INTRODUCTION

The information that society may have about the proposals for reforms to the tax legislation contributes to the formation of criteria, it is important that the population has access to information on the implications of the proposals presented.

It is important to note that in the face of the proposal to tax value added tax on services provided through the various platforms, the edges it presents for society must be analyzed, from the point of view of the consumer and the owners of the platforms.

To meet expectations, it is necessary to make use of the information that can be had in relation to the subject, although, in other countries have proposed reforms to their legislation regarding the aforementioned tax, the results have been published for analysis.

In Mexico, online commerce1 is a growing economic activity, the sale of services, platforms for playing music and videos, among others have permeated society from the consumer, service providers to the same companies, as well as the electronic businesses themselves with residence in the country and managed by nationals; this commercial activity represents 4.6% of the gross domestic product (INEGI 2017) which the regulation of the same can reduce the use of these platforms and affect the user, which according to VAT is a tax paid by the end user.

METHODOLOGY

The research is descriptive, the research method used is the inductive, aided analysis-synthesis. The type of analysis carried out is theoretical, comparative, content and critical, since it is based on documentary research, which is why the results of similar fiscal initiatives in Latin American and European countries were analyzed, in such a way that it would be possible to define an analytical framework of the possible implications of the proposal.

DEVELOPMENT

On the eighth of September, the Ministry of Finance and Public Credit presented to the H. Congress of the Union the Economic Package for the 20202 fiscal year, in this proposal were integrated General Criteria of Economic Policy, initiative for the Revenue Law of the federation, as well as reforms to the income tax laws (ISR), Value Added Tax (VAT), Special Tax on Production and Services (IEPS), as well as the budget of expenditures of the federation among others.

In this draft, it proposes adaptations to the current rules; with regard to the VAT Law, regulations on digital activities and the identification of businesses for tax purposes are identified.

In conjunction, technological development means supporting a country’s long-term economic growth. Innovation policies, related to science and technology, are essential to effectively link the efforts of businesses, governments and academia. (Prats, Hernández, Santiago & de la Torre, 2021)

To identify the concept of digital activities makes references to platforms that offer services or intangible acquisitions, provided by residents abroad without establishment in the national territory, these services are taxed as an import and the obligor to pay is the final consumer or the intermediary, currently due to ignorance of the legislation, the end consumer is not paying for it.

The economic policies proposed, seek to regulate a form of consumption of services that is growing among the population, with the use of Communication Technologies (ICTS), was the birth of innovative trade activities through electronic means.

In this regard (De los Santos, et al., 2020). He mentions that global interconnectivity and globalized economic approaches generated changes in the competitiveness schemes to which commercial banking was accustomed, which forced changes and innovations in order to maintain its traditional customers. This approach of the financing offerors is mostly represented by large corporations, which use technological development as a platform for approaching the demanding sectors.

Electronic commerce is an economic activity that has significantly impacted on the continuous improvement of business processes and social response to social and democratic development3, the Organization for Economic Cooperation and Development (OECD) defines it as “the process of buying, selling or exchanging goods, services and information through communication networks”. This economic activity arises for many years, companies exchange data through various communication networks, what was known as traditional electronic commerce, that is, inter-business relations through their own networks. However, with the development of telecommunications and internet access that has permeated society, it has become a growing economic activity.

Four forms of this type of business activity are distinguished according to the agents who interact in the transaction: 4

-

Consumer-to-business e-commerce.

-

Business-to-consumer e-commerce.

-

Consumer-to-consumer e-commerce.

-

Business-to-business e-commerce.

By the volume of transactions, electronic commerce is distinguished from business to consumer and from business to business, the first category refers to the offers of products or services through a digital sideboard or electronic store, considered one of the most common activities of commercial exchanges; the second category consists of business-to-business digital commerce transactions. 5

E-commerce multiplies the base of consumers and sellers of services or goods, this benefits the increase of competition in the market, has a greater range of accessibility by virtue of the fact that it does not have established schedules, that is, you can access the platforms 24 hours a day, 7 days a week, it is comfortable and easy, since no matter the place both parties can connect, this type of trade is changing business models, forms of consumer behavior, as well as economic and political relations around the world.

Currently in Mexico, the consumption of products and services through digital platforms has been increasing, however, the characteristics of trade and the impact it produces on tax collection are unknown, generating administrative and control weakness for the payment of taxes.

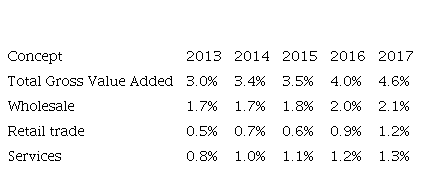

According to INEGI in 2017, the Gross Value Added generated by e-commerce was equivalent to 4.6% of GDP. 6

Table 1

INEGI (2017)

Similarly, in 2018, purchases in electronic commerce with the use of credit and/or debit cards reached 190,633 million pesos, 46% more than in 20177.

INEGI (2017)

Similarly, in 2018, purchases in electronic commerce with the use of credit and/or debit cards reached 190,633 million pesos, 46% more than in 20177.

|

Concept

|

2013

|

2014

|

2015

|

2016

|

2017

|

|

Total Gross Value Added

|

3.0%

|

3.4%

|

3.5%

|

4.0%

|

4.6%

|

|

Wholesale

|

1.7%

|

1.7%

|

1.8%

|

2.0%

|

2.1%

|

|

Retail trade

|

0.5%

|

0.7%

|

0.6%

|

0.9%

|

1.2%

|

|

Services

|

0.8%

|

1.0%

|

1.1%

|

1.2%

|

1.3%

|

The various digital platforms that offer services such as accommodation, music, movies, food, transport, among others, generate a financial year so far not taxed for the collection of tax.

Why impose VAT on these services?

Taxes are the contributions established in law to be paid by natural and legal persons who are in the legal or factual situation provided for8 by it as referred to in the Fiscal Code of the Federation. The VAT arises in Mexico through the Law regulating it published on January 1, 1980, it is a tax collection tool that constitutes the second tax of importance collection in the country after the income tax.

The function of VAT collection in the modern state of the law is not limited only to the collection, but seeks to motivate, encourage and promote new behaviors, currently this collection tool is set at a rate corresponding to the 16%9 same that is taxed on:

-

Disposal of property

-

Provision of independent services

-

Giving in use or temporary enjoyment of property

-

Import of goods or services

In the proposal put forward by the Federal Executive, the latter is contemplated as an import of intangible goods and services, these taxes were already contemplated in the law, but in a diffuse way, for which reason this tax was not collected.

Internet companies with tax residence in the national territory are obliged to pay VAT, so, to equalize the conditions with their foreign peers, the modifications in the tax law are considered.

The issue of the tax domicile is important, the digital platforms of services that are consumed in the territory must pay the taxes generated in the commercial exchange, however, the headquarters are located in other countries known as tax havens, this situation harms the collection of the country, consumers and companies of the traditional economy.

From the point of view of the impact caused by the non-taxation of these companies, it is considered that the benefits posed by the economic package 2020, since it proposes solutions to meet the control of these companies that provide their services in Mexico, exploiting the Mexican market without paying taxes.

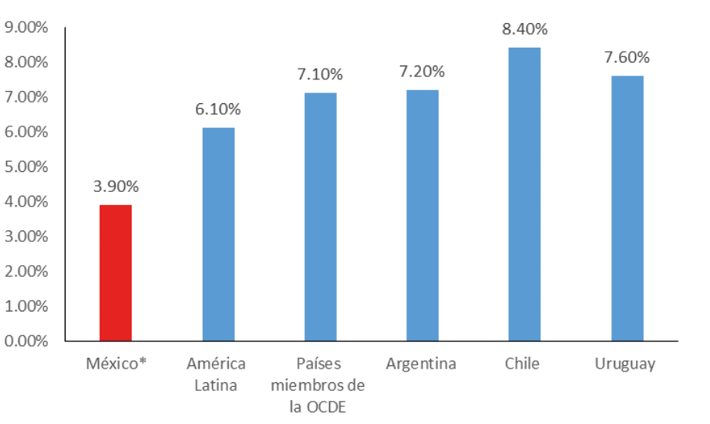

Compared to other Latin American countries (Argentina, Chile, Uruguay) Mexico is below VAT collection; in parallel, digital commerce has increased considerably. 10

Table 2

OCDE (2019)

Table 2

OCDE (2019)

Mexico belongs to the Organization for Economic Cooperation and Development (OECD) along with 34 other countries, an organization that has among its main objectives to support sustainable economic growth, the green economy has become a model to promote economic development Growth, income and job creation, which aims to change the interaction between economic progress and environmental sustainability, especially if The Measure of Wealth takes into account natural assets, not just productivity. (Silva, et. al., 2021) promote employment, improve living standards, maintain financial stability, collaborate with the economic development of other countries, as well as contribute to the growth of world trade; the countries that make up this organization exchange experiences in the application of public policies, identify best practices and promote recommendations, thus making the OECD one of the largest and most reliable sources at the international level in the fields of statistics and economic and social information11.

This organization elaborated in coordination with the G20, in October 2015 the package “BEPS” (Base Erosion and Profit Shifting)12 that refers to the erosion of the tax base and the transfer of beneficial through gaps or unwanted mechanisms between the different national tax systems that can be used by multinational companies (MNEs)., in order to “disappear” profits for tax purposes, or to transfer profits to locations where there is little or no real activity, although it enjoys a low taxation, resulting in little or no income on companies13.

In other words, companies make use of regulatory loopholes in different countries to reduce their tax burden or transfer the profits made by one subsidiary to another located in lower-tax countries14.

The BEPS action plan contains measures aimed at the effectiveness of international tax standards, reinforcing their focus on economic substance and ensuring a fiscal environment of greater transparency, within which we emphasize the following:

With the first action listed, the OECD aims to identify the fiscal challenges and the problems represented by the digital economy, since international regulations are surpassed by this economic activity.

On the second of May 2019 was presented the Economic Study16 conducted by the organization to Mexico, in which it makes an analysis of the economic growth of the country, refers that, although reforms have been made to be more productive and inclusive, the growth of the Mexican economy remains weak, based on these, the organization makes recommendations to substantially improve fiscal activities, thus refers that tax revenues remain low and fiscal policy has little redistributive impact, by making short-term recommendations by improving the efficiency of tax collection and spending will allow the debt-to-GDP ratio to stabilize and provide some room for greater social and infrastructure spending, in the medium term increase tax revenues and modify the tax mix will create more fiscal space and allow to increase progressivity17 .

What is the Tax Reform contained in the 2020 Economic Package?

As noted above, the Federal Government has not contemplated increasing taxes or creating new ones, so the proposals for the new fiscal year are aimed at improving the collection of existing taxes.

Derived from the administrative weakness and the lack of control for the payment of the tax in this type of trade, it is necessary that it be regularized through the legislation, being the service provider who made the transfer and collection of VAT to consumers, the proposal consists of:

“To identify the main challenges posed by the digital economy in the implementation of current international tax rules and to devise comprehensive measures to address these difficulties, taking a panoramic view of this end and considering both direct and indirect taxation. Issues under consideration include, inter alia, the possibility of a company having a significant virtual presence in the economy of another country untaxed due to the absence of a ‘nexus’ under existing international standards, the attribution of value created from the generation of geo-localized marketable data through the use of digital products and services, the qualification of income from new business models, the application of source rules and how to ensure the effective collection of VAT/IBS in respect of the cross-border supply of digital goods and/or services. This work will require a thorough analysis of the different business models in this sector.” 18

This proposal is not generally applicable to services offered through digital platforms, it is proposed to an exclusive category that includes services of final consumption in households or used for individual consumption that are automated; it also states that the tax burden of VAT falls on the final consumer, who acts as payer of the tax; if such products are purchased by companies, the effect is neutral, i.e. it does not generate additional revenue.

In addition to the above, a linking criterion is also contemplated that allows the Mexican tax authority to tax residents abroad without establishment in Mexico, which is in accordance with the means through which they provide the digital services, that is, that they are services and acquisition of intangibles that are provided electronically through platforms or applications via the Internet; in this sense, it is considered that the service is provided in national territory when the recipient of the service is in the aforementioned territory when it is carried out in whole or in part; the digital service is provided to a receiver located in national territory and the consideration that has its origin in Mexico19.

Comparative in the international arena.

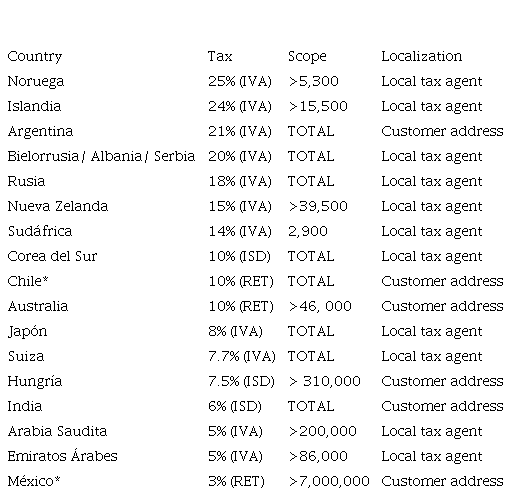

Currently, more than 50 countries have established vat destination principles for the digital economy, have implemented a simplified vat compliance and payment registry on imports of intangible services through digital platforms.

TABLE 3

Florencia, 2019, p. 12.

* Not yet in force

IVA: Value added tax

ISD: Tax on digital services

RET: Withholding. 20

Florencia, 2019, p. 12.

* Not yet in force

IVA: Value added tax

ISD: Tax on digital services

RET: Withholding. 20

|

Country

|

Tax

|

Scope

|

Localization

|

|

Noruega

|

25% (IVA)

|

>5,300

|

Local tax agent

|

|

Islandia

|

24% (IVA)

|

>15,500

|

Local tax agent

|

|

Argentina

|

21% (IVA)

|

TOTAL

|

Customer address

|

|

Bielorrusia/ Albania/ Serbia

|

20% (IVA)

|

TOTAL

|

Local tax agent

|

|

Rusia

|

18% (IVA)

|

TOTAL

|

Local tax agent

|

|

Nueva Zelanda

|

15% (IVA)

|

>39,500

|

Local tax agent

|

|

Sudáfrica

|

14% (IVA)

|

2,900

|

Local tax agent

|

|

Corea del Sur

|

10% (ISD)

|

TOTAL

|

Local tax agent

|

|

Chile*

|

10% (RET)

|

TOTAL

|

Customer address

|

|

Australia

|

10% (RET)

|

>46, 000

|

Customer address

|

|

Japón

|

8% (IVA)

|

TOTAL

|

Local tax agent

|

|

Suiza

|

7.7% (IVA)

|

TOTAL

|

Local tax agent

|

|

Hungría

|

7.5% (ISD)

|

> 310,000

|

Customer address

|

|

India

|

6% (ISD)

|

TOTAL

|

Customer address

|

|

Arabia Saudita

|

5% (IVA)

|

>200,000

|

Local tax agent

|

|

Emiratos Árabes

|

5% (IVA)

|

>86,000

|

Local tax agent

|

|

México*

|

3% (RET)

|

>7,000,000

|

Customer address

|

The table above explains that there are countries that apply VAT, others that impose a withholding tax and those that created a digital tax to tax this activity. In the same way, it refers that at present there is no global policy that homologues the tax rates, since as can be seen in the aforementioned table the tax varies from country to country.

In the global community that seeks the implementation of the control and tax burden on companies that offer online services, derived from the MEETINGS of the OECD, however, according to the zones the works are in less or greater progress.

As far as the European Union is concerned, they have determined that coordination is necessary among its members, presenting a proposal that contemplates the implementation of a tax at European level that taxes certain digital revenues, this proposal seeks that the measures are homogeneous to guarantee equity in economic growth.

The European Commission (EC)21 proposes short-term and transitional measures, until such time as an international regulation is generated to regulate the application of the tax regulatory rate22.

These measures consist of the collection of 3% for income derived from:

-

Advertising aimed at users.

-

Pages in which interaction between users is allowed and facilitates the delivery of goods and services between them.

-

Sale of user data, generated by your digital activity.

These proposals are aimed at countries whose total income exceeds EUR 750 million and EUR 50 million within the European Community. 23

However, the proposal indicated above has not yet been specified, given this situation, the Council of Ministers of Spain approved on October 19, 2018, the draft law through which the Tax on Certain Digital Services, by its acronym IDSD, is created.

This preliminary draft observes a similar mechanism to the project presented by the European Commission, making Spain the first member of the European Union to implement taxes on digital platforms, starting with a rate of 3% for the provision of online advertising services, online intermediation services and the sale of data generated from information provided by the user. 24 (Error 18: La referencia debe estar ligada) (Error 19: El tipo de referencia es un elemento obligatorio) (Error 20: No existe una URL relacionada)

The economic impact on this tax has been analyzed in the short term, taking into consideration the deficiencies and failures within the Tax on Certain Digital Services, according to the digital page civismo.org the economic cost along the value chain is diverse, that is to say the effects on the supply, wholesale market are analyzed, retail and consumer market.

According to data collected in Spanish organizations, Banco de España and Sector Reports, they have determined that the IDSD will negatively affect digital commerce in the Spanish territory, as well as the purchases of Spaniards from abroad. They report discrimination in the domestic market, equivalent to 36.5% of all digital transactions and abroad.

Likewise, the application of a rate of 3% of IDSD would imply a reduction of the gross margin on the net amount of turnover up to two percentage points, this according to data provided by the Central Balance Sheet of the Bank of Spain.

As far as supply is concerned, they say that it will be reflected in the decrease in the market value of rights, as well as the redistribution of income with waterways where added value escapes.

In the wholesale market, the effects they pose are costs of control and settlement of the tax and supposes a tariff on online advertising.

In the retail market the total costs on the value chain are reflected in a possible neutral effect on margins opting for price increases, as well as could incentivize companies to look for legal figures that facilitate tax evasion.

The effect on the consumer may include losses in the surplus, as well as buying goods that are not subject to that tax.

In Latin America, some countries established regulations regarding the application of VAT to electronic goods and services.

In January 2017 Colombia established the regulation for taxes on electronic services purchased through foreign companies, established a 19% tax on these services; this is reflected in the cost that users pay for such a service.

In Argentina25, it was in mid-2018 stipulated a 21% tax for electronic purchases, the Federal Administration of Public Revenues of that country refers that it has generated a collection of 19.1 million dollars; the tax law is subdivided into two categories, those who provide a particular service and those who sell goods or services, being more proactive also regulate applications that, although they do not provide or sell services, offer advertising.

For its part, the government of Chile26, carries out work aimed at tax modernization, makes a difference between natural and legal persons, that is to say for natural persons a charge of 10% is contemplated, which is withheld and paid by banking institutions (credit cards), on the other hand legal entities have a rate that can be up to 35%, however, it is still in the process of validation.

In Brazil27 the taxation is divided by competences, national and municipal, in the national competence two types of taxes are contemplated, the Social Integration Program “PIS” and Contribution to the Social Security Financing “COFINS”, the rate of these two taxes foresees as a minimum the 0.65% and maximum 7.5%; as far as municipal competence is concerned, the tax is fixed according to the municipality in which the service provider is established, having a minimum rate of 2% and a maximum of 5%.

CONCLUSION

The tax applied to digital services is something new, although it has been worked on in previous years, the reality is that most countries are implementing it recently.

As you can see in the European Union they foresee that the tax will be applied uniformly by 2020, seeking commercial equity and causing the least possible damage to the economy of nationals.

In Latin America they are in the process of implementing it, and in the countries in which it has already been applied it has given positive and negative results, however, there is no conclusive opinion regarding its effectiveness.

In our country, expectations are generated regarding the collection, that is, to implement this measure is to improve taxation, which would result in greater revenues to pay for social programs.

From that point of view it seems to be favorable, on the other hand, there is the opinion of consumers, the products and services consumed through this economic activity can suffer an increase in price.

Now, after analyzing the examples of other countries, the goals that have been set, the destination that these resources would have, is there a specific issue, which must be analyzed, what happens with Mexicans who have platforms to offer services and products online? They have their tax domicile registered in national territory, this group of merchants is applied the value added tax for their economic activity, so it is consistent to think that platforms that do not have fiscal domicile in Mexican territory until before the proposal did not apply these taxes; then reforming a law that regularizes this situation would generate an even floor for nationals and internationals, avoid tax evasion due to loopholes in the legislation, and improve opportunities for Mexican entrepreneurs.

The tax on online applications, seems promising with respect to collection and hopefully so, however, the most important thing about this proposal is the fairness of competition that is presented for Mexican entrepreneurs in this area.

REFERENCIAS

Astudillo M., Marcela; Mancilla R., Ma. Enriqueta. La valuación de los bienes intangibles en México. Revista Actualidad Contable FACES, Vol:17 No.28 (2014): 5-20.

De los Santos, L., Fernández, C. G., & Martínez-Prats, G. (2020). Microcréditos, financiamiento alternativo en pymes mexicanas. Publicaciones e Investigación, 14(1).

Florencia Moren, María, El impuesto digital en el mundo, (Argentina: Centro de Estudios en Administración Tributaria, 2019).

Hernández Becerril, Brenda. “Los impuestos: algunas generalidades y su importancia social”. Revista encrucijada. Revista electrónica del Centro de Estudios en Administración Pública. No. 26 (2017): 35-46.

Herreros, Sebastián. La regulación del comercio electrónico transfronterizo en los acuerdos comerciales: algunas implicaciones de política para América Latina y el Caribe, serie Comercio Internacional (Santiago: Naciones Unidas, 2019).

Consejo Europeo. En pos de la unidad: El Consejo Europeo, (Luxemburgo: Secretaría General del Consejo, 2016), 5-87.

Oropeza Doris, Karina. La competencia económica en el comercio electrónico y su protección en el sistema jurídico mexicano, México: IIJ-UNAM, 2018

Prats, G. M., Hernández, F. S., Santiago, M. A., & de la Torre Rodríguez, J. F. (2021). Desarrollo tecnológico e innovación en México.

Ríos Ruíz, Alma de los Ángeles. “Análisis y perspectivas del comercio electrónico en México”. Enl@ce Revista Venezolana de Información, Tecnología y Conocimiento, vol. 11: No. 3 (2014): 97-121.

Recabarren, Soledad, et. alt., “Proyecto de Ley de Modernización Tributaria”, Diálogos Revista de Derecho Aplicado LLM UC, Vol: No. 2 (2018) 2-28.

Roberto Occaso, Carlos. La competencia para el cobro administrativo coactivo y el amigable: estructuras administrativas, alcance, ventajas y desventajas, (Brasil) 1-82.

Silva, F. et. al. (2021). Dimensiones sociales y económicas del uso del recurso hídrico. Bogotá, D. C., Colombia: Editorial Politécnico Grancolombiano.Normativa

Boletín Oficial de las Cortes Generales. 121/000039 Proyecto de Ley del Impuesto sobre Determinados Servicios Digitales. Congreso de los Diputados XII Legislatura, Serie A: proyectos de ley, 25 de enero de 2019, núm. 40-1, pág. 1. Véase https://www.lamoncloa.gob.es/consejodeministros/Paginas/enlaces/191018-enlacedigitales.aspx con fecha 01 de noviembre de 2019.

Código Fiscal de la Federación, Cámara de Diputados del H. Congreso de la Unión, Art. 2° fracción I, Texto publicado en el DOF el 09 de diciembre de 2013.

Comisión Europea, Bruselas, 19.4.2018 COM (2018) 219, COMUNICACIÓN DE LA COMISIÓN AL PARLAMENTO EUROPEO, AL CONSEJO, AL COMITÉ ECONÓMICO Y SOCIAL EUROPEO Y AL COMITÉ DE LAS REGIONES.

Criterios generales de política económica para la iniciativa de ley de ingresos y el proyecto de presupuesto de egresos de la federación correspondientes al ejercicio fiscal 2020. Secretaría de Hacienda y Crédito Público, México.

Gaceta Parlamentaria. Año XXII, Palacio Legislativo de San Lázaro, Número 5361-D, Anexo D http://gaceta.diputados.gob.mx/PDF/64/2019/sep/20190908-D.pdf

Secretaría de Hacienda y Crédito Público. Paquete Fiscal 2020, (SHCP: México, 2019) https://www.gob.mx/shcp/prensa/comunicado-no-082-presentacion-de-la-propuesta-del-paquete-economico-2020

Secretaria de Hacienda y Crédito Público. Paquete Fiscal 2020, México. Fecha de consulta 16 diciembre 2019 https://www.gob.mx/shcp/prensa/comunicado-no-082-presentacion-de-la-propuesta-del-paquete-economico-2020Informes

Awasthi, Rajul, Five Ideas to Help Close International Tax Loopholes, (2014). http://blogs.worldbank.org/governance/plugging-international-tax-loopholes-and-boosting-domestic-resources-call-action-world-bank.

El impuesto sobre los Servicios Digitales en España, consultado en Pricewatherhouse Cooper Asesores de Negocios en la liga pwc_idsd_final_09012019_es%20(1).pdf.

OCDE, Estudio Económico México 2019, (OCDE: México, 2019) http://www.oecd.org/eco/growth/going-for-growth-2018-mexico-spanish-note.htm

OCDE, 10 preguntas sobre BEPS, https://www.oecd.org/ctp/10-preguntas-sobre-beps.pdf

OCDE, Nota explicativa, Proyecto OCDE/G20 de Erosión de Bases Imponibles y Traslado de Beneficios, (OCDE: 2015). https://www.oecd.org/ctp/beps-nota-explicativa-2015.pdf

OCDE, Estudio económico de la OCDE: Economic Survey of Mexico, (OCDE: México, 2019) http://www.oecd.org/economy/surveys/mexico-economic-snapshot/

Recommendation of the council on consumer protection in E-Commerce, Paris, 2016, 3-20.

OCDE, Revisión del gobierno digital en Argentina, acelerando la digitalización del sector público, hallazgos clave, (Argentina: OCDE, 2018), 1-28.

PROFECO. https://www.gob.mx/condusef/prensa/condusef-informa-sobre-las-compras-realizadas-a-traves-de-comercio-electronico-al-cierre-de-2018

Notas

1 Ríos Ruíz, Alma de los Ángeles. “Análisis y perspectivas del comercio electrónico en México”. Enl@ce Revista Venezolana de Información, Tecnología y Conocimiento, vol. 11: No. 3 (2014): 102-104.

2 Criterios generales de política económica para la iniciativa de ley de ingresos y el proyecto de presupuesto de egresos de la federación correspondientes al ejercicio fiscal 2020. Secretaría de Hacienda y Crédito Público, México.

3 Oropeza Doris, Karina. La competencia económica en el comercio electrónico y su protección en el sistema jurídico mexicano, México: IIJ-UNAM, 2018. 5.

4 Oropeza Doris, Karina. El comercio electrónico y principios económico-comerciales, México: IIJ—UNAM, 2018, 11-12.

5 Oropeza, Doris Karina. El comercio electrónico y principios económico-comerciales, México: IIJ—UNAM, 2018, 12.

6 Secretaria de Hacienda y Crédito Público. Paquete Fiscal 2020, México. Fecha de consulta 16 diciembre 2019 https://www.gob.mx/shcp/prensa/comunicado-no-082-presentacion-de-la-propuesta-del-paquete-economico-2020

7 PROFECO. Fecha de consulta 26 de septiembre de 2019 https://www.gob.mx/condusef/prensa/condusef-informa-sobre-las-compras-realizadas-a-traves-de-comercio-electronico-al-cierre-de-2018

8 Código Fiscal de la Federación, Cámara de Diputados del H. Congreso de la Unión, Art. 2° fracción I, Texto publicado en el DOF el 09 de diciembre de 2013.

9 Hernández Becerril, Brenda. “Los impuestos: algunas generalidades y su importancia social”. Revista encrucijada. Revista electrónica del Centro de Estudios en Administración Pública. No. 26 (2017): 38-39.

10 Herreros, Sebastián. La regulación del comercio electrónico transfronterizo en los acuerdos comerciales: algunas implicaciones de política para América Latina y el Caribe, serie Comercio Internacional (Santiago: Naciones Unidas, 2019).

11 Recommendation of the council on consumer protection in E-Commerce, Paris, 2016, 13-18.

12 Awasthi, Rajul, Five Ideas to Help Close International Tax Loopholes, (2014) Fecha de consulta 29 de noviembre de 2019. http://blogs.worldbank.org/governance/plugging-international-tax-loopholes-and-boosting-domestic-resources-call-action-world-bank.

13 OCDE, 10 preguntas sobre BEPS, https://www.oecd.org/ctp/10-preguntas-sobre-beps.pdf consultado el 30 de septiembre 2019. Véase OCDE. Marco inclusivo sobre BEPS de la OCDE y el G-20, Perú, 2018.

14 Florencia Moren, María, El impuesto digital en el mundo, (Argentina: Centro de Estudios en Administración Tributaria, 2019)

15 OCDE, Nota explicativa, Proyecto OCDE/G20 de Erosión de Bases Imponibles y Traslado de Beneficios, (OCDE: 2015). https://www.oecd.org/ctp/beps-nota-explicativa-2015.pdf

16 OCDE, Estudio económico de la OCDE: Economic Survey of Mexico, (OCDE: México, 2019) http://www.oecd.org/economy/surveys/mexico-economic-snapshot/

17 OCDE, Estudio Económico México 2019, (OCDE: México, 2019) http://www.oecd.org/eco/growth/going-for-growth-2018-mexico-spanish-note.htm en fecha de consulta 26 de septiembre de 2019.

18 Gaceta Parlamentaria. Año XXII, Palacio Legislativo de San Lázaro, Número 5361-D, Anexo D http://gaceta.diputados.gob.mx/PDF/64/2019/sep/20190908-D.pdf

19 Secretaría de Hacienda y Crédito Público. Paquete Fiscal 2020, (SHCP: México, 2019) https://www.gob.mx/shcp/prensa/comunicado-no-082-presentacion-de-la-propuesta-del-paquete-economico-2020 Recuperado 15 de octubre de 2019.

20 Florencia Moren, María, El impuesto digital en el mundo, (Argentina: Centro de Estudios en Administración Tributaria, 2019).

21 Comisión Europea, Bruselas, 19.4.2018 COM 219, COMUNICACIÓN DE LA COMISIÓN AL PARLAMENTO EUROPEO, AL CONSEJO, AL COMITÉ ECONÓMICO Y SOCIAL EUROPEO Y AL COMITÉ DE LAS REGIONES, pp. 1-2.

22 Consejo Europeo. En pos de la unidad: El Consejo Europeo, (Luxemburgo: Secretaría General del Consejo, 2016), 31.

23 El impuesto sobre los Servicios Digitales en España, consultado en Pricewatherhouse Cooper Asesores de Negocios en la liga pwc_idsd_final_09012019_es%20(1).pdf.

24 Boletín Oficial de las Cortes Generales. 121/000039 Proyecto de Ley del Impuesto sobre Determinados Servicios Digitales. Congreso de los Diputados XII Legislatura, Serie A: proyectos de ley, 25 de enero de 2019, núm. 40-1, pág. 1. Véase https://www.lamoncloa.gob.es/consejodeministros/Paginas/enlaces/191018-enlacedigitales.aspx con fecha 01 de noviembre de 2019.

25 OCDE, Revisión del gobierno digital en Argentina, acelerando la digitalización del sector público, hallazgos clave, (Argentina: OCDE, 2018), 3-5.

26 Recabarren, Soledad, et. alt., “Proyecto de Ley de Modernización Tributaria”, Diálogos Revista de Derecho Aplicado LLM UC, Vol: No. 2 (2018) 21-24. 2-28

27 Roberto Occaso, Carlos. La competencia para el cobro administrativo coactivo y el amigable: estructuras administrativas, alcance, ventajas y desventajas, (Brasil) 51-53.

Notas de autor

germanmtzprats@hotmail.com