Artículos de investigación científica y revisión del estado del arte

Perceptions of the importance of cost systems within peruvian companies

Percepciones sobre la importancia de los sistemas de costos en empresas peruanas

Percepções da importância dos sistemas de custos nas empresas peruanas

Perceptions de l’importance des systémes de coûts dans les entreprises péruviennes

Julio Hernández-Pajares julio.hernandez@udep.edu.pe

Gino Vivanco-Ruidías gino.vivanco@udep.edu.pe

Julio Hernández-Pajares julio.hernandez@udep.edu.pe

Gino Vivanco-Ruidías gino.vivanco@udep.edu.pe

Costos y Gestión

Instituto Argentino de Profesores Universitarios de Costos, Argentina

ISSN-e: 2545-8329

Periodicity: Semestral

no. 108, 2025

Received: 23 October 2024

Accepted: 17 February 2025

Abstract:

This study explores managers' perceptions of the importance of cost systems in operational and strategic decision-making, as well as the factors influencing these perceptions. Using a relational scope and a quantitative approach, the research is based on a survey of managers responsible for cost systems in Peruvian companies. Factor analysis was employed to identify key perception components, while the Mann-Whitney U and Kruskal-Wallis tests were used to assess the effects of ERP usage and business sector differences. According to the results, standard costing and full costing are the most widely used systems, primarily for financial reporting, profitability analysis, and budgeting, particularly in short-term decision-making. ERP implementation and the business sector moderately influence managerial perceptions. These results provide a basis for future confirmatory studies on the relevance and determinants of cost system adoption. The study underscores the need for enhanced training in analytical tools for cost system managers to improve decision-making at both operational and strategic levels.

JEL: M4.

Keywords: cost accounting, management control, ERP, costing systems.

Resumen:

Este estudio explora las percepciones de los directivos sobre la importancia de los sistemas de costos en la toma de decisiones operativas y estratégicas, así como los factores que influyen en dichas percepciones. Utilizando un alcance relacional y un enfoque cuantitativo, la investigación se basa en una encuesta a directivos responsables de los sistemas de costos en empresas peruanas. Se empleó el análisis factorial para identificar los componentes clave de las percepciones, mientras que las pruebas U de Mann-Whitney y Kruskal-Wallis se utilizaron para evaluar los efectos del uso de ERP y las diferencias entre sectores empresariales. Según los resultados, los sistemas de costos estándar y el costeo por absorción son los más utilizados, principalmente para la elaboración de información financiera, análisis de rentabilidad y presupuestos, sobre todo en la toma de decisiones a corto plazo. La implantación de ERP y el sector empresarial influyen moderadamente en las percepciones de los directivos. Estos resultados proporcionan una base para futuros estudios confirmatorios sobre la relevancia y los determinantes de la adopción de sistemas de costos. El estudio subraya la necesidad de mejorar la formación en herramientas analíticas de los gestores de sistemas de costos para mejorar la toma de decisiones tanto a nivel operativo como estratégico.

JEL: M4.

Palabras clave: contabilidad de costos, control de gestión, ERP, sistemas de costos.

Resumo:

Este estudo explora as percepções dos gestores sobre a importância dos sistemas de custos na tomada de decisões operacionais e estratégicas, bem como os fatores que influenciam essas percepções. Utilizando um escopo relacional e uma abordagem quantitativa, a pesquisa se baseia em un levantamento de dados com gerentes responsáveis por sistemas de custos em empresas peruanas. A análise fatorial foi usada para identificar os principais componentes das percepções, enquanto os testes U de Mann-Whitney e Kruskal-Wallis foram usados para avaliar os efeitos do uso de ERP e as diferenças entre os setores de negócios. De acordo com os resultados, os sistemas de custeio padrão e custeio por absorção são os mais comumente utilizados, principalmente para a elaboração de informações financeiras, análise de rentabilidade e orçamento, especialmente na tomada de decisões de curto prazo. A implantação do ERP e do setor empresarial influenciam moderadamente as percepções dos gestores. Esses resultados fornecem uma base para futuros estudos confirmatórios sobre a relevância e os determinantes da adoção de sistemas de custeio. O estudo ressalta a necessidade de melhorar o treinamento em ferramentas analíticas para gerentes de sistemas de custos para melhorar a tomada de decisões nos níveis operacional e estratégico.

JEL: M4.

Palavras-chave: contabilidade de custos, controle gerencial, ERP, sistemas de custos.

Résumé:

Cette étude explore les perceptions des gestionnaires quant á l’importance des systèmes de coûts dans la prise de décisions opérationnelles et stratégiques ainsi que les facteurs qui influencent ces perceptions. Á la place d’une portée relationnelle et d’une approche quantitative, la recherche se soutient sur une enquête auprès des gestionnaires responsable de systèmes de coûts dans des entreprises péruviennes. L’analyse factorielle a été utilisée pour identifier les éléments clés des perceptions, tandis que les tests U de Mann-Whitney et Kruskal-Wallis ont été utilises pour évaluer les effets d’utilisation de ERP et les différences entre les secteurs d’activité. Selon les résultats, les systèmes de calcul des coûts standard et les coûts d’absorption sont les plus couramment utilisés principalement pour la préparation de l’information financière, l’analyse de la rentabilité et la budgétisation en particulier dans la prise de décision á court terme. La mise en place de l’ERP et le secteur d’activité influencent modérément les perceptions des managers. Ces résultats servent de base á de futures études de confirmation sur la pertinence et les déterminants de l’adoption des systèmes d’établissement des coûts. L’étude souligne la nécessité d’améliorer la formation aux outils analytiques des gestionnaires ce systèmes de coûts afin d’améliorer la prise des décisions aux niveaux opérationnel et stratégique.

JEL: M4.

Mots clés: comptabilité analytique, contrôle de gestion, ERP, systèmes de coûts.

1. Introduction

Historically, costing systems within organizations have primarily been designed to support financial reporting and planning through standard costing and budgeting. However, the growing complexity of business environments has underscored the need for more advanced cost accounting methodologies, such as activity-based costing (ABC), target costing, and strategic indicator analysis, to better align with organizational strategic objectives. The adoption of these methodologies remains limited due to several barriers, including insufficient knowledge among practitioners and resistance from senior management (Guilding et al., 1998; Joshi, 2001; Sulaiman et al., 2004).

Furthermore, management accounting must evolve to provide relevant financial and non-financial information across all organizational functions, supporting both operational and long-term decision-making. This calls for an innovative approach that leverages advanced data analysis systems or repurposes existing ones to not only measure performance but also assess the impact of stakeholder relationships (e.g., with employees and customers) on achieving competitive advantage (Malmi, 2016; Oyewo, 2021; Pedroso & Gomez, 2024).

Despite the potential of strategic costing and control systems like ABC and KPI analysis, research indicates that their widespread implementation remains elusive. This can be attributed to several factors, including a persistent conservative culture within cost accounting, unfamiliarity with the benefits of these systems, resource constraints, implementation complexities, the need for IT infrastructure, and the challenge of aligning organizational behavior (Maelah & Ibrahim, 2007; Yaser-Saleh et al., 2023; Sulaiman et al., 2004).

Innovation in costing and management control systems is shaped by the utilization of IT systems, such as Data Analytics and Enterprise Resource Planning (ERP) tools. These systems have facilitated the generation of valuable financial and non-financial information, leading to more efficient accounting and management control processes. This, in turn, results in enhanced information quality for decision-making, achieving competitive advantages, striving for process excellence, and optimizing resources (Azan & Bollecker, 2011; Balios, 2021; Sánchez-Rodríguez & Spraakman, 2012).

In line with the above, this study aims to contribute to research on the effectiveness of costing systems in operational and strategic decision-making within environments that employ data analytical tools, especially in the context of a Latin American country with an emerging economy like Peru. Existing literature indicates that costing systems are predominantly applied for financial purposes or short-term decision-making, highlighting a deficiency in the development of more advanced systems and tools for long-term strategic decision-making within companies (Gallegos & Rodríguez, 2020; Morillo & Cardozo, 2017).

Therefore, this study aims to explore managers' perceptions of the importance of cost systems in operational and strategic decision-making and examines the factors that influence these perceptions within Peruvian companies.

1.1. Development of Costing Systems

Research on costing systems highlights the traditional reliance of some companies on full costing, order costing, process costing, and standard costing systems, alongside budgeting systems primarily focused on short-term decision-making (Badem et al., 2013; Lukka & Granlund, 1996; Yaser-Saleh et al., 2023). Conversely, other companies have adopted alternative systems such as Activity-Based Costing (ABC), target costing, and cost-volume-profit analysis. These approaches have facilitated cost reduction strategies, enhanced operational efficiency, improved organizational performance, and ultimately provided superior information for strategic decision-making (Almeida & Cunha, 2017; Askarany & Yazdifar, 2012; Wijewardena & De Zoysa, 1999).

Further studies indicate that a key driver in the evolution of cost systems geared towards management control and decision-making has been their influence on the improved utilization of data analytics tools and IT systems. These technologies enable the generation of higher-quality cost and management information (Hadid & Al-Sayed, 2021; Rodniski & De Souza, 2014; Yazdifar et al., 2019; Widjaja & Mauritsius, 2019). Additional research underscores the importance of companies developing such systems to enhance strategic decision-making information. However, a lack of innovation in these systems and resistance from top management have impeded their implementation (Angelakis et al., 2010; Hyvönen, 2005; Joshi, 2001; Sulaiman et al., 2004).

The development and implementation of data analytics systems have facilitated the adoption of more sophisticated costing and management control systems, necessitating a process of change and adaptation. For instance, successful ABC costing implementations have required the introduction of improved information systems, management engagement, alignment, and organizational culture change (Askarany et al., 2010; Fei & Isa, 2010; Hofmann & Bosshard, 2017; Quinn, 2017).

As an alternative to traditional costing systems, ABC costing aims to achieve efficient and effective resource management across activities (Almeida & Cunha, 2017; Escobar-Mamani et al., 2021; Gupta & Galloway, 2003; Quesado & Silva, 2021). Research reveals that companies have been hesitant to adopt this system due to limited resources and the costs associated with implementing improved costing systems that provide decision-making information on the efficiency of organizational processes and activities (Joshi, 2001; Maelah & Ibrahim, 2007; Majid & Sulaiman, 2008; Mazbayeva et al., 2022). It is also important to note that successful ABC costing implementation necessitates consideration of key factors such as management leadership, alignment of the model's strategic objectives with those of the organization, and technological systems that are compatible with other company management systems. On the other hand, this costing system facilitates better-informed resource allocation decisions and product decisions (Daowadueng et al., 2023; Fito & Slof, 2011).

The implementation of data analytics tools and ERP systems has been a decisive factor in enhancing cost accounting and management information systems, leading to reduced operating costs, increased competitiveness, and improved overall company management. ERP systems, in particular, provide more relevant, timely, accurate, and integrated financial and non-financial information for management control and strategic decision-making while optimizing resource utilization and processes (Abbasi et al., 2014; Brands & Holtzblatt, 2015; Gaol et al., 2020; Grabski et al., 2011; Kallunki et al., 2011; Kanellou & Spathis, 2013; Machado & Gomes, 2018). Furthermore, data analytics tools equip managers with more analytical and predictive insights regarding their company's market performance. These tools support decision-making processes, such as activity-based cost analysis, cost-volume-profit analysis, and management control, thereby enabling companies to enhance their business models (Kitsantas et al., 2020; Rikhardssona & Yigitbasioglu, 2018).

1.2. Costing Systems in Latin American Companies

In the context of this research, we consider studies on the use of costing systems in Latin American companies, which have shown significant development in the literature. Research conducted in companies from Brazil, Chile, and Colombia (Borgert et al., 2010; Cárdenas-Mora, 2011; Gallegos & Rodriguez, 2017) has highlighted limitations in the application of costing systems and their role in process management control for products and services. These shortcomings arise from a lack of expertise among those responsible for information, insufficient involvement of general management, and the need for more advanced information system development.

Other studies point to the absence of costing systems that provide improved decision-making information for senior management; instead, they are predominantly used for financial reporting and short-term decision-making (Chacón, 2011; Duque-Roldán et al., 2011; Gallegos & Rodríguez, 2020). However, further research reveals progress made by companies in adopting the Activity-Based Costing system, which facilitates more accurate cost measurement and control, cost-reduction strategies, improved profitability, and the development of information systems linked to enhanced decision-making (Cherres, 2010; López-Mejía et al., 2011; Morillo & Cardozo, 2017; Rodniski & De Souza, 2014; Vicente & Rodríguez, 2024).

Finally, other studies underscore the benefits of utilizing costing systems focused on decision-making, such as process and activity analysis for cost reduction, increased profitability, process efficiency, enhanced product quality and pricing, contribution margin analysis, and consequently, more effective decision-making in both industrial and service companies in Argentina, Chile, Mexico, and Colombia (Gallegos & Rodriguez, 2020; García-Pérez et al., 2006; López & Marín, 2010; Otálora-Beltrán et al., 2016; Sachetto, 2021).

In Peru, literature on company costing systems is less developed, and this research aims to address this gap. Existing studies refer to the implementation of costing systems, such as those by Cherres (2010), Ramos et al. (2020) and Waters et al. (2004), which investigate the implementation of the ABC system, demonstrating its benefits in analyzing more realistic product costs. The study by Lopez-Meza et al. (2021) examines the application of the order costing system for sales control and cost reduction.

Other studies have analyzed managers' perceptions regarding the use of costing systems. Fernández (2018) research identified a relationship between the use of the cost-volume-profit system and financial and management decision-making. Meanwhile, the study by Hernández-Pajares & Vivanco (2023) reveals a lack of orientation towards strategic management control in costing systems, which are primarily applied for financial reporting and profitability analysis.

We pose the following research questions based on the reviewed theoretical background:

2. Research Method

Following a quantitative approach with a relational scope, this study employed a survey administered via Google Forms to examine the application of cost systems and the perceived importance of their use among accountants, controllers, and other professionals responsible for cost accounting in Peruvian companies. A Likert scale with 1 denoting "unimportant" and 5 denoting "very important" was used to gauge perceptions. In March 2023, the survey was carried out.

The sample was selected using a non-probabilistic approach from a pool of 2,000 accounting professionals connected via LinkedIn, specifically those responsible for cost management and cost information systems. While the findings are not intended to be generalized to the entire population of cost system managers in Peruvian companies, they provide a basis for future confirmatory quantitative research. Similar studies have been conducted on accounting professionals using LinkedIn, such as those by Santonastaso & Macchioni (2022).

The criteria for the selection of managers to determine the sample were:

a) Being the general accountant or cost accountant.

b) Being the company’s general controller.

c) Being the Head or Manager of the Management Control Department, or the Administration and Finance Department.

We sent out 450 surveys based on the aforementioned criteria and received 123 responses, which formed the final sample for this study.

Table 1 shows the characteristics of the companies in the final sample of respondents. The companies are presented by business activity and turnover level. With respect to the respondents’ business activity, there are up to six categories: agro-industry, trading, industrial, real estate and construction, mining and oil, and services. Service companies, which were engaged mainly in consulting, educational, and logistics activities, stand out with 29%, followed by industrial companies with 18% and trading companies with 15%.

| Industry | Frequency | % |

| Services | 45 | 36% |

| Industrial | 22 | 18% |

| Trading | 18 | 15% |

| Agro-industrial | 14 | 11% |

| Real Estate/Construction | 14 | 11% |

| Mining and Oil | 10 | 9% |

| Total | 123 | 100% |

The variables considered in the quantitative study are listed in Table 2, which describes the criteria used to measure each variable.

| Variable | Description of measure |

| Gender | Dichotomous variable of the gender of the person responsible for cost accounting |

| Profession | Categorical variable of profession of the person responsible for cost accounting |

| Position | Categorical variable of management position of the person responsible for cost accounting |

| Type of business activity | Categorical variable of sector or activity of business |

| Costing system applied | Categorical variable of the costing system(s) applied by the companies |

| Applied analytics and ERP for costing systems | Categorical variable of the data analytics tool and ERP system applied by the companies |

| Perception of the importance of costing systems | Quantitative variable of the level of importance of the costing systems in the categories set with a 1 to 5 measure on a Likert scale |

Factor analysis was applied to identify key perception components. For the relational analysis, the influence of the variables application of ERP systems and type of business activity on the level of assessment of the costing systems was analyzed with a non-parametric Kruskal-Wallis and Mann-Whitney U test, given that the measure of each perception analyzed does not follow a normal distribution.

3. Results and Discussion

3.1. Profile of companies and respondents

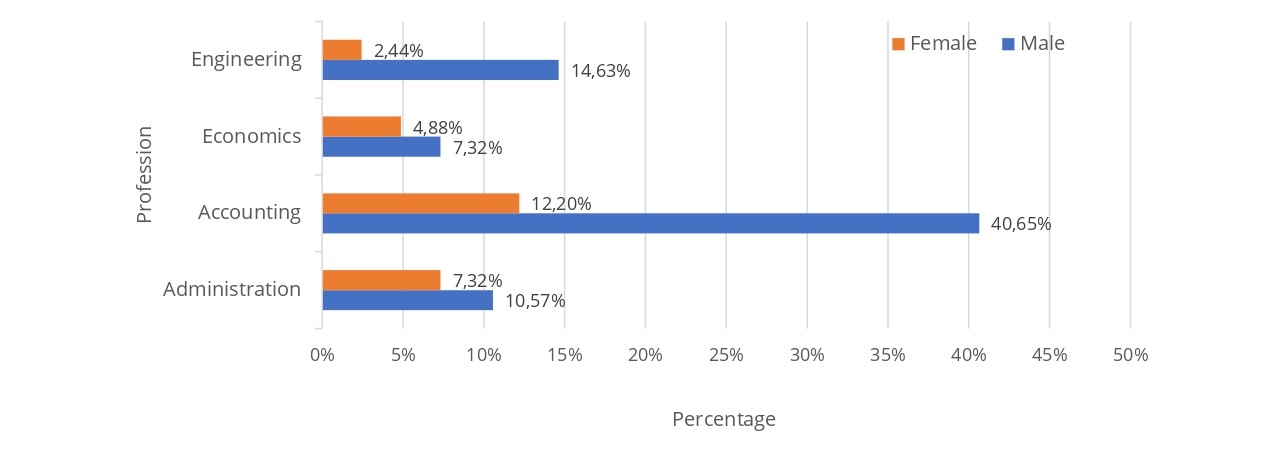

The profile of the respondents corresponds, in its majority, to public accountants with 52.85% and administrators with 17.89%. For all professions, there is a higher number of males, as shown in Figure 1.

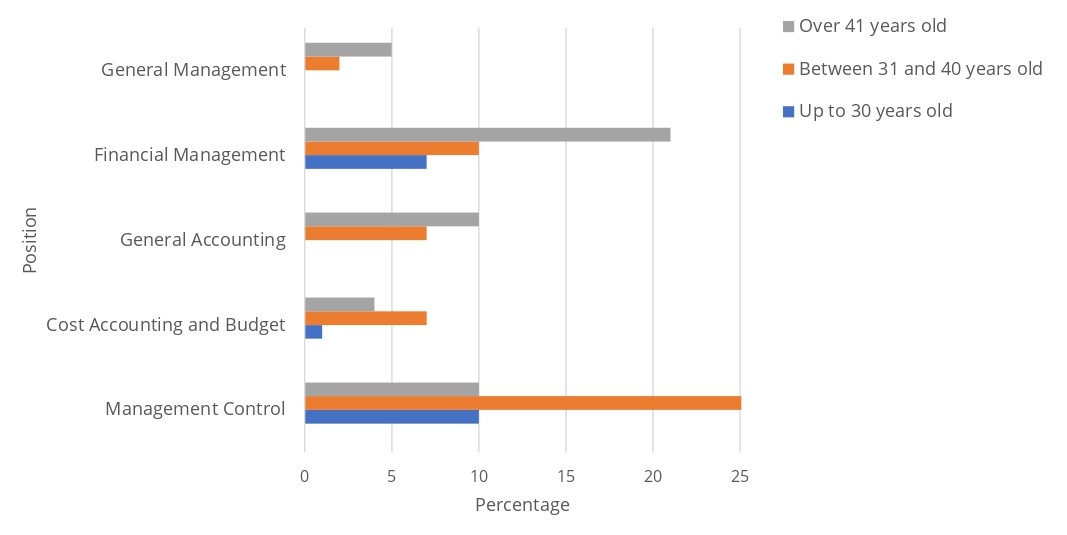

Figure 2 also shows that the majority of the positions held by those responsible for cost accounting were in the management control (39.84%) and financial management (30.89%) departments, while the traditional general accounting and cost accounting positions were present to a lesser extent (13.82% and 9.75%, respectively). Professionals aged between 31 and 40 were in management control, financial management, and cost accounting positions to a greater extent, with 23.58%, 8.13%, and 5.69%, respectively. On the other hand, the majority of the respondents aged over 40 were in the financial management and general accounting departments, with 17.07% and 8.13%, respectively. Only 8.13% of young people under 30 actively participated in the management control department, which serves as their professional development department.

For the first study question, the profile of those responsible for cost accounting corresponds to young males aged over 30 responsible for costing systems. These results are consistent with the studies conducted by Machado (2012) and Machado & Alves (2017). Management control and financial management positions were the most affected, indicating that executives use costing systems to prepare both financial and management control information (Gallegos & Rodriguez, 2017; Quesado & Silva, 2021; Maelah & Ibrahim, 2007).

3.2. Descriptive Analysis

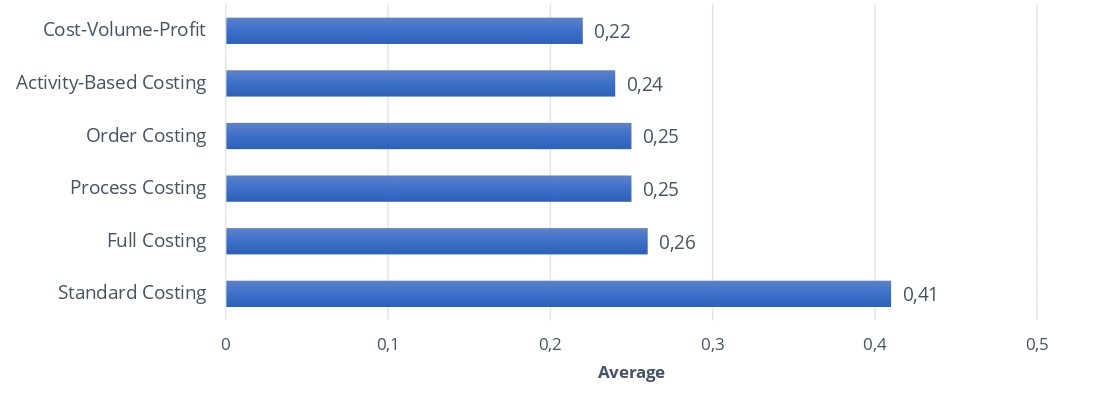

In response to the second study question on costing systems, Figure 3 reveals that the standard costing system, with an average incidence of 0.41, is the most commonly used system for analyzing budget cost variances. The full costing, process costing, and order costing systems, which are considered traditional systems and are used to prepare financial information on inventories, production costs, and selling costs, are among the other systems applied. The ABC and cost-volume-profit costing systems are the least used, with 0.24 and 0.22, respectively; they do not have a significant influence on the companies studied and are applied for activity efficiency analysis and strategic decision-making.

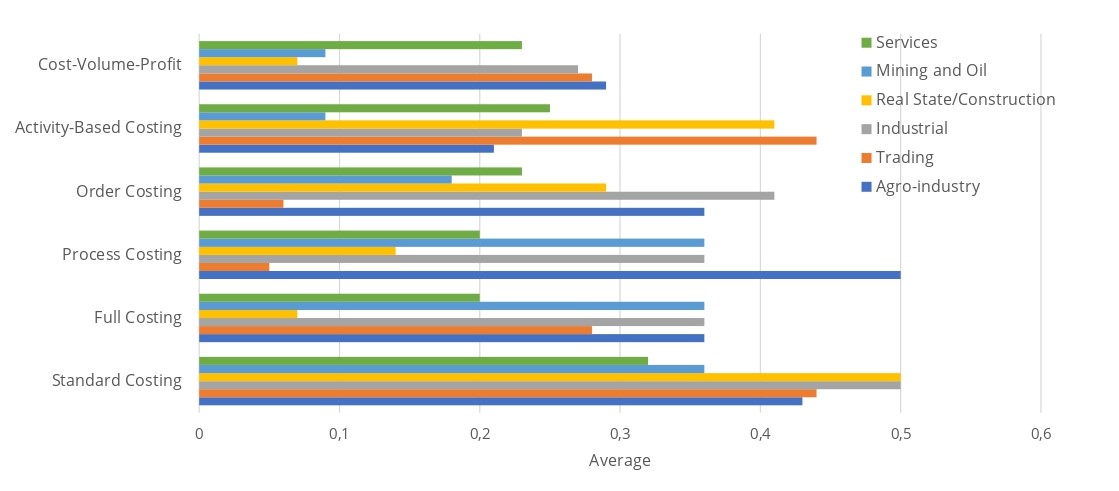

Figure 4 presents the average incidence of applied costing systems across different industries, highlighting how these systems vary based on the nature of the activity and the characteristics of each product or service. The industrial, agro-industrial, and mining sectors show a traditional accounting approach with a greater application of process costing, order costing, standard costing, and full costing systems for the valuation of finished products for financial reporting purposes and the analysis of standard cost variances from budgets. Companies with a greater diversity of products and services complement traditional costing systems with additional methods focused on decision-making. For example, commercial companies predominantly use standard costing, activity-based costing (ABC), full costing, and cost-volume-profit analysis to assess and analyze the profitability of their various products. Real estate, construction, and service companies use standard costing, order costing system, ABC, and cost-volume-profit methods to determine the cost of their services, given the unique nature and variety of the services they provide to their customers and the need to analyze their margins. These results demonstrate the differences in the application of costing systems depending on the nature of the products and services in different sectors, as well as the differences in their use and analysis. (Badem et al., 2013; Gupta & Galloway, 2003; Pietrzak et al., 2020; Yazdifar et al., 2019).

The results show that traditional accounting uses the most commonly applied costing systems, including standard costing, full costing, process costing, and order costing systems. To a lesser extent, the ABC and cost-volume-profit costing systems are also used to analyze and make decisions about the efficiency of activities, product volume, and pricing strategies, often in conjunction with traditional systems (Duque-Roldán et al., 2011; Gupta & Galloway, 2003; Morillo & Cardozo, 2017; Yaser-Saleh et al., 2023). The simultaneous application of various costing systems is present in certain sectors, such as industrial, agro-industrial, and mining companies that use the standard costing, full costing, and process costing systems for inventory measurement and variance analysis. Trading and service companies apply the ABC and cost-volume-profit costing systems to a greater extent (Almeida & Cunha, 2017; Morillo & Cardozo, 2017).

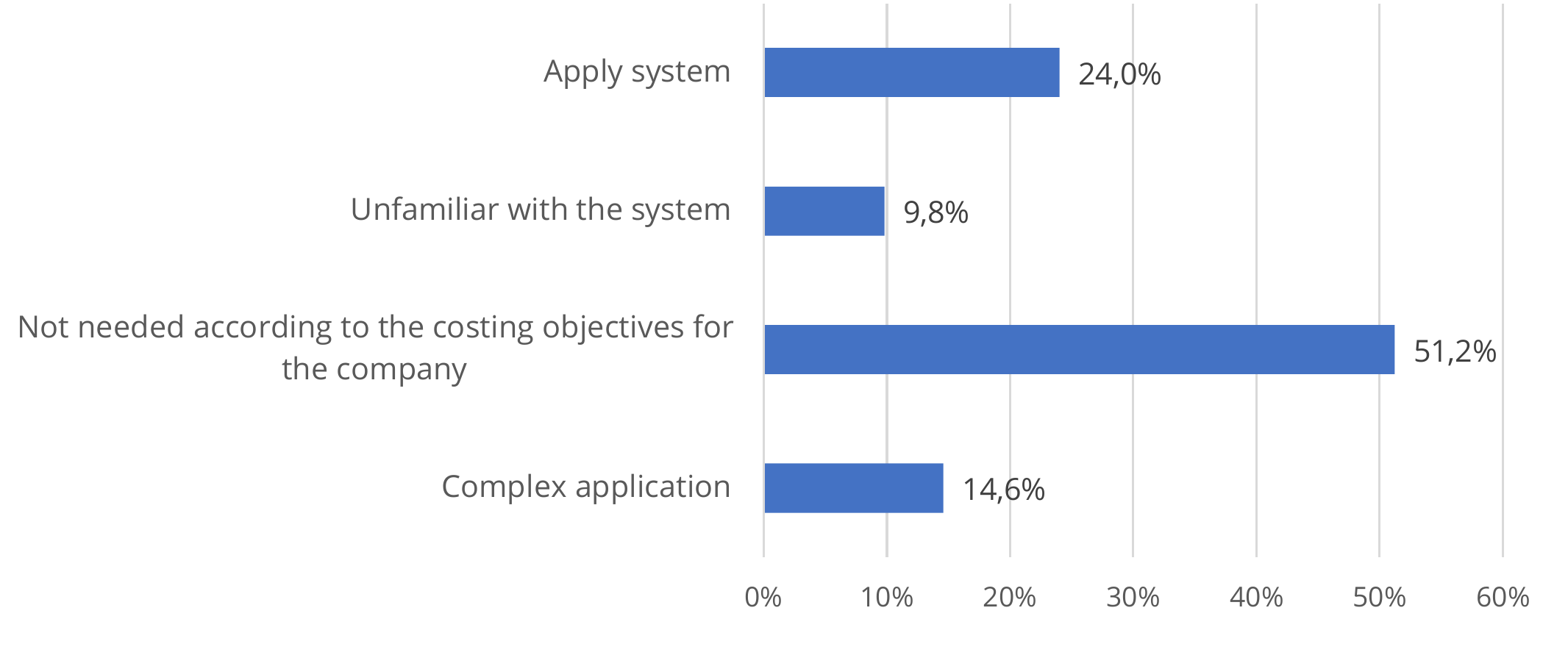

Given that ABC costing is one of the least used costing systems, those in charge of the companies' costing systems cited three main reasons for not considering it: first, they didn't need it to meet the company's costing objectives (51.2%); second, they found its implementation and use to be complex (14.6%); and third, they were unfamiliar with it (9.8%), as illustrated in Figure 5. These results align with studies suggesting that the ABC application is not widely used due to its complex implementation and insufficient information systems, resources, and knowledge (Majid & Sulaiman, 2008; Mazbayeva et al., 2022; Pietrzak et al., 2020; Quinn, 2017). The results also indicate a lack of alignment of the ABC costing systems at all levels of responsibility, which requires leadership from management and a connection to strategic objectives. (Fito & Slof, 2011; Maelah & Ibrahim, 2007).

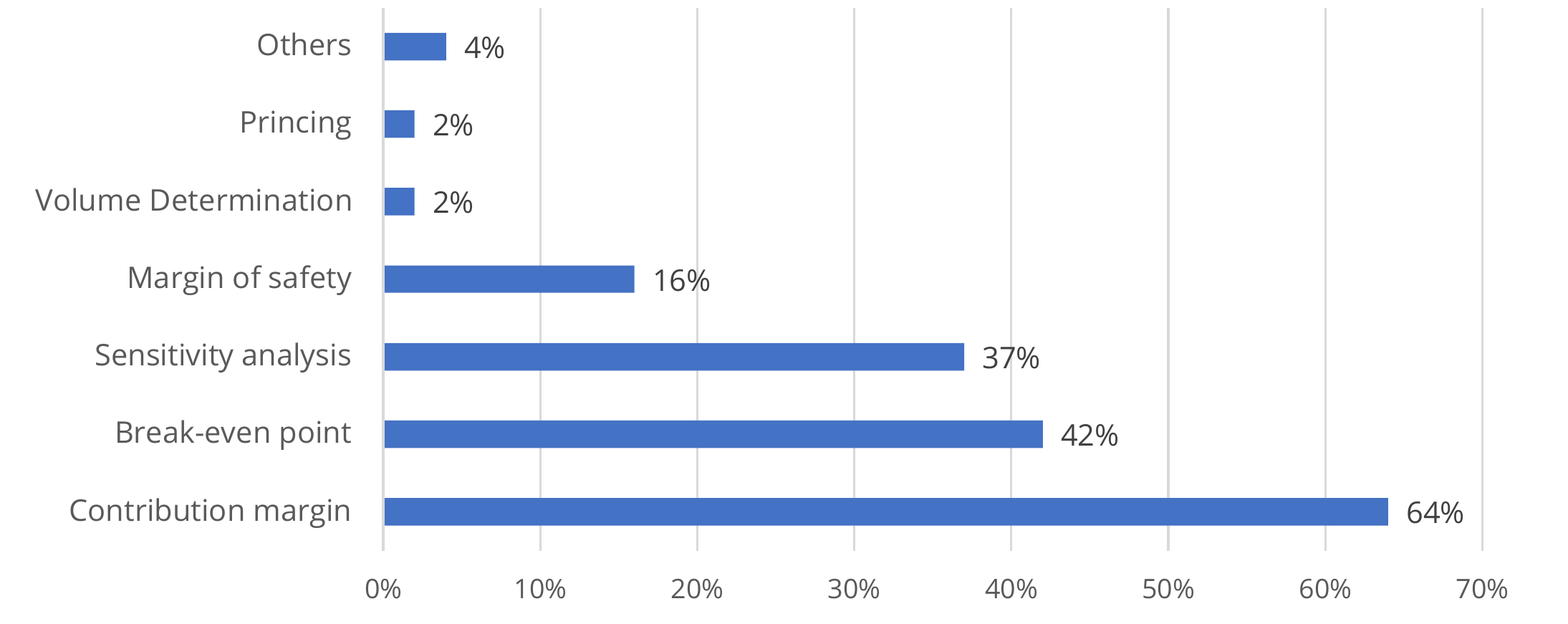

Figure 6 illustrates that the respondents primarily use the cost-volume-profit system to calculate the contribution margin, break-even point, and safety margin of products and services, accounting for 64%, 42%, and 16%, respectively, in short-term decision-making. It is worth noting that 37% of respondents reported using the system for sensitivity analysis, an application that was reported in the studies conducted by Gallegos & Rodríguez (2020), Hyvönen (2005), and López-Mejía et al. (2011).

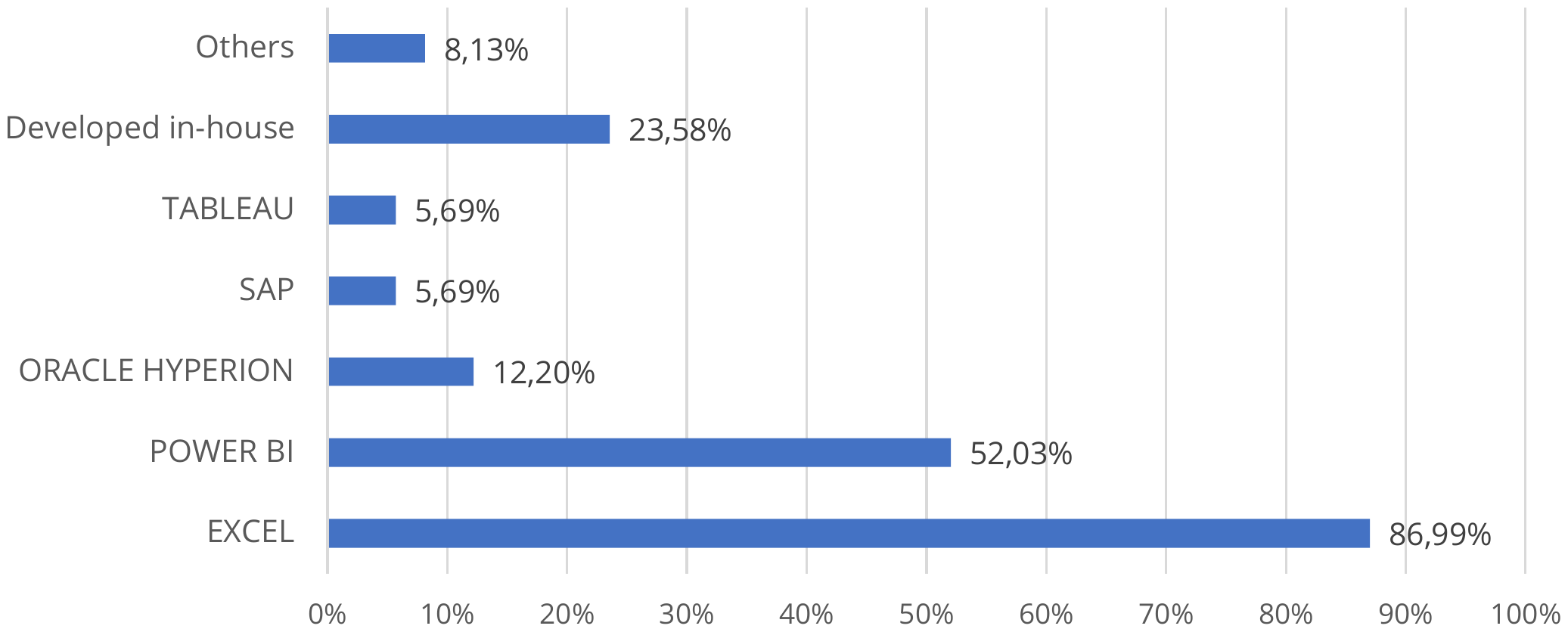

To address the third study question, Figure 7 shows that the most commonly used data analytics tools for costing systems are Excel and Power BI, with 86.99% and 52.03%, respectively. It is worth noting that the companies use the analysis tools developed in-house, with 23.58%. These tools are considered necessary for the development of costing systems in all cases (Brands & Holtzblatt, 2015; Gaol et al., 2020; Widjaja & Mauritsius, 2019).

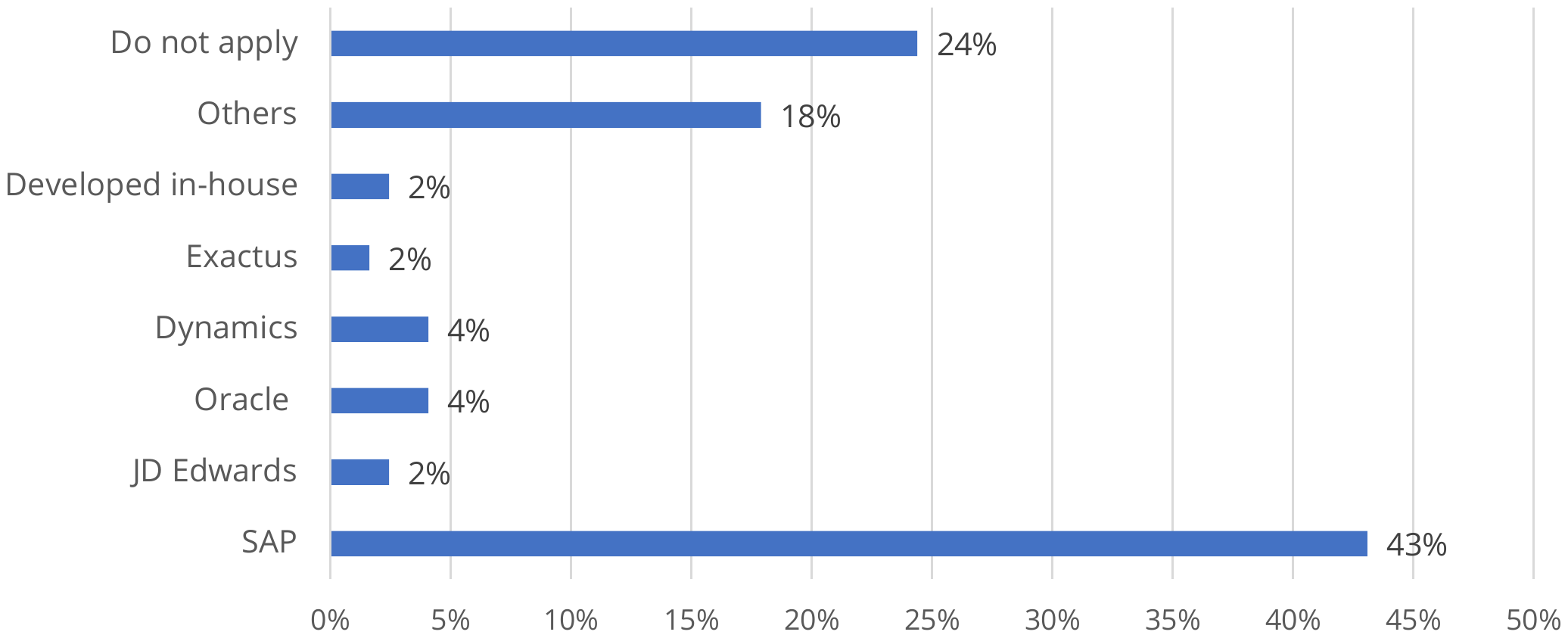

With respect to the use of the ERP system, as seen in Figure 8, 24% of the companies have not applied any ERP system. Out of the companies that utilized an ERP system, 43% primarily utilized SAP, while less than 4% utilized other systems or in-house systems. Companies still face resistance to adopting new ERP systems for accounting purposes. This can be inflexible and need specialized staff, unlike large companies that need to analyze a greater volume of information and to have timely information available for analysis and decision-making, as well as to reorganize functions in the accounting department (Brands & Holtzblatt, 2015; Kanellou & Spathis, 2013; Kitsantas et al., 2020; Machado & Gomez, 2018).

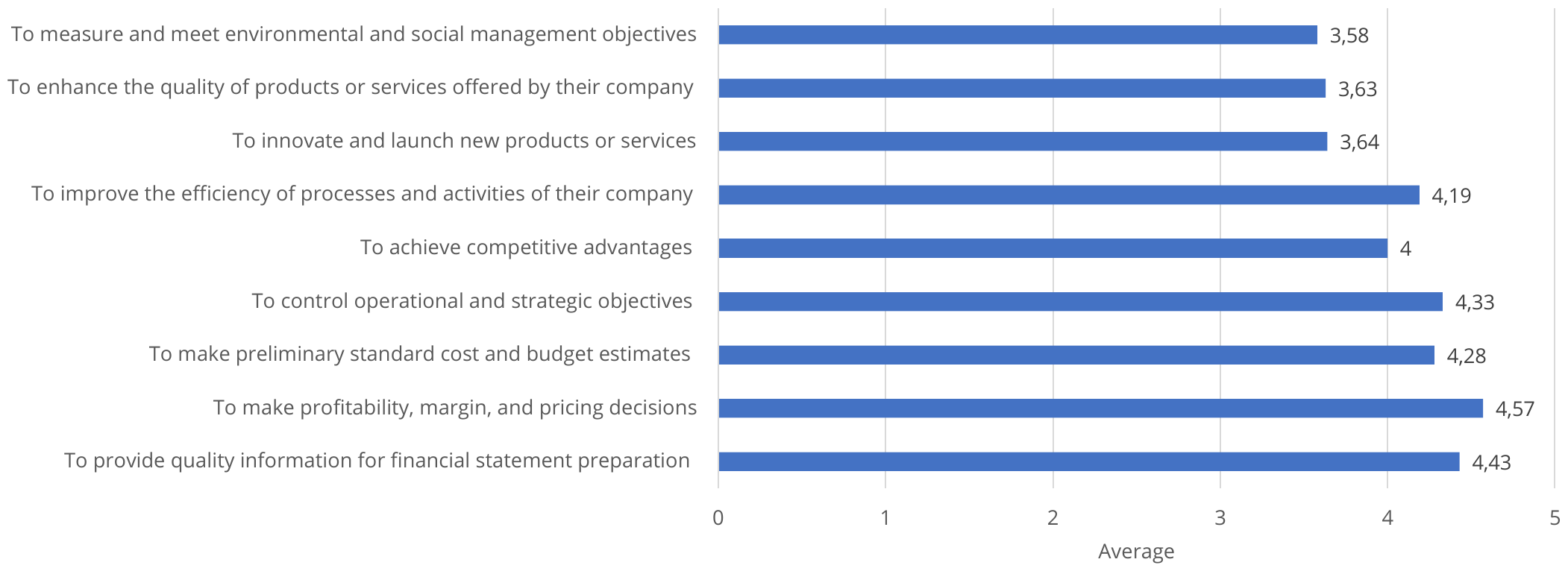

For the fourth study question, Figure 9 shows the importance perceived and valued by those responsible for the costing systems of their use and utility by their average on a 1 to 5 Likert scale. Decisions on profitability and margin of products and services hold the highest importance, with an average score of 4.57, followed by financial information preparation at 4.43 and operational and strategic management control at 4.33. Executives, still in the process of developing and applying topics like product and service quality and innovation, received the lowest scores, averaging 3.64 and 3.63, respectively, while information preparation for environmental and social management received an average of 3.58.

However, other companies give lower scores to improvements in operation and process efficiency, enhancement of product and service quality, and innovation, indicating that companies assess the use of costing systems according to business objectives, which in some cases are short-term operational and in others long-term strategic (Almeida & Cunha, 2017; Askarany et al., 2010; Gallegos & Rodriguez, 2020; Maelah & Ibrahim, 2007; Quinn, 2017; Yazdifar et al., 2019; Wijewardena & De Zoysa, 1999).

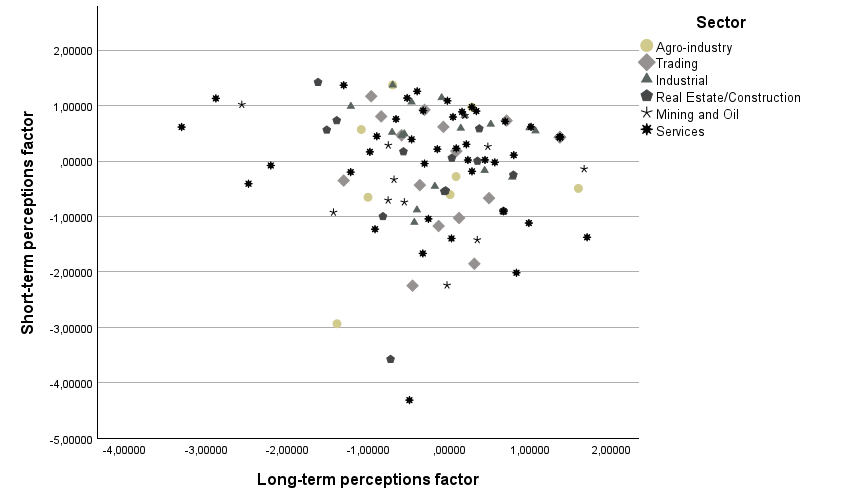

A factor analysis with varimax rotation was performed to reduce the variables of perception of the importance of costing systems. The analysis yielded an acceptable Kaiser-Meyer-Olkin sample adequacy and variable relationship statistic of 0.879, as well as a Bartlett sphericity test with a significance level of 0.01, indicating an adequate correlation of the variables. The representative components with the highest factor loadings of the perceptions were two: the first component, which was called "short-term perception", focused on the importance of costing systems in short-term decisions related to the analysis of financial information, profitability analysis and pricing, standard cost analysis, budget deviation and operations control. The second component, called “long-term perception,” included the role of costing systems in long-term decisions such as obtaining competitive advantages, improving the efficiency of processes and activities, promoting innovation and quality in products and services, and managing environmental and social objectives. Table 3 presents the component matrix and factor loadings of perception questions.

| Importance of costing systems questions | Components and factor loadings | |

| Short-Term Perception | Long-Term Perception | |

| To provide quality financial information | 0.866 | 0.143 |

| To make profitability, margin, and pricing decisions | 0.866 | 0.180 |

| To make preliminary standard cost and budget estimates | 0.710 | 0.346 |

| To control operational objectives | 0.691 | 0.517 |

| To achieve competitive advantages | 0.560 | 0.613 |

| To improve the efficiency of processes and activities | 0.569 | 0.558 |

| To innovate and launch new products or services | 0.297 | 0.819 |

| To enhance the quality of products or services | 0.225 | 0.835 |

| To measure and meet environmental and social management objectives | 0.156 | 0.818 |

Figure 10 shows the companies studied by component, classified by type of business activity. The majority of those responsible for costing systems evaluate both short- and long-term objectives. According to the business activity, there was no predominance of either short- or long-term assessments. Companies, regardless of sector, assess the short- and long-term objectives according to the needs of the cost control systems for operational and strategic purposes (Askarany et al., 2010; Gallegos & Rodríguez, 2020;Yaser-Saleh et al., 2023; Yazdifar et al., 2019).

3.3. Relational Analysis

To answer the fifth question of the study, we used the Kruskal-Wallis test to perform an impact analysis of the categorical variables of ERP application and business sector on each assessment of the importance of using cost systems in the surveys.

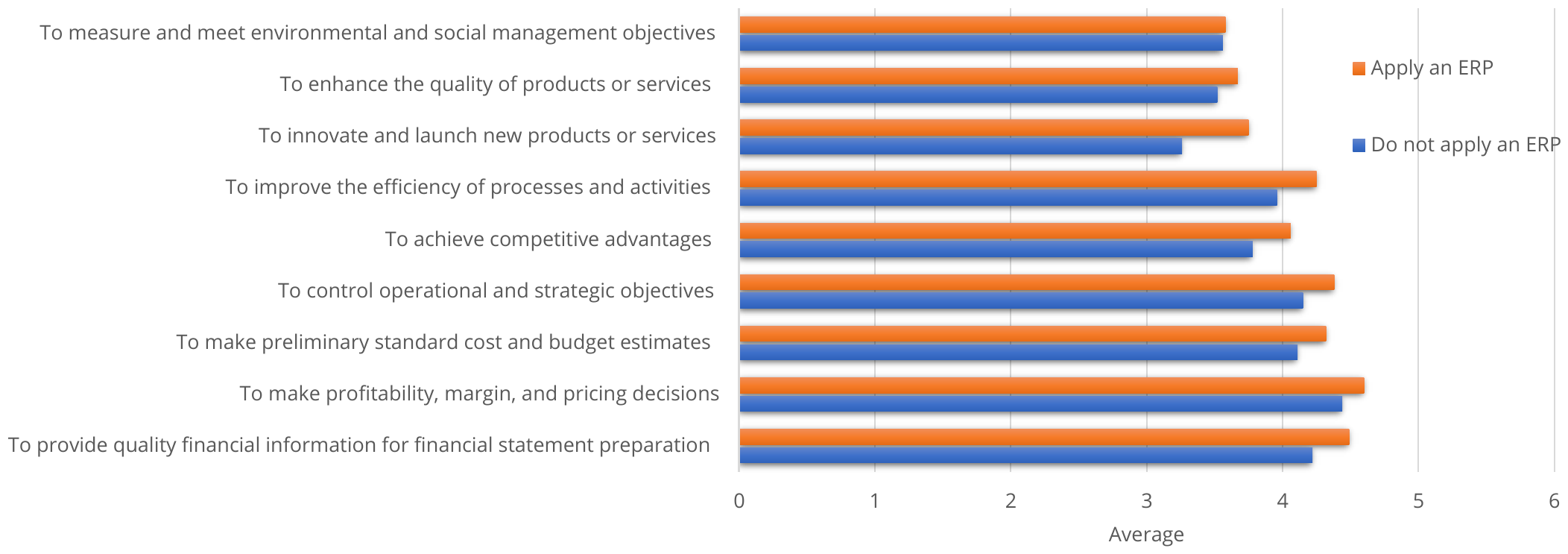

Figure 11 presents the categorized perceptions of companies that do and do not apply ERP systems. Table 4 shows that companies that used ERP systems had a higher assessment of the perceptions of the importance of cost systems, but there was only a moderate impact effect of ERP application (sig. < 10%) on the importance of preparing financial information and innovating new products and services.

These perceptions with a higher incidence of ERP application refer to providing better and timely financial and non-financial information for analysis, control, and strategic decision-making, as well as for the innovation of processes, products, and services (Abbasi et al., 2016; Balios, 2021; Hadid & Al-Sayed, 2021; Kallunki et al., 2011; Kanellou & Spathis, 2013; Kitsantas et al., 2020).

| To provide quality financial information | To make profitability, margin, and pricing decisions | To make preliminary standard cost and budget estimates | To control operational and strategic objectives | To achieve competitive advantages | To improve the efficiency of processes and activities | To innovate and launch new products or services | To enhance the quality of products or services | To measure and meet environmental and social management objectives | |

| Mann-Whitney U | 1042 | 1130 | 1169 | 1145 | 1084 | 1050 | 994 | 1177 | 1264 |

| Z | -1.759 | -1.218 | -0.85 | -1.014 | -1.368 | -1.636 | -1.915 | -0.760 | -0.206 |

| Asymp. sig. | 0.079* | 0.223 | 0.394 | 0.310 | 0.171 | 0.102 | 0.055* | 0.447 | 0.837 |

| * p<0.10 | |||||||||

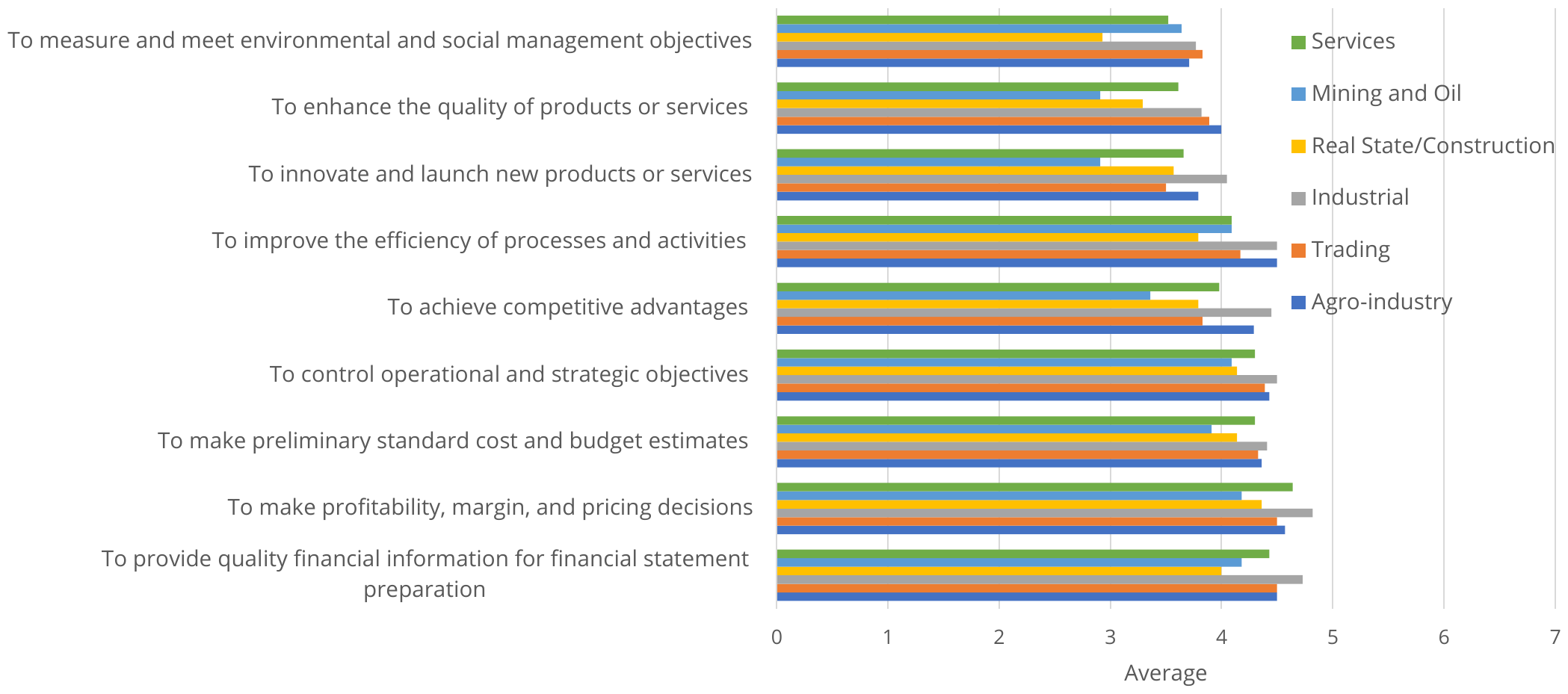

Figure 12 shows that the level of assessment of the costing systems differs for each business sector. Table 5 reveals a significant impact of sector, with a probability (sig.) of less than 10% and 5%, respectively, on perception scores on preparing financial information and improving the quality of products and services, which are significantly higher in the industrial, agro-industrial, and commercial sectors, and on decisions on profitability, pricing, and achieving competitive advantage, which are significantly higher in firms in the industrial, agro-industrial, and service sectors. Therefore, the type of industry and the nature of products and services offered are considered to determine the use of costing systems by firms (Cardenas-Mora, 2011; Grabski et al., 2011; Pietrzak et al., 2020; Yazdifar et al., 2019).

| To provide quality financial information | To make profitability, margin, and pricing decisions | To make preliminary standard cost and budget estimates | To control operational and strategic objectives | To achieve competitive advantages | To improve the efficiency of processes and activities | To innovate and launch new products or services | To enhance the quality of products or services | To measure and meet environmental and social management objectives | |

| H de Kruskal-Wallis | 12.229 | 9.608 | 4.732 | 3.455 | 14.911 | 7.299 | 7.969 | 10.948 | 7.792 |

| gl | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 | 5 |

| Sig. | 0.032** | 0.087* | 0.449 | 0.630 | 0.011** | 0.199 | 0.158 | 0.052* | 0.168 |

| * p<0.10 ** p<0.05 | |||||||||

4. Conclusions

This study explored managers' perceptions of the importance of cost systems in operational and strategic decision-making and analyzed the factors influencing these perceptions. The findings highlight significant developments in the use of cost systems and the application of data analytics tools for their enhancement.

Those responsible for these systems in the Peruvian companies surveyed use them mainly for financial reporting, profitability analysis, identifying cost variances, improving operational efficiency and pricing, and focusing mainly on short-term control, especially in agro-industrial, manufacturing, and mining companies based on finished production. However, long-term objectives on the usefulness of cost systems for improving competitiveness through quality and innovation of products, services, and processes, and the management of environmental and social objectives, were not significantly emphasized.

Other sectors, such as commercial, real estate, and services, tend to complement traditional cost systems with activity-based costing and cost-volume-profit analysis due to the diverse nature of their operations and products. The adoption of specific cost systems is influenced by the sector and the characteristics of the products and services provided, shaping managerial perceptions of their importance for both operational and strategic decision-making.

All the companies surveyed utilize cost system data analysis tools, enabling more advanced and accurate cost allocation models while minimizing manual errors. Notably, a quarter of the surveyed companies have not implemented ERP systems for cost management, primarily due to resource constraints and limited implementation expertise. In contrast, companies that have adopted ERP systems benefit from greater process integration and optimization, improved cost allocation to products, services, and activities, and enhanced managerial decision-making. Additionally, ERP implementation influences managers' perceptions of the importance of cost systems, particularly in financial reporting and product design and innovation.

The study is primarily limited by the sample size of cost system managers surveyed, which restricts the generalizability of the findings to all Peruvian companies using cost systems. Furthermore, organizational structure, degree of innovation and technology adoption, company size, resource availability, and other possible influencing factors were not taken into account.

Despite these limitations, the study contributes to the literature by providing insights into managers' assessments of cost system importance in selected Peruvian companies. It also identifies areas for improvement in cost systems to better support long-term strategic decision-making. Future research could expand the sample to include a broader range of managers and companies of different sizes and sectors, both in Peru and other Latin American countries. Such studies could further explore the limitations and advantages of cost system adoption, the role of analytical tools in decision-making, and the knowledge and resources needed to optimize cost management procedures.

Finally, future studies should look at how new technologies, like big data and artificial intelligence, have affected the development of cost systems and their function in strategic decision-making. Enhancing competitive advantages and market differentiation requires these developments.

References

Abbasi, S., Zamani, M. & Valmohammadi, C. (2014), The effects of ERP systems implementation on management accounting in Iranian organizations. Education, Business and Society: Contemporary Middle Eastern Issues, 7 (4), 245-256. https://doi.org/10.1108/EBS-03-2014-0020

Almeida, A., & Cunha, J. (2017). The implementation of an Activity-Based Costing (ABC) system in a manufacturing company. Procedia manufacturing, 13, 932-939. https://doi.org/10.1016/j.promfg.2017.09.162

Angelakis, G., Theriou, N., & Floropoulos, I. (2010). Adoption and benefits of management accounting practices: Evidence from Greece and Finland. Advances in Accounting, 26(1), 87-96. https://doi.org/10.1016/j.adiac.2010.02.003

Askarany, D., Yazdifar, H., & Askary, S. (2010). Supply chain management, activity-based costing and organisational factors. International Journal of Production Economics, 127(2), 238-248. https://doi.org/10.1016/j.ijpe.2009.08.004

Askarany, D., & Yazdifar, H. (2012). An investigation into the mixed reported adoption rates for ABC: Evidence from Australia, New Zealand and the UK. International Journal of Production Economics, 135(1), 430-439.

Azan, W. & Bollecker, M. (2011). Management control competencies and ERP: an empirical analysis in France. Journal of Modelling in Management, 6 (2), 178-199. https://doi.org/10.1108/17465661111149575

Badem, A. C., Ergin, E., & Drury, C. (2013). Is standard costing still used? Evidence from Turkish automotive industry. International Business Research, 6(7), 79-90. https://doi.org/10.5539/ibr.v6n7p79

Balios, D. (2021). The impact of Big Data on accounting and auditing. International Journal of Corporate Finance and Accounting, 8(1), 1-14. https://doi.org/10.4018/IJCFA.2021010101

Borgert, A., Alves, R. V., & Schultz, C. A. (2010). Processo de implementação de um sistema de gestão de custos em hospital público: um estudo das variáveis intervenientes. Revista Contemporânea de Contabilidade, 7(14), 97-119.

Brands, K., & Holtzblatt, M. (2015). Business Analytics: Transforming the Role of Management Accountants. Management Accounting Quarterly, 16(3).

Cárdenas-Mora, S. M. (2011). Una aproximación al uso de herramientas de gerencia estratégica de costos en instituciones privadas de educación superior. Cuadernos de Contabilidad, 12(31), 547-569. https://revistas.javeriana.edu.co/index.php/cuacont/article/view/3104

Chacón, G. B. (2011). La contabilidad de costos en el sistema de información contable de las PyME del estado Mérida. Actualidad Contable Faces, 14(22), 21-44.

Cherres, S. L. (2010). Un caso de aplicación del sistema ABC en una empresa peruana: Frenosa. Contabilidad y negocios, 5(10), 29-43. https://doi.org/10.18800/contabilidad.201002.006

Daowadueng, P., Hoozée, S., Jorissen, A., & Maussen, S. (2023). Do costing system design choices mediate the link between strategic orientation and cost information usage for decision making and control?. Management Accounting Research, 61, 100854. https://doi.org/10.1016/j.mar.2023.100854

Duque-Roldán, M. I., Agudelo, J. A. O., & Hernández, D. M. A. (2011). Costos estándar y su aplicación en el sector manufacturera colombiano. Cuadernos de Contabilidad, 12(31), 521-545. https://revistas.javeriana.edu.co/index.php/cuacont/article/view/3102

Escobar-Mamani, F., Argota-Pérez, G., Ayaviri Nina, V. D., Aguilar-Pinto, S. L., Quispe Fernandez, G. M., & Arellano Cepeda, O. E. (2021). Costeo basado en actividades (ABC) en las PYMES e iniciativas innovadoras:¿ opción posible o caduca?. Revista de Investigaciones Altoandinas, 23(3), 171-180. https://doi.org/10.18271/ria.2021.321

Fei, Z. Y., & Isa, C. R. (2010). Behavioral and organizational variables affecting the success of ABC success in China. African Journal of Business Management, 4(11), 2302. https://doi.org/10.5897/AJBM.9000113

Fernández, V. H. (2018). Punto de equilibrio y su incidencia en las decisiones financieras de empresas editoras en Lima. Quipukamayoc, 26(52), 95-101. https://doi.org/10.15381/quipu.v26i52.15507

Fito, M. A., & Slof, J. (2011). From design of activity-based costing systems to their regular use. Intangible Capital, 7(2), 474-506. https://doi.org/10.3926/ic.268

Gallegos, C., & Rodríguez, E. R. (2020). Gestión de costos en el sector de áridos a través del método de costeo basado en actividades. Cuadernos de Contabilidad, 21, 17. https://doi.org/10.11144/Javeriana.cc21.gcsa

Gallegos, C., & Rodríguez, E. R. (2017). Métodos de costos utilizados por instituciones hospitalarias en Chile: estudio de caso. CAPIC REVIEW, 15(1), 75-84. https://doi.org/10.35928/cr.vol15.2017.13

García-Pérez D., Marín, S., & Martínez, F. J. (2006). La contabilidad de costos y rentabilidad en la Pyme. Contaduría y Administración, (218), 39-59. http://dx.doi.org/10.22201/fca.24488410e.2006.578

Gaol, F. L., Abdillah, L., & Matsuo, T. (2020). Adoption of business intelligence to support cost accounting based financial systems—case study of XYZ company. Open Engineering, 11(1), 14-28. https://doi.org/10.1515/eng-2021-0002

Guilding, C., Lamminmaki, D., & Drury, C. (1998). Budgeting and standard costing practices in New Zealand and the United Kingdom. The International Journal of Accounting, 33(5), 569-588. https://doi.org/10.1016/S0020-7063(98)90013-9

Gupta, M., & Galloway, K. (2003). Activity-based costing/management and its implications for operations management. Technovation, 23(2), 131-138. https://doi.org/10.1016/S0166-4972(01)00093-1

Grabski, S. V., Leech, S. A., & Schmidt, P. J. (2011). A review of ERP research: A future agenda for accounting information systems. Journal of information systems, 25(1), 37-78. https://doi.org/10.2308/jis.2011.25.1.37

Hadid, W., & Al-Sayed, M. (2021). Management accountants and strategic management accounting: The role of organizational culture and information systems. Management Accounting Research, 50, 100725. https://doi.org/10.1016/j.mar.2020.100725

Hernández-Pajares, J., & Vivanco, G. (2022). Percepciones de los controllers sobre los sistemas de control de gestión de empresas peruanas. CAPIC REVIEW, 20, 1-15. https://doi.org/10.35928/cr.vol20.2022.169

Hofmann, E., & Bosshard, J. (2017). Supply chain management and activity-based costing: Current status and directions for the future. International Journal of Physical Distribution & Logistics Management, 47(8), 712-735. https://doi.org/10.1108/IJPDLM-04-2017-0158

Hyvönen, J. (2005). Adoption and Benefits of Management Accounting Systems: Evidence from Finland and Australia. Advances in International Accounting, 18, 97–120. https://doi.org/10.1016/S0897-3660(05)18005-2

Joshi, P. L. (2001). The international diffusion of new management accounting practices: the case of India. Journal of International Accounting, Auditing and Taxation, 10(1), 85-109.https://doi.org/10.1016/S1061-9518(01)00037-4

Kallunki, J. P., Laitinen, E. K., & Silvola, H. (2011). Impact of enterprise resource planning systems on management control systems and firm performance. International Journal of Accounting Information Systems, 12(1), 20-39. https://doi.org/10.1016/j.accinf.2010.02.001

Kanellou, A., & Spathis, C. (2013). Accounting benefits and satisfaction in an ERP environment. International Journal of Accounting Information Systems, 14(3), 209–234. https://doi.org/10.1016/j.accinf.2012.12.002

Kitsantas, T., Vazakidis, A., & Stefanou, C. (2020). Integrating Activity Based Costing (ABC) with Enterprise Resource Planning (ERP) for Effective Management: A Literature Review. Technium: Romanian Journal of Applied Sciences and Technology, 2(7), 160–178.https://doi.org/10.47577/technium.v2i7.1882

López-Meza, A., Palomino, S. S., & Vílchez, K. A. (2021). Sistema de costos por órdenes específicas y la comercialización de la fibra de alpaca en la comunidad campesina de Pampachacra, periodo 2019. Balance´ s, 8(12), 16-20. https://revistas.unas.edu.pe/index.php/Balances/article/view/227

López, M. R., & Marín, S. (2010). Los Sistemas de Contabilidad de Costos en la PyME mexicana. Investigación y ciencia, 18(47), 49-56.

López-Mejía, M. R., Gómez-Martínez, A., & Marín-Hernández, S. (2011). Sistema de costos ABC en la mediana empresa industrial mexicana. Cuadernos de contabilidad, 12(30), 23-43. https://revistas.javeriana.edu.co/index.php/cuacont/article/view/3109

Lukka, K., & Granlund, M. (1996). Cost accounting in Finland: current practice and trends of development. European Accounting Review, 5(1), 1-28. https://doi.org/10.1080/09638189600000001

Machado, M. J. (2012). Activity Based Costing Knowledge: Empirical study on small and medium size enterprises. Revista contemporânea de contabilidade, 9 (18), 167-186. http://dx.doi.org/10.5007/2175-8069.2012v9n18p167

Machado, M. J., & Alves, P. C. (2017). Quality in management accounting: approach by activities in large companies. International Journal of Productivity and Quality Management, 21(3), 392-409. https://doi.org/10.1504/IJPQM.2017.084463

Machado, M. J., & Gomes, J. (2018). Accounting and the ERP Systems. International Journal of Knowledge-Based Organizations, 8(2), 32–41. https://doi.org/10.4018/IJKBO.2018040103

Maelah, R., & Ibrahim, D. N. (2007). Factors influencing activity based costing (ABC) adoption in manufacturing industry. Investment Management and Financial Innovations, (4, Iss. 2), 113-124.

Majid, J. A., & Sulaiman, M., (2008). Implementation of activity-based costing in Malaysia: A case study of two companies. Asian Review of Accounting.16(1), 39-55. https://doi.org/10.1108/13217340810872463

Malmi, T. (2016). Managerialist studies in management accounting: 1990–2014. Management Accounting Research, 31, 31-44. https://doi.org/10.1016/j.mar.2016.02.002

Mazbayeva, K., Barysheva, S., & Saparbayeva, S. S. (2022). The influence of the importance of cost information, product diversity and accountants’ participation on the activity-based costing adoption. Journal of Accounting & Organizational Change, 18(2), 346-366. https://doi.org/10.1108/JAOC-01-2021-0013

Morillo, M. C., & Cardozo, C. D. (2017). Sistema de costos basado en actividades en hoteles cuatro estrellas del estado Mérida, Venezuela. Innovar, 27(64), 91-113. https://doi.org/10.15446/innovar.v27n64.62371

Otálora-Beltrán, J. E., Escobar-Castillo, A. E., & Borda-Viloria, J. C. (2016). Sistemas de gestión de costos en las cooperativas de ahorro y crédito de Barranquilla. Cuadernos de Contabilidad, 17(44), 349-375. https://doi.org/10.11144/Javeriana.cc17-44.sgcc

Oyewo, B. (2021). Do innovation attributes really drive the diffusion of management accounting innovations? Examination of factors determining usage intensity of strategic management accounting. Journal of Applied Accounting Research, 22(3), 507-538. https://doi.org/10.1108/JAAR-07-2020-0142

Pedroso, E., & Gomes, C. F. (2024). The current role of management accounting: paradigm shift and future challenges. Journal of Accounting & Organizational Change, 20(2), 307-333. https://doi.org/10.1108/JAOC-05-2022-0086

Pietrzak, Ž., Wnuk-Pel, T., & Christauskas, Č. (2020). Problems with activity-based costing implementation in Polish and Lithuanian companies. Inžinerinė ekonomika, 26-38. https://doi.org/10.5755/j01.ee.31.1.24339

Quesado, P., & Silva, R. (2021). Activity-based costing (ABC) and its implication for open innovation. Journal of Open Innovation: Technology, Market, and Complexity, 7(1), 41. https://doi. org/10.3390/joitmc7010041

Quinn, M., Elafi, O. & Mulgrew, M. (2017). Reasons for not changing to activity-based costing: a survey of Irish firms, PSU Research Review, 1(1), 63-70. https://doi.org/10.1108/PRR-12-2016-0017

Ramos, E., Huacchillo, L., & Portocarrero, Y. (2020). El sistema de costos ABC como estrategia para la toma de decisiones empresarial. Revista Universidad y Sociedad, 12(2), 178-183.

Rikhardsson, P., & Yigitbasioglu, O. (2018). Business intelligence & analytics in management accounting research: Status and future focus. International Journal of Accounting Information Systems, 29, 37-58.

Rodniski, C. M., & De Souza, M. A. (2014). Structure of system costs and attributes of information: a study with Brazilian companies. Revista Universo Contabil, 10(4), 45. https://ojsrevista.furb.br/ojs/index.php/universocontabil/article/view/4136

Sachetto, F. (2021). El análisis marginal en la industria automotriz. Costos y Gestión, (100), 173-184. https://iapuco.org.ar/ojs/index.php/costos-y-gestion/article/view/182

Sánchez‐Rodríguez, C., & Spraakman, G. (2012). ERP systems and management accounting: A multiple case study. Qualitative Research in Accounting & Management, 9(4), 398-414. https://doi.org/10.1108/11766091211282689

Santonastaso, R., & Macchioni, R. (2022). An Exploratory Study of the Digital Competences of Italian Accountants: Some Preliminary Results. International Journal of Business and Management, 17(2), 13-27. https://doi.org/10.5539/ijbm.v17n2p13

Sulaiman, M. B., Nazli Nik Ahmad, N., & Alwi, N. (2004). Management accounting practices in selected Asian countries: a review of the literature. Managerial Auditing Journal, 19(4), 493-508. https://doi.org/10.1108/02686900410530501

Vicente, N., & Rodríguez, E. I. (2024). Costeo Basado en Actividades: Impacto en la Rentabilidad en una clínica odontológica. Costos y Gestión, (107). https://doi.org/10.56563/costosygestion.107.e3

Widjaja, S., & Mauritsius, T. (2019). The development of performance dashboard visualization with power BI as platform. International Journal of Mechanical Engineering and Technology, 10(5), 235-249. https://iaeme.com/Home/article_id/IJMET_10_05_024

Waters, H., Abdallah, H., & Santillán, D. (2001). Application of activity‐based costing (ABC) for a Peruvian NGO healthcare provider. The International Journal of Health Planning and Management, 16(1), 3-18. https://doi.org/10.1002/hpm.606

Wijewardena, H., & De Zoysa, A. (1999). A comparative analysis of management accounting practices in Australia and Japan: an empirical investigation. The International Journal of Accounting, 34(1), 49-70. https://doi.org/10.1016/S0020-7063(99)80003-X

Yaser-Saleh, Q., Barakat AL-Nimer, M., & Abbadi, S. S. (2023). The quality of cost accounting systems in manufacturing firms: A literature review. Cogent Business & Management, 10(1), 2209980. https://doi.org/10.1080/23311975.2023.2209980

Yazdifar, H., Askarany, D., Wickramasinghe, D., Nasseri, A., & Alam, A. (2019). The diffusion of management accounting innovations in dependent (subsidiary) organizations and MNCs. The International Journal of Accounting, 54(01), 1950004. https://doi.org/10.1142/S1094406019500045

Additional information

ARK CAICYT: http://id.caicyt.gov.ar/ark:/s25458329/woy1azwrv