categories of travellers.

Data were analysed systematically to identify trends, similarities, and differences across the municipalities. Findings were coded manually, with each regulation reviewed against the five categories. This approach enabled a comparative analysis and facilitated the identification of commonalities and unique features among the municipalities’ tourist tax frameworks. The results provide a comprehensive overview of the implementation of tourist taxes in Portugal during the study period.

Results

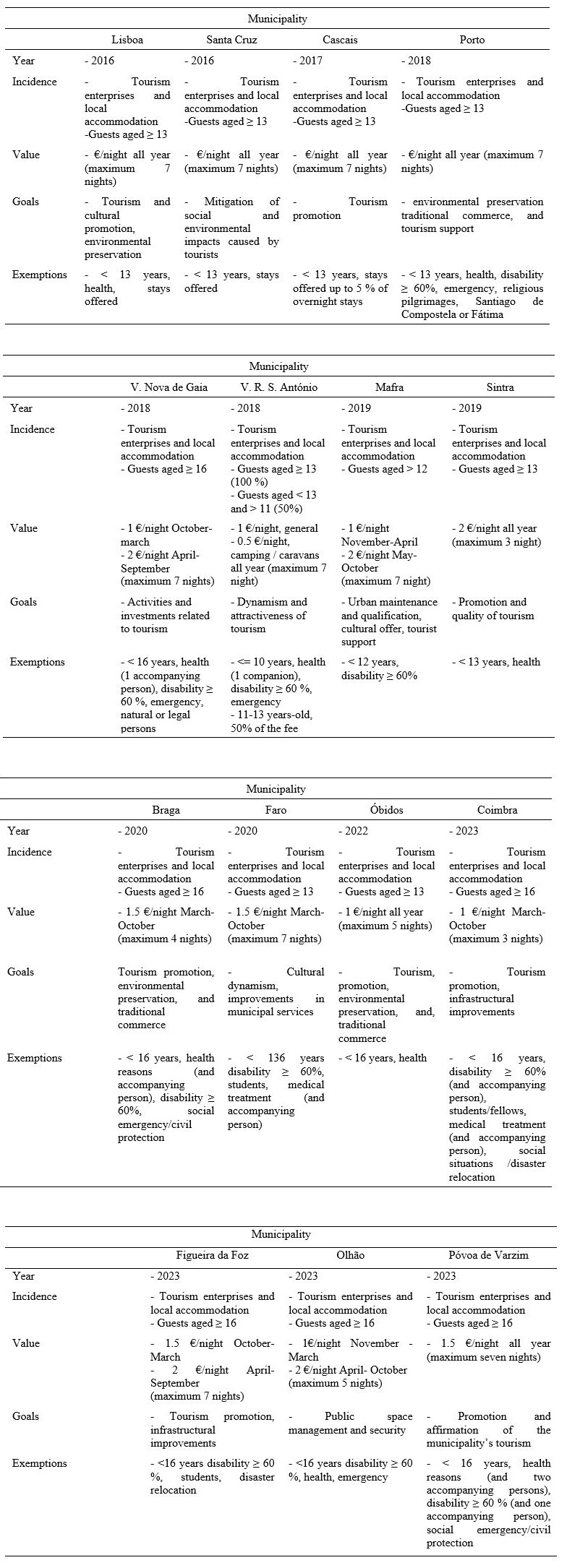

The implementation of the tourist tax in Portugal began to be gradually regulated by different municipalities, reflecting the evolution of their tourism strategies and local priorities. Table 1 presents tourist tax regulations by municipality 1.

Lisbon was a pioneer in implementing the tourist tax, starting the collection in 2016. The tax applies to guests aged 13 and above and has a fixed value of €2 per night, with a maximum stay of 7 nights. The generated revenue is allocated to tourism and cultural promotion, as well as environmental preservation and the maintenance of public facilities.

Santa Cruz also began applying the tourist tax in 2016, following a model similar to Lisbon, with a fee of €2 per night for guests aged 13 and over, with a maximum duration of 7 nights. The purpose of the revenue is similar, focusing on mitigating the social and environmental impact on infrastructure caused by tourists.

In 2017, Cascais introduced a tourist tax of €2 per night for guests aged 13 and above. The revenue is allocated to international promotion and tourism support, emphasising the promotion of the city as a high-quality tourist destination.

Porto followed this trend in 2018, introducing a €2 nightly tax for guests aged 13 and above. The revenue is used for environmental preservation, supporting traditional commerce, and providing tourist assistance, reflecting the significant role tourism plays in the local economy. Vila Nova de Gaia and Vila Real de Santo António also implemented the tourist tax in 2018. Gaia applies a rate of €2 per night from April to September and €1 per night for the rest of the year, for guests aged 16 and over, and Vila Real de Santo António has a differentiated rate for general tourists and caravanners. Both direct the revenues to similar purposes as Lisbon and Porto.

Mafra began charging the tourist tax in 2019, with a variable rate depending on the season: €1 per night from November to April and €2 per night from May to October. The tax applies to guests aged 12 and over and is applied for a maximum of 7 nights. The revenue is allocated to urban maintenance and cultural activities.

Sintra also started applying the tax in 2019, with a rate of €2 per night for guests aged 13 and over, using the revenue to support tourism and cultural promotion.

Braga and Faro introduced the tourist tax in 2020. Braga charges €1.50 per night for guests aged 16 and over from March to October, with a maximum of four nights. The revenue is used for tourism promotion, environmental preservation, and safeguarding traditional commerce. Faro, on the other hand, applies a rate of €1.50 per night from March to October, affecting guests aged 13 and above, with a maximum duration of 7 nights. The revenue is allocated to cultural dynamization and public space management to enhance services.

Óbidos began collecting the tourist tax in 2022, charging €1 per night for guests aged 13 and over, with a maximum stay of 5 nights. The revenue is used for tourism promotion, environmental preservation, and safeguarding traditional commerce.

In 2023, several municipalities implemented a tourist tax. Coimbra charges €1 per night for guests aged 16 and over, limited to a maximum of three nights, from March to October, with the revenue being used for the promotion and conservation of public assets. Figueira da Foz applies a seasonal tax:

€1.50 per night from October to March and €2 per night from April to September, for guests aged 16 and over, directing the revenue to economic promotion and space conservation. Olhão charges a seasonal rate of €1 per night from November to March and

€2 per night from April to October for guests aged 16 and over, with the revenue used for public management and security. Póvoa de Varzim introduced a rate of €1.50 per night for guests aged 16 and above, directing the revenue to the environmental preservation and tourism support.

Exemptions from the tourist tax are common among local authorities. They are usually granted to young visitors (aged under 12 to 16 years, depending on the location), individuals with disabilities with a degree of incapacity of 60% or more, students, and cases of social or civil protection emergencies. These exemptions reflect social sensitivity and an effort to balance tax revenue with the need for inclusion and support for vulnerable groups.

Discussion

The analysis of the tourist tax regulations in Portuguese municipalities reveals both similarities and notable differences among the 15 municipalities. These variations reflect each municipality’s specific strategies and priorities, adapting to their particular tourist characteristics and local needs

About similarities, we can highlight:

· General objective: Most municipalities impose the tourist tax to encourage tourism, preserve the environment, and improve local infrastructure. The revenue is primarily allocated to tourism and cultural promotion, and maintaining public spaces.

· Incidence: Many municipalities apply the tax on guests aged 13 or older. For example, Lisbon, Cascais, Porto, Santa Cruz, Sintra, and Vila Real de Santo António apply the tax to guests aged 13 or older, while Braga, Coimbra, Figueira da Foz, Olhão, Póvoa de Varzim, and Vila Nova de Gaia apply it to guests aged 16 or older.

· Exemptions: Exemptions are a common feature in municipal regulations. Usually, young guests (aged under 12 to 16 years old), individuals with disabilities with an incapacity of 60% or more, students, and cases of social civil protection emergencies are exempt. This practice shows social sensitivity and an effort to balance tax collection with the need for inclusion and support for vulnerable groups.

· Maximum duration: Most municipalities establish a maximum length for the tax application per stay, which generally ranges between 3 and 7 nights. For instance, Lisbon, Cascais, Porto, Santa Cruz, Sintra, and Vila Nova de Gaia apply the tax for stays up to 7 nights.

As far as differences are concerned:

· Date of implementation: The implementation timeline varies considerably. Lisbon and Santa Cruz were pioneers, introducing the tax in 2016, while Coimbra, Figueira da Foz, Olhão, and Póvoa de Varzim began applying it only in 2023.

· Tax value: Charges vary between municipalities. Lisbon, Cascais, Porto, Santa Cruz, and Sintra levy a fixed rate of €2 per night. Braga charges €1.50 per night, while Coimbra applies €1 per night. Some municipalities, such as Faro, Figueira da Foz, Mafra, and Olhão, have seasonal rates that range from €1 to €2 per night, depending on the time of year.

· Specific revenue purpose: Although tourism promotion and environmental preservation are common goals, the specific purposes can differ. Braga and Coimbra, for example, emphasise the preservation of traditional commerce. Faro and Figueira da Foz focus on cultural dynamization and public space management. Cascais and Mafra emphasise international promotion and tourism support.

· Seasonal incidence: Some municipalities, such as Figueira da Foz, Mafra, and Olhão, apply different rates depending on the season. Figueira da Foz charges a rate of €1.50 from October to March and €2 from April to September, while Mafra levies €1 per night from November to April and €2 per night from May to October. The municipalities that applied the tax only during part of the year, generally from March to October, in the changes planned for 2024, propose applying it year-round.

Furthermore, the research highlights both similarities with the established literature and differences that reflect specific local strategies and contexts.

Several findings align with the theoretical foundations of tourist taxation. As emphasised by Do Valle et al. (2012), Biagi et al. (2017), and Borges et al. (2020), tourist taxes are commonly implemented to generate additional revenue for local governments, finance public goods, and mitigate the negative externalities associated with increased tourism, such as congestion and environmental degradation. This is reflected in the Portuguese context, where most municipalities allocate their tourist tax revenue to purposes such as environmental preservation, tourism promotion, and urban maintenance.

The seasonal variation in tax rates, observed in municipalities such as Figueira da Foz, Mafra, and Olhão, reflects the strategic use of taxation as a tool to manage tourism demand and reduce pressure on local resources during peak periods, in line with the recommendations of Nepal & Nepal (2021) for managing overtourism through dynamic tax policies. These municipalities utilise taxation as a strategic instrument to balance tourist flow throughout the year, thereby avoiding congestion and its associated costs.

Another point to mention is the predominance of the ad quantum (fixed-per-night) tax structure in Portugal, which contrasts with the ad valorem system also used in other international contexts (Do Valle et al., 2012; Durán-Roman et al., 2020; Gago et al., 2009; Vareiro et al., 2023). This fixed-rate model introduces predictability for tourists and reduces administrative complexity for local authorities.

However, some findings diverge from established theoretical assumptions. While the literature often highlights concerns about reduced competitiveness due to the imposition of tourist taxes (Biagi et al., 2017; López-del-Pino et al., 2020), this research does not support those concerns. Cities like Lisbon and Porto have experienced sustained growth in tourism despite implementing the tax. These findings align with Alves (2019), who found that tourist demand remained stable in Lisbon, possibly due to visible reinvestment in infrastructure and services, funded by taxes, which enhanced the visitor experience.

The high degree of variation in tax exemptions and target age groups also distinguishes the Portuguese case from international norms. While exemptions for tourist taxes in many European countries typically target children and young people (Goktas & Polat, 2019; SIC Notícias, 2019), Portuguese municipalities implement diverse and localised exemption criteria based on their specific social and economic contexts. For example, the age thresholds for tax applicability range from 12 to 16 years, and exemptions often include students and individuals with certain health conditions, reflecting an effort to balance tax collection with social inclusion.

Conclusions

An analysis of the tourist tax regulations across the fifteen Portuguese municipalities reveals a diverse approach to the application and management of these taxes. Commonalities include the general objective of promoting tourism and environmental preservation, similar age thresholds for tax applicability, and the presence of exemptions to support social inclusivity. However, significant differences exist in the rates applied, specific revenue purposes, and the timing of tax implementation.

These findings underscore the adaptability of tourist tax policies to local contexts and the importance of developing tailored approaches to address the unique needs of each region. The study highlights the potential of tourist taxes to support sustainable tourism development, while also emphasising the need for transparent and efficient monitoring to ensure the effective utilisation of tax revenues. Future research could expand on the impacts of these taxes on tourist behaviour and local economies, providing a more comprehensive understanding of their long-term benefits and challenges.

The study examines regulations without providing a detailed analysis of the actual impact of these regulations on tourism, local economies, or social aspects. This limits the understanding of the broader consequences of the tax policies and will be the focus of our future research. Moreover, regulations enacted after 2023 were excluded; ongoing monitoring remains crucial and may lead to new studies.

Conflict of interest

The authors declare that they have no conflict of interest in this study.

Ethical responsibility

In the research, the authorship of the cited sources was acknowledged, and they were referenced at the end of the text. The necessary authorisations for conducting the research were obtained.

Author contribution

LMCV: Theoretical framework, analysis of results, discussion, conclusions, and references.

SMFG: Theoretical framework, analysis of results, discussion, conclusions, and references.

EMMM: Methodology, data collection, analysis of results, discussion, conclusions, and references.

RBVM: Methodology, data collection, analysis of results, discussion, conclusions, and references.

Funding

National funds supported this work through FCT/MCTES (PIDDAC): UID/04752, Applied

Management Research Unit (UNIAG).

Acknowledgements

Earlier versions of this paper were presented at the 63rd ERSA Congress, Ilha Terceira, Açores, Portugal, on August 26-30, 2024, and at ICOTTS 2024 - 6th International Conference on Tourism Technology & Systems, University of Madeira, Funchal, Portugal, on October 30-31, 2024. The authors would like to thank their colleagues present at both sessions for their contributions.

Regulations consulted

Regulation no. 382/2016 of Município de Cascais, Diário da República: II Série, no. 73 (2016). https://diariodarepublica.pt/dr/detalhe/regulamento/382-2016-74145437

Regulation no. 723/2018 of Município de Vila Real de Santo António, Diário da República: II Série, no. 207 (2018). https://diariodarepublica.pt/dr/detalhe/regulamento/723-2018-116791434

Regulation no. 773/2018 of Município de Óbidos, Diário da República: II Série, no. 219 (2018). https://diariodarepublica.pt/dr/detalhe/regulamento/773-2018-116963791

Notice no. 19334-A/2018 of Município de Lisboa, Diário da República: II Série, no. 248 (2018). https://diariodarepublica.pt/dr/detalhe/aviso/19334-a-2018-117487474

Public Notice no. 1022/2019 of Município de Braga, Diário da República: II Série, no. 175 (2019). https://diariodarepublica.pt/dr/detalhe/edital/1022-2019-124642728

Regulation no. 725/2019 of Município de Faro, Diário da República: II Série, no. 178 (2019). https://diariodarepublica.pt/dr/detalhe/regulamento/725-2019-124750449

Regulation no. 652/2022 of Município de Vila Nova de Gaia, Diário da República: II Série, no. 136 (2022). https://diariodarepublica.pt/dr/detalhe/regulamento/652-2022-186145829

Regulation no. 1111/2022 of Município de Santa Cruz, Diário da República: II Série, no. 219 (2022). https://diariodarepublica.pt/dr/detalhe/regulamento/1111-2022-203367383

Regulation no. 1135/2022 of Município do Porto, Diário da República: II Série, no. 226 (2022). https://diariodarepublica.pt/dr/detalhe/regulamento/1135-2022-203803584

Regulation no. 1182/2022 of Município de Póvoa de Varzim, Diário da República: II Série, no. 243 (2022). https://diariodarepublica.pt/dr/detalhe/regulamento/1182-2022-204991668

Regulation no. 207/2023 of Município de Mafra, Diário da República: II Série, no. 33 (2023). https://diariodarepublica.pt/dr/detalhe/regulamento/207-2023-207483822

Regulation no. 352/2023 do Município da Figueira da Foz, Diário da República: II Série, no. 56 (2023). https://diariodarepublica.pt/dr/detalhe/regulamento/352-2023-210488240

Notice no. 5970/2023 of Município de Coimbra, Diário da República: II Série, no. 57 (2023). https://diariodarepublica.pt/dr/detalhe/aviso/5970-2023-210520547

Notice no. 6116/2023 of Município de Sintra, Diário da República: II Série, no. 58 (2023). https://diariodarepublica.pt/dr/detalhe/aviso/6116-2023-210537223

Regulation no. 664/2024 of Município de Olhão, Diário da República: II Série, no. 115 (2024). https://diariodarepublica.pt/dr/detalhe/regulamento-extrato/664-2024-868658480

Datos de los autores

Laurentina Vareiro

Escuela de Gestión, Universidad Politécnica de Cávado e Ave, Barcelos, Portugal.

Doctora en Economía por la Universidad de Minho, Portugal. Actualmente, es profesora asociada y coordina el Grupo Disciplinario de Economía en la Facultad de Economía y Gestión en la Universidad Politécnica de Cávado y Ave, Portugal. También es investigadora en la Unidad de Investigación en Gestión Aplicada (UNIAG) y en el Centro de Investigación Lab2PT de la Universidad de Minho, Portugal.

ORCID: https://orcid.org/0000-0001-8945-1593

Autor corresponsal: lvareiro@ipca.pt

Soraia Gonçalves

Escuela de Gestión, Universidad Politécnica de Cávado e Ave, Barcelos, Portugal.

Doctora en Ciencias Políticas por la Universidad de Santiago de Compostela, España. Actualmente, es profesora asociada y coordina el Grupo Disciplinario de Administración Pública y Finanzas en la Facultad de Gestión de la Universidad Politécnica de Cávado y Ave, Portugal. También es investigadora de la Unidad de Investigación Aplicada en Gestión (UNIAG), Portugal.

ORCID: https://orcid.org/0000-0001-7385-438X

soraia@ipca.pt

Eva Maria Miranda

Escuela de Turismo y Hotelería, Universidad Politécnica de Cávado e Ave, Barcelos, Portugal.

Máster en Administración y Planificación Educativa por la Universidad Portucalense de Oporto, Portugal. Actualmente, es profesora en la Escuela de Administración y en la Escuela de Turismo y Hotelería en la Universidad Politécnica de Cávado y Ave, Portugal.

ORCID: https://orcid.org/0009-0002-5542-9800

emiranda@ipca.pt

Raquel Mendes

Escuela de Gestión, Universidad Politécnica de Cávado e Ave, Barcelos, Portugal.

Doctora en Economía por la Universidad de Minho, Portugal. Actualmente, es profesora asociada en la Facultad de Gestión de la Universidad Politécnica de Cávado y Ave, Portugal. Participación con comunicación oral en diversos eventos internacionales.

ORCID: https://orcid.org/0000-0002-7312-5248

rmendes@ipca.pt

References

Adedoyin, F., Seetaram, N., Disegna, M., & Filis, G. (2023). The effect of tourism taxation on international arrivals to a small tourism-dependent economy. Journal of Travel Research, 62(1), 135-153. https://doi.org/10.1177/00472875211053658

Alves, C. (2019). Turismo em Portugal: Aplicação da taxa municipal turística. Master’s Dissertation, ISCTE Business School.

Biagi, B., Brandano, M. G., & Pulina, M. (2017). Tourism taxation: A synthetic control method for policy evaluation. International Journal of Tourism Research, 19(5), 505-514. https://doi.org/10.1002/jtr.2123

Borges, A., Vieira, E., & Gomes, S. (2020). The evaluation of municipal tourist tax awareness: The case of the city of Porto. Tourism and Hospitality Management, 26(2), 381-398. https://doi.org/10.20867/thm.26.2.6

Costa, A. (2016). O impacto da taxa turística no Norte de Portugal. Master’s Dissertation, University Católica of Porto.

Costa, R. (2017). A tributação turística municipal: O caso do Município de Lisboa. Coimbra: Edições Almedina.

Do Valle, P., Pintassilgo, P., Matias, A., & André, F. (2012). Tourist attitudes towards an accommodation tax earmarked for environmental protection: A survey in the Algarve. Tourism Management, 33(6), 1408-1416. https://doi.org/10.1016/j.tourman.2012.01.003

Elo, S., Kääriäinen, M., Kanste, O., Pölkki, T., Utriainen, K., & Kyngäs, H. (2014). Qualitative content analysis. SAGE Open, 4(1). https://doi.org/10.1177/2158244014522633

Gago, A., Labandeira, X., Picos, F., & Rodríguez, M. (2009). Specific and general taxation of tourism activities. Evidence from Spain. Tourism Management, 30, 381-392. https://doi.org/10.1016/j.tourman.2008.08.004

García, A., Marchena, M., & Morilla, A. (2018). Sobre la oportunidad de las tasas turísticas: el caso de Sevilla. Cuadernos de Turismo, 42, 161-183. https://doi.org/10.6018/turismo.42.07

Gooroochurn, N., & Sinclair, M. T. (2005). Economics of tourism taxation: Evidence from Mauritius. Annals of Tourism Research, 32(2), 478-498. https://doi.org/10.1016/j.annals.2004.10.003

Goktas, L. S., & Polat, S. (2019). Tourist tax practices in European Union member countries and its applicability in Turkey. Journal of Tourismology, 5(2), 145-158. https://doi.org/10.26650/jot.2019.5.2.0026

Gusman, I., Rio Fernandes, J. A., & Chamusca, P. (2023). Back to business? Taking lessons from Porto (Portugal) to inform sustainable tourism futures after COVID-19. Boletín de la Asociación de Geógrafos Españoles (99). https://doi.org/10.21138/bage.3448

Harvey, D. (2013). Ciudades rebeldes: del derecho de la ciudad a la revolución urbana. Ediciones Akal, Madrid.

Ihalanayake, R. (2013). Tourism taxes and negative externalities in tourism in Australia: A CGE approach. Corporate Ownership & Control, 10(4), 200-214.

Ihalanayake, R., & Divisekera, S. (2006). The tourism tax burden: Evidence from Australia. Tourism Economics, 12(2), 247-262. https://doi.org/10.5367/000000006777637421

Law no. 73/2013, Assembleia da República, Diário da República: I Série, no. 169 (2013). https://diariodarepublica.pt/dr/legislacao-consolidada/lei/2013-105795409

Law no. 53-E/2006, Assembleia da República, Diário da República: I Série, no. 249 (2006). https://diariodarepublica.pt/dr/legislacao-consolidada/lei/2006-212243428

Lee, S. (2014). Revisiting the impact of bed tax with a spatial panel approach. International Journal of Hospitality Management, 41, 49-55. https://doi.org/10.1016/j.ijhm.2014.04.010

López-del-Pino, F., Grisolía, J., & Ortúzar, J. (2020). Is there room for a room tax in the Canary Islands? International Journal of Tourism Research, 23(5), 743-756. https://doi.org/10.1002/jtr.2438

Mak, J. (2006). Taxation of travel and tourism. In P. Forsyth & L. Dwyer (Eds). International handbook on the economics of tourism (pp. 251-265). Edward Elgar Publishing Limited.

Milano, C. (2017). Overtourism y turismofobia. Tendencias globales y contextos locales. Ostelea School of Tourism & Hospitality. http://www.aept.org/archivos/documentos/ostelea_informe_overtourism_y_turismofobia.pdf

Nepal, R., & Nepal, S. (2021). Managing overtourism through economic taxation: Policy lessons from five countries. Tourism Geographies, 23(5/6), 1094-1115. https://doi.org/10.1080/14616688.2019.1669070

Peeters, P., Gössling, S., Klijs, J., Milano, C., Novelli, M., Dijkmans, C., Eijgelaar, E., Hartman, S., Heslinga, J., Isaac, R., Mitas, O., Moretti, S., Nawijn, J., Papp, B., & Postma, A., (2018). Research for TRAN Committee - Overtourism: impact and possible policy responses. European Parliament, Policy Department for Structural and Cohesion Policies, Brussels. https:// www.europarl.europa.eu/RegData/etudes/STUD/2018/629184/IPOL_STU%282018%29629184_EN.pdf

Ponjan, P., & Thirawat, N. (2016). Impacts of Thailand’s tourism tax cut: A CGE analysis. Annals of Tourism Research, 61, 45-62. https://doi.org/10.1016/j.annals.2016.07.015

SIC Notícias. (2019). Vai viajar na Europa? Saiba o valor das taxas turísticas. https://sicnoticias.pt/economia/2019-01-04-Vai-viajar-na-Europa-Saiba-o-valor-das-taxas-turisticas

Vareiro, L., Miranda, E., & Gonçalves, S. (2023). Exploring motivations behind accommodation tax in Portuguese municipalities: A press reading. In A. Teixeira, A. P. Delgado, L. Carvalho, M. I. Mota & M. M. Castro e Silva (Eds.), Estudos de Homenagem a José da Silva Costa (pp. 710-721). Porto Press.

WTO. (1998). Tourism taxation: Striking a fair deal. World Tourism Organisation.

Notes

Additional information

Para citar este artículo:: Vareiro, L., Gonçalves, S., Miranda, E. V., & Mendes, R. (2025). Municipal Tourist Tax Regulations in Portugal: A comparative analysis. Turismo y Patrimonio, 25, 7-21. https://doi.org/10.24265/turpatrim.2025.n25.01