2.1 Indicators of corporate profitability

The field of financial indicators is within the framework of the theory of the firm, which tries to explain and predict business behavior. Depending on the emphasis on each explanatory factor, several derived theories emerged: economic, behavioral, contractual and others, each group supported by its empirical evidence. All these theories are taken into account to determine the explanatory variables frequently used in business performance research(3)(4).

Within the firm theories, and particularly the traditional neoclassical economic theory, profitability is one of the most analyzed elements. The approach and variables considered as determinants will depend on the type of theory on which they are based. For example, economic theory will focus on profitability represented by indicators such as ROA or ROE(1)(3)(5)(6)(7)(8).

In other cases, in parallel with profitability, the level of indebtedness is also analyzed. The company’s behavior towards the form of financing with third-party funds is explained by the agency's theory, in which tensions between managers and owners can generate cost overruns due to debts, impairments in the reinvestment of profits, loss of business opportunities and other problems that attack profitability in the medium and long term(9).

When profitability is focused on innovation, potential of human resources or capital, theories called Resourced Based View are referenced. This purely qualitative approach(10)(11) affirms that competitive advantages and better performance result from the combination of resources and capabilities available to the company, for example, quantity and quality of its employees(6)(12).

Instead, economic theories focus on the monetary values of certain equity items such as assets or debts, or in other cases, on the monetary values of sales revenue or cost structures.

In terms of indicators, to work with data from the annual financial statements, the Dupont system is widely used, where the ratios Return On Assets (ROA) and Return On Equity (ROE) are calculated for each company. To standardize the results and make them comparable, it is common to previously use EBITDA (Earnings Before Interest Taxes Depreciation and Amortization) as a measure of the result in monetary units, instead of the final result(13)(14).

The use of EBITDA aims to work with the operating result of the company, without considering its tax situation —clearly dependent on the country of residence— nor the form of financing, often also dependent on the country and the vertical integration of the meso-economic chains in which the company is located. On several occasions, companies are part of economic groups that cover the primary, secondary and financial sectors. This study finds its core problem precisely on this point or tension. The literature presents an ambiguous treatment regarding this dichotomy and it is difficult to find backgrounds that pose the problem as a dilemma.

Methodologically, profitability is the most widely used indicator to measure business performance. Moreover, studies based on accounting results or cost structure are scarce. Limitations in the use of accounting bases, usually highlighted by the literature, are: the impact of the accounting practices of the company on the variables, the different international accounting standards and the risk of manipulation that owners can perform in the accounting data. In the case of this study, given Uruguayan legal regulations, the database is composed of audited Financial Statements and supported by an affidavit by the owners, which provides a certainty framework(15)(16).

Several similar studies have been carried out in many countries, but, in general, they deal with the industrial and commercial sectors. In any case, they constitute a starting point as long as they identify variables with an impact on profitability, such as indebtedness, number of employees, size of assets or level of activity, which will be used in this case(17)(18)(19)(20)(21)(22).

The best-known explanatory variables are the size given by the assets, the revenue or the number of employees. The debt-to-investment ratio, age of the firm, inventory levels, ratio of fixed assets to total assets and capital turnover are also analyzed. But there is no paradigm on the impact of these factors on the profitability of the company. The ROA is the dependent variable most used to measure profitability and, therefore, the variable that will be considered as the central axis of this discussion, but that does not imply that there is agreement on the causal relationships with the independent variables. It is also considered that it involves and combines various aspects of the company's economy, such as assets, revenues, costs and results(1)(23)(24)(25)(26)(27).

Therefore, the ways of measuring the absolute economic result and also the relative result are very diverse in the literature. Sometimes the Net Result, derived from the Result Statement, is used; in others, the EBITDA, and in others certain intermediate results. In terms of relative profitability, the ROA is mostly used, but in other circumstances, the ROE is used.

2.2 Conceptual framework for measuring profitability

Taking into account this background, this study will consider the following definitions:

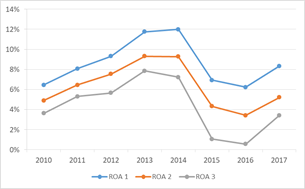

· Operating ROA 1: profit before taxes[III], interest and leases relative to total assets. Hereinafter, ROA 1.

· Operating ROA 2: profit before taxes and interest relative to total assets. Hereinafter, ROA 2.

· Financial ROA: profit before taxes relative to total assets. Hereinafter, ROA 3.

The value of the total of Assets (common denominator in the calculation of the three analyzed profitability ratios) is taken from the balance sheet presented in the declaration for the payment of taxes on Income on Economic Activities and Net Worth, form 1006 (version 3)(28), which constitutes the database used in this paper.

Variables are constructed in this way:

- ROA 1: Profit Before Taxes, Interest and Leases: Income minus Total Costs (not including payments for the use of external capital, interest on credits and leases) relative to the total Assets of the Statement of Equity of each company. For the economic approach of the agricultural literature, under conditions of complete information, the value of the leased assets should be added to the total assets of the balance sheet, since this approach evaluates the profitability of the resources used, regardless of their ownership. As such information is not available, ROA 1 overstates —in this perspective— the measure of economic profitability. For the accounting approach, this is equivalent to considering as its own assets land that is not owned by the company; a contradiction to the definition of assets.

- ROA 2: Income Before Taxes and Interest: Income minus Total Costs (payments for the use of leased assets are included, interest payments are not included) relative to total Assets. Given the information available, this way of estimating economic profitability can be considered balanced.

- ROA 3: Profit Before Tax: Income minus Total Costs (including all costs but Income Tax on Economic Activities and Net Worth) relative to total Assets in the Statement of Position. This way of measuring profitability focuses on the surplus appropriated by the business owner and, secondly, by the State, in taxes.

In all cases, the Income is made up of the genuine income from sales, plus —in the case of livestock companies— the Gross Agricultural Product, which is obtained, for each unit of analysis, directly as base data, since it is declared by each taxpayer.

Conceptually, the financial ROA (ROA 3) represents the final economic wealth appropriated by the producer, either in the form of cash or goods (assets), or reduction of their liabilities. In the case of companies that do not own the land, but lease it, as has happened with Argentine firms in Uruguay, the ROA may be higher than that of a land-owner company, since it is calculated exclusively based on movable assets (animals, seeds, working capital). That does not necessarily mean that the result is inaccurate, since it is the economic reality: they are more financially profitable since their fixed investment is lower. The exception would be a very high lease due to high land demand(29).

ROA 1 (operating) focuses on a more primitive, primary or operating profitability. It measures the result of agricultural operations. It is not an inadequate indicator in itself, but it is partial. The problem arises when, by not considering leasing, the ROA of the firms that lease is distorted, as in the case of the mentioned Argentine investments.

ROA 2 (operating) is an intermediate state between operating ROA 1 and financial ROA. Lease costs have been included, but the interest payment associated with the use of external capital remains in the surplus.

These operating (1 and 2) and financial ROA measurements are complementary if analyzed together, they can indicate where the firm's weaknesses and strengths are. A company can be profitable from an operating point of view (positive operating ROA), but with a financial situation that makes its final result negative; for example, evaluated through ROE. The interpretation of such a situation is very delicate. It is not possible to affirm that the company is operationally profitable without considering that its operating profitability is perhaps too low to withstand the financial constraints.

As for the ROA or the ROE option, if the intention is to link size with profitability, ROA is an ideal indicator —or more consistent—, since it is determined according to the asset, which is one of the most reliable indicators of size. Note that the asset includes cash, rights, goods, equipment and facilities,but also intangible assets, such as brand equity. On the other hand, ROE presents a more complex view, which is not always easy to interpret. This index is measured based on wealth. If a firm is very large, but simultaneously presents a high level of indebtedness, its equity will be small and will not represent its economic relevance, therefore not being a good indicator of size. Business profitability understood as the profitability of the company as a whole must be measured in regard to its assets and not on equity. ROE is designed to assess shareholder profitability —which is ultimately an external investor—, but it is not an indicator to analyze business performance in isolation. In general, its use is widespread in countries with developed and long-standing stock exchanges, a case that does not correspond to Uruguay, where these forms of financing are still incipient.

As for the calculation basis for the indicators in general terms, EBITDA or the net result can be used. EBITDA belongs to the group of indicators called financial. It is considered a good indicator of operating efficiency, but also incomplete, since it does not measure the ability to obtain good sources of financing and good tax structures, elements that affect the competitiveness of the company(1).

EBITDA could be used to compare companies and visualize their problem areas (commercial, operational, logistics), at least comparatively, or the advantages with respect to other companies in their sector, but it should not be used to measure and explain economic performance. Its use spread in the United States in the 1990s among financial analysts because there was a need to show positive results in companies that were growing based on debt, since it was an intense period in terms of mergers and acquisitions. It is considered a highly pernicious indicator and its use is correlated with deviations in accounting standards(30).

According to Bejar-León and Jijón-Gordillo(31), EBITDA is an inadvisable ratio, since it ignores the cost of depreciation and was used to show partial results; so it is a ratio criticized not only for its bias but for the opportunism of its practical implications.

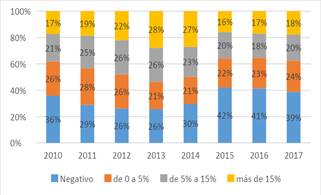

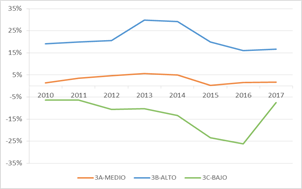

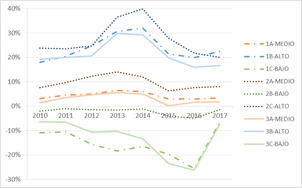

In summary, the use of ROA based on business result is postulated, instead of ROE, due to its consistency with the measure of business size, given by assets. It is suggested to compare the results of the study of 713 Uruguayan agricultural companies according to their size and profitability, measured by the operating ROA and the financial ROA, in order to obtain a conclusion based on empirical evidence. In this way, it is expected to observe whether there are noticeable differences in the evolution of profitability measured by one or the other indicator.

Christian Kuster

Christian Kuster