1 INTRODUCTION

The curriculum of talent development programs plays a pivotal role in undergraduate education, as it establishes the foundation for students to acquire the essential professional skills and knowledge required in their field. Its primary objective is to broaden students' expertise, guiding them toward more open and diverse directions of development. A well-structured talent development curriculum is crucial in determining the quality of accounting education, as it directly impacts the level of professional competence students achieve. In turn, this ensures the sustainability of education and helps prepare students for future academic pursuits or employment. As such, it has become a significant challenge and focus for university educators (Liu, 2024; Jackson, Richardson, Michelson, & Munir, 2022). Comparative analysis of talent development programs for accounting majors, both domestically and internationally, is relatively rare, reflecting the limited attention this area receives within the accounting discipline (Das & Singh, 2018; Fang, 2022).

Universities, as institutions responsible for talent cultivation, play a pivotal role in both social development and the nurturing of skilled professionals. The quality of curriculum design significantly impacts on the effectiveness of higher education in fulfilling these functions. The competencies of graduates are closely linked to the structure and relevance of the curriculum, highlighting its critical importance. Nevertheless, many universities are frequently criticized by both the public and industry for producing graduates whose skills do not meet the demands of the labor market. A persistent disconnect exists between academic training and the professional qualifications required by employers (Wang & Jing, 2018; Zhao, Huang, & Chen, 2017). This misalignment can largely be attributed to outdated educational structures and talent development models, as well as a lack of targeted curriculum planning. These issues have hindered the development of undergraduate accounting education (Achalapathi & Janakiram, 2016; Gao, 2016).

The objectives of this study are as follows: (1) To understand the current status and developmental direction of the undergraduate accounting talent cultivation programs at six universities; (2) To examine the differences in planning among these six universities with regard to talent cultivation goals, course modules, and curriculum design in the field of accounting; (3) To explore the distinctions, strengths, and potential shortcomings in the curriculum systems of these universities, and to propose feasible recommendations. This study aims to address a gap in the existing literature, which has seldom compared curriculum systems within accounting talent cultivation programs. It also seeks to highlight the unique characteristics and differences in accounting education planning across universities and to offer practical suggestions for the development of accounting curricula. The findings are expected to serve as a valuable reference for domestic universities in planning and designing future accounting programs, and to contribute to the advancement of the accounting discipline.

This study, therefore, employs content analysis and comparative research methods to examine the undergraduate accounting programs at universities in Guangdong Province, China. The criteria for selection and filtering are as follows: First, the universities must be located within the Guangdong-Hong Kong-Macao Greater Bay Area (GBA), which includes the nine cities of Guangzhou, Shenzhen, Zhuhai, Foshan, Huizhou, Dongguan, Zhongshan, Jiangmen, and Zhaoqing. Second, the universities’ official websites must provide detailed information on their accounting undergraduate talent development curriculum systems, with downloadable resources available. After searching and filtering, six sample institutions were selected, consisting of two universities and four colleges, all of which are undergraduate institutions.

The rankings of these six universities in the 2024-2025 Chinese undergraduate university rankings are as follows: 96th, 298th, 494th, 523rd, 702nd, and 950th (China Science and Education Evaluation Network, 2024). China has a total of 3,012 higher education institutions, including 2,756 general higher education institutions (1,270 universities and 1,486 colleges) and 256 adult higher education institutions. Of these, Guangdong Province is home to 160 general higher education institutions (67 universities and 93 colleges) and 14 adult higher education institutions (Ministry of Education of the People's Republic of China, 2024).

2 LITERATURE REVIEW

2.1 Current Status of the Accounting Industry

The development of accounting talent is significantly shaped by changes in the socioeconomic environment. Traditionally, accounting was focused on tasks such as bookkeeping, accounting, and financial reporting. However, the scope of accounting has expanded to include high-level management areas like internal control, investment and financing decisions, mergers and acquisitions, value management, and the informatization of accounting. Furthermore, the continuously evolving global landscape and shifting key competencies have transformed the nature of accounting work, shifting it from a primarily operational task to one based on knowledge and management skills.

In today's digital age, informatization allows accounting professionals to work more efficiently, with emerging technologies such as big data, cloud computing, and artificial intelligence having a profound impact on the future careers and employment opportunities for students in the field. The rapid development of these technologies, along with other global changes, creates new challenges that demand the acquisition of new key competencies, while simultaneously making traditional accounting roles increasingly obsolete (Deloitte, 2017).

In this context, society has raised higher expectations for university-level accounting education. The job market for general financial accountants is now saturated, while there remains a significant demand for high-quality accounting professionals with strong management skills. As a result, the accounting talent market is characterized by a polarized supply-and-demand gap (Huang, 2021; Liu, H. P., 2020). In the face of the knowledge economy, economic globalization, and the demand for highly skilled accounting professionals, universities must adapt by addressing the emerging knowledge and key competencies needed in the job market. This highlights the many challenges currently faced by accounting education (Wang & Jing, 2018; Zhao, Huang & Chen, 2017). At the same time, it serves as a warning to universities that continue to focus solely on training operationally- focused professionals (Ma, 2020). The design and quality of the accounting curriculum system have a profound impact on both the development of universities and the cultivation of students, influencing societal progress and the future career readiness of graduates.

2.2 Curriculum System Planning

In January 2018, China’s Ministry of Education promulgated the National Standards for Teaching Quality of Undergraduate Programs in Regular Higher Education Institutions, establishing principled guidelines for universities to design discipline-specific talent development objectives. The National Standards for Teaching Quality in Business Administration (Accounting Major) explicitly defines the accounting program’s mission: to cultivate well-rounded professionals. The specific training objectives are articulated as follows: “The undergraduate accounting program aims to nurture talent aligned with the demands of socialist market economy development, equipping students with humanistic literacy, scientific rigor, and professional ethics. Graduates must attain proficiency in accounting, management, economics, law, and computer applications, complemented by practical competencies and communication skills. Upon completion, they shall be qualified for accounting and related positions across diverse sectors—including commercial enterprises, financial institutions, intermediary organizations, government agencies, and public institutions—as applied, interdisciplinary, internationally adaptable, and innovative specialists” (Ministry of Education of the People's Republic of China, 2018).

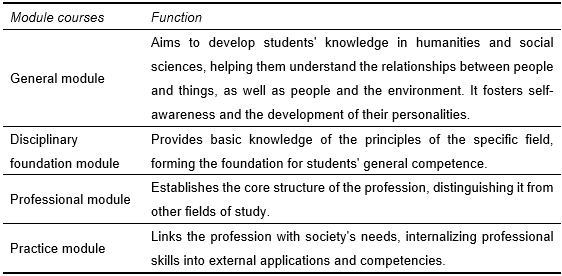

At universities in China, the curriculum system for talent development programs is generally divided into several modules, including general education, disciplinary foundations, specialization, and practical application (as shown in Table 1). To effectively achieve talent development goals, a curriculum system must be systematically planned to ensure that students acquire the most appropriate knowledge content at the most suitable time. Generally, education and socio-economic development exhibit an interactive and evolutionary relationship. Centered on the fundamental principles and core knowledge framework of accounting, the curriculum should be designed to progress in a logical sequence: from easy to difficult, from simple to complex, from concrete to abstract, and ultimately from abstract back to concrete. This progression facilitates a structured transformation of knowledge, ensuring that students, upon completing each stage of learning, possess the essential knowledge and competencies required for that level (Cai & Jiang, 2021).

As universities are the primary institutions for undergraduate talent development, they must not only address the talent needs of society but also consider changes in the external economic environment. Universities must actively optimize their curriculum systems to produce graduates who can adapt to societal development and meet the qualifications demanded by employers in the accounting profession. The effective implementation of talent development objectives depends on the design of the curriculum system, which should enable students to achieve more efficient and structured learning outcomes throughout their studies. These requirements genuinely reflect the distinctive characteristics and core essence of the accounting discipline, while also posing significant challenges to the quality of talent development in university education programs (Zhou, Cui, Liu, & Song, 2016).

Table 1

Classification of Undergraduate Talent Development Curriculum Modules

2.3 Current State of Accounting Education

With the continuous innovation and development of China’s economy and emerging technologies, the competencies required of accounting professionals are also evolving. However, universities are unable to respond to market changes as rapidly as businesses, resulting in a persistent gap between the two. This gap primarily stems from the stark differences in the environments in which universities and enterprises operate. Universities exist in relatively stable settings where economic changes occur gradually, whereas businesses must continuously adapt to ongoing social and economic transformations (Bloom, Collins, Fuglister, & Heymann, 1994). Due to the relative lag in academic research (Moser, 2012), the influence of accounting research on the accounting profession and practice remains somewhat limited (Basu, 2012; Kaplan, 2011). Consequently, its role in guiding and reforming accounting education is also relatively weak (Duff et al., 2020). As a result, higher education in accounting faces significant challenges.

The effective training of graduates who can meet the human resource demands of the accounting market has not yet been widely achieved (Liu, 2020). Research by Zhang and Zhu (2015) indicates that the talent cultivation curriculum for undergraduate accounting programs in many Chinese universities has remained largely unchanged for an extended period—course titles, content, and even instructors have shown little variation over time. This prolonged stability has led to a consistent level of teaching quality, which, rather than serving as a distinctive competitive advantage, has often become a source of criticism from both students and employers. Common concerns include an outdated curriculum system, a professional structure misaligned with core disciplinary knowledge, and a lack of responsiveness to the evolving societal demand for accounting expertise (Altbach, Reisberg, & Rumbley, 2009; Liu, 2020; Zhao & Ren, 2020). Moreover, many regional universities design their curriculum based on faculty members' personal interests rather than the real needs of society. This often results in a narrow, outdated, and unstable curriculum system that does not meet the demands of employers (Bai, 2020; Xi, 2022).

To address the challenges currently facing accounting education, a comparative analysis of the current structure of accounting talent development curriculum systems is needed. Comparative research not only helps to identify the strengths and weaknesses of curriculum structures across different universities, but more importantly, it allows universities to learn from each other's successful planning experiences. This approach can contribute to improving the overall quality of accounting education and raising the professional standards of the discipline.

3 CURRICULUM DESIGN ANALYSIS

3.1 Talent Development Goals at the Six Universities

Within the context of China’s higher education philosophy, national development, and social progress, the formulation of talent development objectives serves as the primary and foundational element in constructing the entire educational system (Zhang, Long, Xiao, & Wu, 2020). However, there has long been debate regarding the cultivation of specialized versus professional talents, and the emphasis on training application-oriented, interdisciplinary talents capable of integrating theory with practice. Clarifying these concepts is essential for better understanding the educational perspectives emphasized in talent cultivation objectives. The term "specialization" originates from specialize. In the fields of science and science education, it refers to focusing time and energy on a specific direction while excluding other possibilities (Etymonline, 2025a). In contrast, "professionalization" derives from the Latin word professionem, whose original meanings include devotion, organization, and occupation (Etymonline, 2025b). Specifically in the context of professional development, both concepts pertain to the categorization required by the demands of occupational division of labor. However, the semantics of "specialization" emphasize functional differentiation and expertise in distinct domains, whereas "professionalization" is more closely associated with the implications of professional ethics (Zheng, 2017).

Specialized talent refers to individuals with technical capabilities in "specific areas," typically possessing specialized skills or knowledge within a narrow scope. This highlights proficiency in a particular technique or function and may not necessarily require a comprehensive theoretical foundation. Such specialization is commonly found in technical or operational roles—for example, "machining specialists" or "software testing specialists." In contrast, professional talent involves the integration of systematic theoretical knowledge with practical application, governed by industry standards. It refers to individuals who have undergone formal education or professional training (such as higher education or certification) and possess both theoretical and practical competencies within a specific "professional field"—for instance, law, medicine, or engineering. These individuals generally meet society's established normative standards for their profession, as seen in "accounting professionals" or "medical professionals" (Becker, 1964; Freidson, 2001; Xinhua News Agency, 2010). Composite talent, meanwhile, refers to individuals who can integrate knowledge across disciplines and specialties, exhibiting interdisciplinary thinking and perspectives. This includes the integration of knowledge, skills, and cognitive approaches, thereby fostering well-rounded, multifaceted individuals (Ministry of Education of the People's Republic of China, 2018).

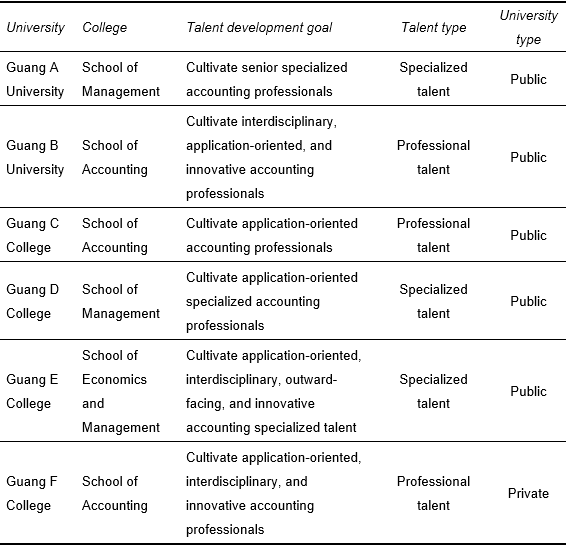

Among the six universities, three focus on cultivating "specialized talent," while the other three focus on "professional talent" (as shown in Table 2).

Table 2

Comparison of Talent Development Goals at the Six Universities

Note: This data was organized by the researcher. The university names are represented by codes.

Note: This data was organized by the researcher. The university names are represented by codes.

Excessive emphasis on "specialized talent" in talent cultivation presents several shortcomings. First, it fails to align with the competencies required of generalist, applied, interdisciplinary, and innovative accounting professionals. Second, curriculum planning may result in outdated content and a disconnect from societal needs at the technical level, thereby weakening students’ employment competitiveness (Hu, 2024). Third, it can mislead students into believing that four years of undergraduate study have already made them high-level specialists, leading to an inflated self-assessment and a tendency to dismiss entry-level positions (Wu, Chen, & Zhao, 2021). University education is a form of professional education, which does not require students to master every subject in great depth during their studies. Rather, they should gain a clear understanding of the core aspects of their chosen field, identify their interests, and continue to explore and deepen their expertise as needed (Wu & Wang, 2017).

3.2 Total Graduation Credits Required

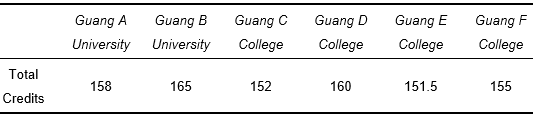

According to the "National Standards for the Teaching Quality of Undergraduate Programs in General Higher Education" published by the Ministry of Education of the People's Republic of China, the total credits required for the Accounting program in business administration should not be less than 140 credits, with no more than 85% of these credits derived from classroom teaching courses (Ministry of Education of the People's Republic of China, 2018). As shown in Table 3, the total graduation credits required by the six universities range from 151.5 to 165 credits, with a 13.5-credit difference between the universities with the highest and lowest credit requirements. Lu (2015), Hu, Zhu, and Qin (2016) point out that a higher number of required credits does not necessarily lead to better learning outcomes, as it may result in a "paradigm trap."

They further note that in many foreign universities, undergraduates are required to complete only 120 to 130 credits. Thus, they argue that the total number of credits is not the most important factor; what matters is whether the curriculum plan aligns with the core competencies of the profession. The focus should be on designing a curriculum that meets the needs of employers and satisfies the fundamental requirements of the accounting profession in the context of a knowledge-driven and technologically advanced economy. Only by doing so can universities effectively train contemporary accounting professionals and ensure the quality of the talent they produce.

Table 3

Comparison of Total Graduation Credits Required by Six Universities

3.3 General Education Curriculum Module

General education (also referred to as liberal education) is designed with the curricular aim of preventing premature specialization and dismantling rigid boundaries between academic disciplines. Its purpose is to broaden students' knowledge and foster a more holistic intellectual perspective. This is especially important in today’s higher education landscape, where universities often place excessive emphasis on employability skills and specialized knowledge, resulting in a narrow and unbalanced educational orientation (Huang, 2015; Wu & Wang, 2017). The goal of general education is to teach students how to live and interact in society, fostering an understanding of human relationships, human-environment interactions, and the development of balanced and well-rounded personalities. It encourages students to adapt to interpersonal relationships and societal needs while cultivating social responsibility and humanistic values.

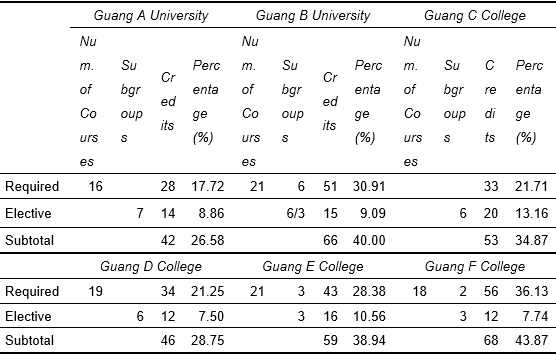

Currently, China’s Ministry of Education has not established explicit restrictions or requirements concerning the proportion of credits allocated to general education modules; instead, this is independently regulated by each university through its own institutional policies. As seen in Table 4, three of the six universities have planned for general education credits to exceed 30%. Among them, Guang F College has the highest proportion, with 68 credits (43.87%). It is evident that each university adopts a distinctive approach to designing general education curriculum modules, marked by substantial differences in educational philosophy and diverse considerations in the planning process. He and Li (2013), and Liu and Du (2021), observe that while domestic accounting education reforms are actively exploring general education and practical teaching, there has been no significant improvement in the quality of accounting talent cultivation.

Table 4 shows that the universities further divide their general education modules into subcategories. Guang A University has seven subcategories, Guang B University has nine, and Guang C College, Guang D College, and Guang E College each have six subcategories, while Guang F College has five. For example, the seven subcategories at Guang A University include: History and Culture, Philosophy and Logic, Society and Economy, Science and Technology, Arts and Aesthetics, Innovation and Entrepreneurship, and Sports and Health. Guang B University, on the other hand, has nine subcategories. The first six offer both required and elective courses, while the last three are elective: Ideology and Politics, Nature and Technology, Literature and Arts, Sports and Health, Innovation and Entrepreneurship, Expression and Communication, Interdisciplinary and Interprofessional Studies, Rule of Law and Society, and Thinking and Methods.

Table 4

Comparison of General Education Credits and Their Proportions at Six Universities

Note (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

Note (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

Dividing the modules into subcategories is beneficial because it provides a clearer reflection of the relationship between general education and professional courses. The advantage of this approach is that it enables the integration of different professional fields, making "general education" and "professional education" complementary and mutually reinforcing. The breakdown of subcategories also shows that universities emphasize broadening and integrating knowledge across various fields such as ideological politics, humanities, social sciences, and natural sciences. This structure offers students distinct, expansive, and diverse options.

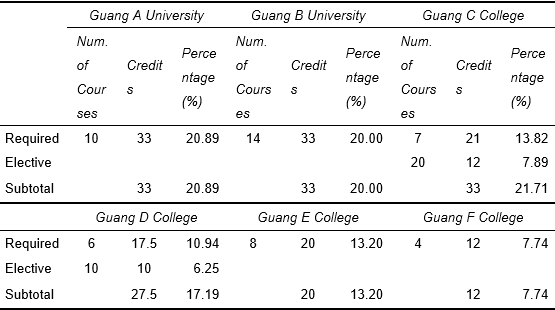

3.4 Subject Foundation Curriculum Module

The subject foundation module consists of elements that are consistent with the professional knowledge of the subject, forming a curriculum module that helps develop foundational concepts within the academic system. This not only provides students with a solid base of professional knowledge but also allows them to expand their expertise based on their personal development needs. The module emphasizes the intrinsic value of the subject's professional discipline and core knowledge (Chen & Guo, 2017; Xie, Zhang, & Wang, 2020). As shown in Table 5, there are still notable differences in the planning of subject foundation courses across universities. These modules typically include courses in mathematics, management, economics, and related fields, which are influenced by factors such as faculty resources, student quality, and available educational infrastructure.

Guang A University and Guang B University each offer 10 courses (33 credits) and 14 courses (33 credits), respectively, with the former accounting for 20.89% and the latter 20.00% of the total required graduation credits. In contrast, Guang F College plans only 4 courses (12 credits, or 7.74%) in this module.

Table 5

Comparison of Subject Foundation Courses and Their Proportions at Six Universities

Note: (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

Note: (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

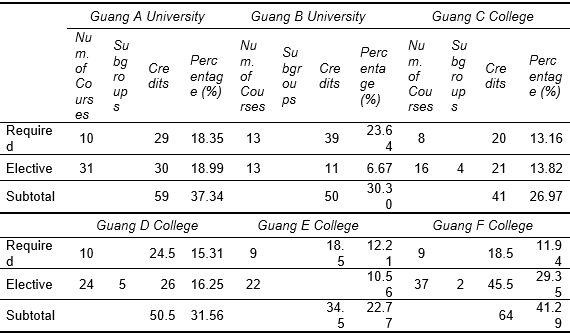

3.5 Professional Course Modules

As shown in Table 6, there are notable differences in the professional course modules planned by the universities. For example, Guang F College offers 46 courses, totaling 64 credits (41.29%), whereas Guang E College provides 31 courses with 34.5 credits (22.77%). In the planning of professional elective courses, a more flexible, modular approach is adopted, with smaller, independent subcategories that allow students to choose courses in specific fields of interest. For instance, Guang C College divides its courses into four subcategories: General Foundation, Big Data, Financial Accounting, and Corporate Accounting, requiring at least 21 credits. Guang D College offers five subcategories: General Foundation, Management Accounting, Auditing, Big Data, and Corporate Accounting, requiring at least 26 credits. Guang F College, in contrast, has only two subcategories: General Courses and Professional Elective Courses, with the former requiring 30.5 credits and the latter 15 credits. This approach helps make the curriculum more practical and better aligned with the needs of societal development.

In terms of international perspectives and digitalization-related courses, such as International Taxation, International Accounting, IT Auditing, Big Data Analytics/Auditing/Finance, and Python and Data Analytics, it is evident that Guang E College and Guang F College are relatively conservative in offering these courses compared to other universities. As cloud accounting and the internet continue to evolve, and as big data becomes widely applied in computerized accounting practices, offering such courses could help improve students’ overall competence in accounting (Yang, 2021).

Table 6

Comparison of Professional Course Credits and Proportions at Six Universities

Note: (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

Note: (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

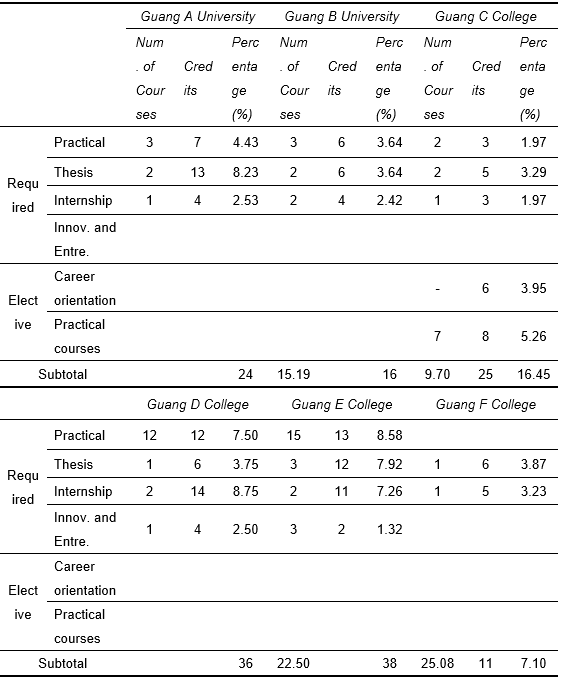

3.6 Practical Course Modules

Practical courses are generally divided into several categories, including practical courses, thesis courses, internship courses, innovation and entrepreneurship courses, and career-oriented courses. As shown in Table 7, Guang E College (25.08%) and Guang D College (22.50%) have a higher proportion of practical courses (over 20%), while Guang F College (7.10%) and Guang B University (9.70%) have a lower proportion. Guang E College offers 15 practical courses (8.58%), seven of which are coordinated with theoretical courses, such as Cost Accounting Experiment in conjunction with Cost Accounting, Management Accounting Experiment with Management Accounting, and Financial Management Experiment with Financial Management. The thesis module requires 12 credits (7.92%) and includes courses such as Yearly Thesis I, Yearly Thesis II, and Graduation Thesis. The internship module requires 11 credits (7.26%), with courses such as Professional Internship and Graduation Internship. In contrast, Guang F College offers only thesis (3.87%) and internship (3.23%) courses. Overall, Guang E College and Guang D College place a stronger emphasis on practical courses compared to the other four universities.

Table 7

Comparison of Practical Course Module Planning at Six Universities

Note: (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

Note: (1) Guang A University Talent Development Plan, 2018 edition; (2) Guang B University Talent Development Plan, 2020 edition; (3) Guang C College Talent Development Plan, 2019 edition; (4) Guang D College Talent Development Plan, 2020 edition; (5) Guang E College Talent Development Plan, 2020 edition; (6) Guang F College Talent Development Plan, 2019 edition.

The division between practical and theoretical courses is a distinctive feature at Guang E College, which is not seen in the other five universities. This approach may help prevent instructors from teaching these courses purely from a theoretical perspective. However, it could also lead to a situation where theory and practice are treated as separate entities. Regarding this teaching method, Li and Wang (2023) noted that traditional teaching typically involves first delivering a comprehensive lecture on theory and methods, followed by specific training sessions at a later stage. This structure often results in a disconnect between theory and practice. They suggest that theory and practice should be taught concurrently so that students can better understand how accounting theory integrates with various job roles. This concurrent approach is adopted by the other five universities. If the same instructor teaches both theory and practice within the same semester, there may not be significant issues. However, if different instructors or semesters are involved, it could result in fragmented knowledge, where the cohesive understanding of a single course becomes disjointed and superficial. Although Guang E College's approach is well-intentioned, it must be carefully implemented to avoid such fragmentation.

From the perspective of credit allocation, the highest and lowest proportions differ by 27 credits (17.98%)—38 credits versus 11 credits (25.08% vs. 7.10%). While a high allocation of credits to practical courses can help students develop essential skills and improve their hands-on capabilities, it may also result in the production of operational workers rather than applied or interdisciplinary professionals. This could reduce students' adaptability in the workforce. Moreover, this approach risks neglecting the development of key financial analysis and management decision-making skills that are central to accounting education. Additionally, an excessively high proportion of practical courses might reduce the space available for other important modules. For instance, Guang E College's professional course module accounts for just 22.77%, the lowest among the six universities. In contrast, Guang D College allocates 22.50% to practical courses, but its professional course module is set at 31.56%, which is 8.79% higher than that of Guang E College (31.56% – 22.77%). The various course modules are complementary and have a sequence in terms of learning. The proportion of credits allocated to each module influences the number of courses offered. Therefore, an excessively high proportion of one module should be adjusted to ensure a more balanced and beneficial curriculum for students pursuing this major.

4 CONCLUSION AND RECOMMENDATIONS

4.1 Conclusion

Although the six universities differ in the total number of credits required for graduation, all meet or exceed the minimum credit requirements set by the Ministry of Education of China. In terms of the general education module, three universities allocate more than 30% of total credits to this area—likely due to differences in institutional history, type, scale, and available educational resources. The disciplinary foundation module, which serves as the cornerstone for developing students’ professional knowledge, typically integrates courses in management, finance, and economics. This facilitates interdisciplinary alignment with applied fields relevant to contemporary accounting. Universities with either excessively high or low credit allocations in this module should consider making appropriate and reasonable adjustments. The design of the professional module reflects a university’s commitment to cultivating students’ core professional competencies. Among the general education, foundational, and practical modules, the professional module holds the highest intrinsic and essential value. It provides top-level guidance for accounting education, embodying the structure, logic, and disciplinary value of the profession. This represents a rigorous and systematic form of disciplinary knowledge.

After comparing the talent cultivation program curricula of six institutions, we found that “Guang A University” demonstrates a more robust and rational overall curriculum design. “Guang D College” and “Guang C College” adopt a tiered structure in their specialized elective course planning, which enhances the quality of their professional offerings. Accounting professionals often face workplace challenges in environments such as multinational corporations, large enterprises, government agencies, and accounting firms—institutions that typically demand a higher level of professional expertise than small and medium-sized enterprises or micro-enterprises. Institutions like “Guang E College” and “Guang F College”, which may lack sufficient qualified faculty or fail to incorporate courses addressing international accounting perspectives (such as those related to the Belt and Road Initiative), accounting digitalization, and the application of AI in accounting, risk falling behind. If their talent cultivation programs are not aligned with the evolving needs of contemporary enterprises and the digital transformation of the accounting field, the future competitiveness of their accounting graduates may be compromised. The accounting profession places significant emphasis on the practical application of theoretical knowledge, managerial competencies, and a sound level of professional judgment. If the design of professional courses is inaccurate, insufficient, or overly narrow, students' professional knowledge may become too limited, hindering the development of broader professional perspectives (Jiang, 2020).

In comparative educational research, understanding the strengths and weaknesses of different curriculum plans is crucial. It is also essential to learn from the experiences and best practices of other institutions. The proportions of various curriculum modules directly impact the course structure and the achievement of talent development goals. Excessive or insufficiently designed modules could crowd out space for other vital components of the curriculum, potentially narrowing the breadth and depth of accounting knowledge and weakening its alignment with the development of high-quality human resources. Interestingly, when comparing the six universities' rankings in the 2022-2023 China Undergraduate University Rankings (China Science and Education Evaluation Network, 2024), it is apparent that the higher-ranked universities tend to have better-planned talent development programs.

4.2 Recommendations

Each module within a talent development program holds equal importance. High-quality accounting professionals should possess expertise in areas such as accounting management, digitalization, big data analytics, international accounting standards, global perspectives, and strategic thinking. Universities that have either overly emphasized general education or practical course modules, or those with insufficient professional courses, should adjust their module proportions to ensure the core principles of accounting education are upheld.

It is recommended that universities introduce courses focused on digital accounting, accounting with artificial intelligence, international perspectives in accounting, and strategic thinking in accounting. These courses will enable students to understand and master the digital and AI competencies required in modern accounting practice, thus improving their expertise in smart accounting. This approach will enhance students' professional core competencies and increase their competitiveness in the job market. The curriculum should align with current trends and technological developments to prepare students for careers in high-quality accounting roles. Regarding Guang E College's decision to split a single course into two separate courses—one theoretical and one practical—this approach warrants further consideration. While it may be an innovative teaching method that reinforces students' theoretical knowledge, it could potentially enhance learning outcomes. However, this division is not observed in the curriculum plans of the other five universities, making it an area for further exploration.

4.3 Scope and Limitations of the Study

This study is limited to analyzing the talent development programs of six universities in Guangdong Province and does not include universities from other regions. Future research could expand the scope by comparing talent development curriculum plans across different countries and institutions. A comparative study between universities in various countries within the same academic field could provide deeper insights and offer a broader perspective. Additionally, conducting surveys with alumni who have graduated with an accounting degree could help refine future talent development programs and contribute to the scientific development of accounting curricula.

REFERENCES

Achalapathi, K. V., & Janakiram, M. (2016). Accounting education in India: A comparative analysis. Indian Journal of Accounting, XLVIII(2), 1-6.

Altbach, P. G., Reisberg, L., & Rumbley, L. E. (2009). Trends in global higher education: Tracking an academic revolution. A Report Prepared for The UNESCO 2009 World Conference on Higher Education, Paris.

Bai, D. H. (2020). A brief discussion on the employment crisis and countermeasures for accounting majors in the age of artificial intelligence. China Management Informationization, 23(20), 228-229.

Basu, S. (2012). How can accounting researchers become more innovative?. Accounting Horizons, 26(4), 851-870.

Becker, G. (1964). Human capital: A theoretical and empirical analysis, with special reference to education. Columbia University Press, New York.

Bloom, R., Collins, M., Fuglister, J., & Heymann, H. (1994). The Schism in Accounting. Praeger Publishers Inc.

Cai, H. Y., & Jiang, K. (2021). Classical patrimony, not just for commemoration——Collected works of Jean Piaget, a must-read. Psychological Research, 14(2), 191-192.

Chen, N., & Guo, Y. X. (2017). The connotation and features of the discipline curriculum concept and its attention on teaching. Curriculum, Teaching Material and Method, 37(8), 11-16.

China Science and Education Evaluation Network. (2024, November 10). 2024-2025 China university overall competitiveness rankings. http://www.nseac.com/eva/CUcompallE.php

Das, S. C., & Singh, R. K. (2018). Accounting education in India and USA: A comparative study. Journal of Commerce & Accounting Research, 7(1), 54-64.

Deloitte. (2017). What key competencies are needed in the digital age? The impact of automation on employees, companies and education.https://www2.deloitte.com/content/dam/Deloitte/ch/Documents/innovation/ch-en-innovation-automation-competencies.pdf

Duff, A., Hancock, P., & Marriott, N. (2020). The role and impact of professional accountancy associations on accounting education research: An international Study. The British Accounting Review, 52(5), 100829.

Etymonline (2025a, July 20). Etymology of "specialisation". Online Etymology Dictionary. https://www.etymonline.com/cn/word/specialisation

Etymonline (2025b, July 20). Etymology of "profession". Online Etymology Dictionary. https://www.etymonline.com/tw/word/profession

Fang, Y. S. (2022). Structure design of accounting undergraduate talent cultivation curriculum model planning: Examples of five universities in Zhejiang province, China. Regional and Cultural Studies, 3(4), 68-80.

Freidson, E. (2001). Professionalism, the third logic: On the practice of knowledge 1st. University of Chicago Press.

Gao, L. (2016). An innovation of college career guidance curriculum based on social interactive model of instruction. Education & Social Sciences, (1), 32-38. https://doi.org/10.14121/j.cnki.1008-3855.2016.01.008

He, Y. R., & Li, X. H. (2013). Study on accounting professional talents education modes——An investigation based on ten famous universities in US. Accounting Research, (4), 26-31+95.

Hu, C. H. (2024). Ideas and practices for building the accounting curriculum system in the context of digital intelligence — A case study of the accounting program at Wuhan textile university school of international business and trade. Journal of Mudanjiang College of Education, (1), 20-23+61.

Hu, J., Zhu, H., & Qin, G. Y. (2016). How much work time is needed for a bachelor degree: An international comparative study on credit hours. Fudan Education Forum, 14(1), 87-92.

Huang, J. J. (2015). The philosophy and practice of university general education. Taipei: National Taiwan University Press.

Huang, Q. Q. (2021). Design of review teaching based on improving core accounting literacy and cultivating key competencies — A case study of "accounting subjects and accounts" review teaching in secondary vocational schools. Occupation, (21), 36-38.

Jackson, D., Richardson, J., Michelson, G., & Munir, R. (2022). Attracting accounting and finance graduate talent – beyond the Big Four. Accounting & Finance, 62(3), 3761-3790. https://doi.org/10.1111/acfi.12904

Jiang, Y. F. (2020). Research on the differences in accounting undergraduate education in Chinese universities. Commercial Accounting, (3), 120-122.

Kaplan, R. S. (2011). Accounting scholarship that advances professional knowledge and practice. The Accounting Review, 86(2), 367-383.

Li, H. W., & Wang, L. (2023). Exploring the construction of the practical teaching system for accounting majors in applied undergraduate universities. Knowledge World, (11), 93-95.

Liu, F., & Du, X. Q. (2021). Accounting general education: Theory and practice. China University Teaching, (7), 58-63.

Liu, H. P. (2020). Analysis of key competencies required for accounting talent to be competent in accounting positions. Marketing Circles, (48), 88-89.

Liu, S. (2024). Enhancing accounting talent training: Innovative feedback and improvement mechanisms for the new business environment. Asia Pacific Economic and Management Review, 1(4), 1-6. https://doi.org/10.62177/apemr.v1i4.9

Liu, X. L. (2020). Research on the construction of the accounting curriculum system and accounting education methods — Review of "principles of accounting". Yangtze River, 51(4), 235.

Lu, X. D. (2015). On quantity of learning. China Higher Education Research, (6), 38-48.

Ma, C. H. (2020). Current development status and trends of the accounting industry. Today's Wealth (China Intellectual Property), (9), 90-91.

Ministry of Education of the People's Republic of China. (2018). National standards for teaching quality of undergraduate majors in general higher education institutions. Beijing: Higher Education Press, pp.849-850.

Ministry of Education of the People's Republic of China. (2024, November 10). List of higher education institutions in China.http://www.moe.gov.cn/jyb_xxgk/s5743/s5744/A03/202110/t20211025_574874.html

Moser, D. V. (2012). Is Accounting research stagnate?. Accounting Horizons, 26(4), 845-850.

Wang, W. F. & Jing, Y. P. (2018). Research on the practical teaching problems and countermeasures with the positioning of high-quality application-oriented talents——A case study of undergraduate economics and management major. Journal of National Academy of Education Administrat, (3), 56-62.

Wu, Q. S., & Wang, L. Y. (2017). Analysis and Improvement of the structure of general education courses in public universities. Curriculum and Teaching, 20(1), 1-23. http://dx.doi.org/10.6384/CIQ.201701_20(1).0001

Wu, Z. F., Chen, J., & Zhao, C. F. (2021). Achieving bidirectional improvement in professional education and talent cultivation quality. China Higher Education, (12), 59-61.

Xi, C. L. (2022). A Survey on the Current Situation and Countermeasures of Accounting Education + Innovation and Entrepreneurship Integration. China Steel Focus, (3), 196-198.

Xie, M. H., Zhang, J. X., & Wang, J. (2020). Research on the construction of the characteristics of the accounting undergraduate program and innovation in talent cultivation — A case study of five comprehensive universities. Journal of Higher Education, (13), 1-7.

Xinhua News Agency. (2010). National medium- and long-term talent development plan (2010–2020) released. Central People's Government of the People's Republic of China. http://big5.www.gov.cn/gate/big5/www.gov.cn/jrzg/2010-06/06/content_1621777.htm

Yang, Q. M. (2021). Analysis of the impact of big data on financial accounting. Economic Management Digest, (16), 148-149.

Zhang, X. M., & Zhu, J. G. (2015). The core curriculum construction of undergraduate accounting major: Way to break though. Accounting Research, (8), 80-85.

Zhang, J., Long, Y. E., Xiao, F., & Wu, Z. F. (2020). Enhancing the quality of accounting professionals cultivation in local universities. China Higher Education, (18), 59-60. doi:CNKI:SUN:ZGDJ.0.2020-18-034.

Zhao, F. Q., Huang, H. Y., & Chen, Y. (2017). An international comparison of cultivating internationalized talents for the human resources management of university and its reference. Contemporary Economic Management, 39(2), 66-72.

Zhao, L., & Ren, L. Y. (2020). Research on the talent cultivation mode for accounting undergraduates in China in the context of informationization. Marketing Circles, (52), 110-111.

Zheng, Z. C. (2017). Specialization and professionalization. Journal for Studies of Everyday Life, (15), 135-136.

Zhou, W. Y., Cui, Y. K., Liu, L. L., & Song, Y. D. (2016). Empirical research of school curriculum planning quality——Based on a text analysis of junior high school curriculum planning in city Z. Global Education, 45(9), 53-61.

Additional information

Código JEL: M40